All things commodities

Hi there!

Resources are all the rage right now. Last week, we touched on the key drivers for most major commodities, so this week we're diving into a few specific stories, stocks and ideas.

With major commodity benchmarks/stocks starting to break out of multi-year bases, this could be a powerful move and a key sector to watch in 2026. I've got a feeling that 3/4 of what I write next year will be commodities related.

Let’s dive in.

Investor sentiment survey

.xlsx%20-%20Excel.png)

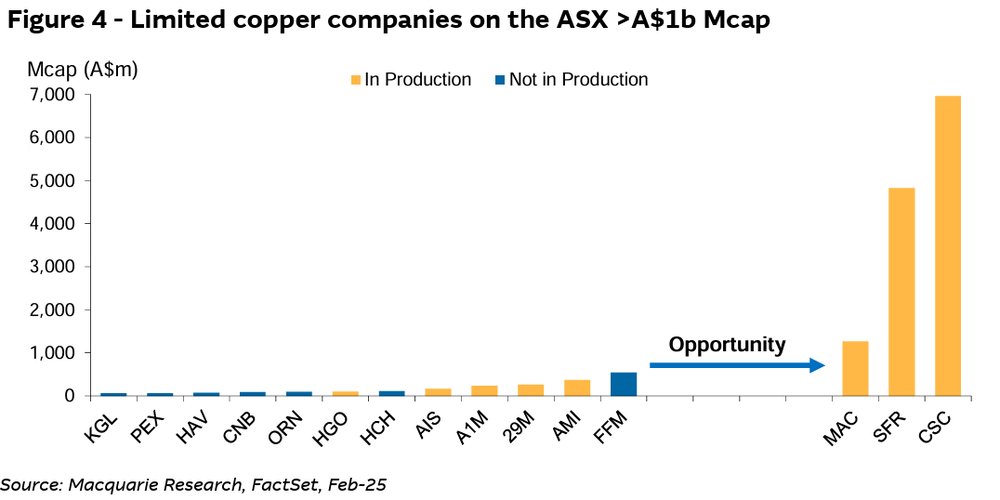

The copper complex

I’m not a big fan of the breadth of opportunities we have for copper.

The main names that come to mind include:

Larger cap producers: SFR, CSC plus BHP (~47% of Group EBITDA was copper, 22% NAV from copper) and Rio Tinto (20% of NAV from copper)

Smaller cap producers: AIS, 29M and HGO (struggling)

Higher-profile explorers: FFM, HCH

As the above Macquarie chart shows, there’s a real opportunity for emerging names to join the $1bn market cap club.

From the brink of death

Aeris Resources (AIS) has experienced one of the most insane hero-to-zero moments, with the stock falling from around $1.50 in July 2021 to a low of 8.5 cents in February 2024.

This followed a series of unfortunate events spanning low copper prices, major operational issues and production downgrades.

In August 2023, I genuinely thought the company was going to die. The stock suffered a 28% one-day selloff after announcing it was placing its Jaguar Project into care and maintenance due to large operating losses, while also securing a new $50 million working capital facility.

Now $50 million was a lot considering the company had a market cap of just $190 million at the time. Given that market cap, it had to choose debt since a capital raising of that size would have diluted shareholders to oblivion.

But the terms of the facility was honestly, a shark loan.

Interest rate: BBSY + 11% per annum (payable monthly)

Establishment fee: 3.5% of the facility limit

Exit fee: 3.5% of the facility if paid during the first 12 months, up to 8.5% if paid after 18 months of the term

Undrawn commitment fee: 5% per annum of the undrawn portion

Fast forward to today, Aeris is trading at 53 cents (~$580 million market cap), reported $45.2 million net profit after tax for FY25, and is sitting on $434 million in tax losses for future years. The decision to take on debt has left them in a prime position, highly leveraged to copper. Trading at around 11x FY25 earnings and 4x FY26 ests, they're not all that expensive either!

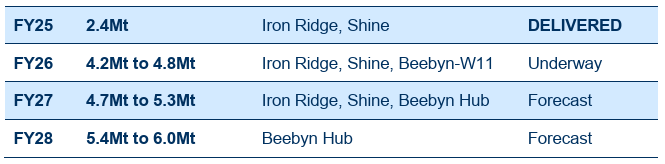

Mini-Fortescue

I’ve been following Fenix Resources for a while. The company operates three iron ore mines in WA as well as a bulk haulage and port services. From 2021-23, the stock yielded around 10-15% every year, backed by a highly cash generative business.

Come 2024, they flipped the switch and outlined plans to grow production from ~1.5wmt to 4Mtpa over the next ~12 months. No dividend was paid between 2024 and late 2025.

Yield-hungry investors weren’t happy about the news, with the stock falling ~12% (~27 cents) on the day of the initial dividend announcement. But fast forward to today, Fenix is up 86% year-to-date to 48 cents.

Earlier this week, the company outlined even more ambitious plans to grow production to 6.0Mtpa by FY28 and provide the base for 10Mtpa over the medium term.

You don't get many growth stories like this today.

Buying something for nothing?

Alright here me out – this week, St Barbara sold a portion of its Simberi Gold Project in PNG. It’s a recurring theme we’ve seen in the past 12-24 months, where governments are looking to get some skin in the game.

The terms of the deal weren't terrible and create a rather intriguing value proposition.

Sold 20% of Simberi to state owned Kumul for $100m

Kumul does not pay anything upfront and the $100m will be repaid via its future share of revenues

The selldown to Kumul is more about government buy-in and ensure a smooth process with obtaining a mining licence and tax resolution

Of the remaining 80%, half (40%) was sold to China’s Lingbao for $370m cash, which brings on board a partner to derisk funding

Now here’s where it starts to get interesting:

St Barbara had $157m cash and equivalents in the September quarter or $527m when you include the proceeds from Lingbao

Given its current share price of 51 cents, we’re looking at a cash backing of ~40 cents per share

Simberi’s latest feasibility study outlined a post tax NPV (8%) of US$1.8bn at US$4,000/oz and US$50/oz silver

St Barbara also owns three advanced gold development projects in Canada, with a combined 1.4Moz in ore reserves

At current prices, the company is effectively around 77% cash backed. Sure, it doesn't own 100% of Simberi anymore, but it's now more derisked from both a funding and operational perspective, along with three projects in much lower-risk jurisdictions.

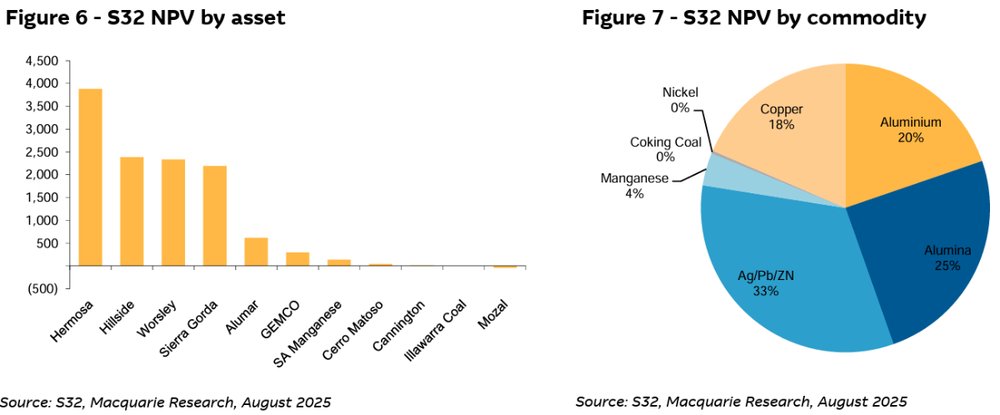

The market’s largest silver stock

The silver complex on the ASX became awfully dull after Dundee Precious Metals acquired Adriatic for $1.25 billion earlier this year.

While there are quite a few small caps to consider (e.g. Sun Silver (SS1), Silver Mines (SVL), Unico Silver (USL) and Andean Silver (ASL), there’s basically no large cap options.

Or maybe, we’re not looking hard enough.

A few weeks ago, it came to my attention that South32’s largest asset by NPV is the silver-lead-zinc Hermosa Project (Macquarie’s NPV by asset and commodity charts above).

Hermosa was purchased for US$1.6 billion in 2018 but bringing it online has been a dicey process (e.g. US$1.3bn impairment in 2023 due to soaring capex). Almost $2 billion in capex has been spent to date.

But by the end of it, Hermosa should be an absolute beast of a project. Here are some of Macquarie's projections:

FY27 production:

Silver: 0.7 million ounces

Lead: 11,700 tonnes

Zinc: 10,500 tonnes

FY30 production:

Silver: 9.7 million ounces

Lead: 168,300 tonnes

Zinc: 150,900 tonnes

Last laughs

All these miners are printing cash ... and so is OpenAI.

.png)