Hi there!

The ASX 200 is down 3.9% from its 21 October record high, with the path of least resistance flipping towards the downside. It's getting a little bearish out there, and you have to wonder whether we're in the midst of a garden variety 3-5% pullback or if it will unravel into something more. There are plenty of bearish talking points, some of which we'll unpack below.

Let’s dive in.

Investor sentiment survey

In case you were wondering

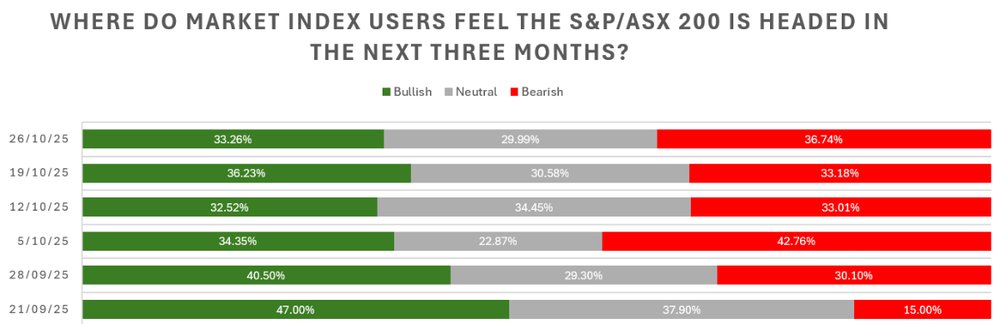

Since I started the Investor Sentiment Survey, there have been three instances where 'Bearish' sentiment exceeded 36%.

Week ended 22 June: The ASX went on a five-day skid as American B-2 bombers struck Iran's three main nuclear sites, marking a significant escalation in the Iran-Israel conflict.

Week ended 3 August: Bank weakness, Amazon sold off on quarterly earnings and Trump set a 10% global minimum tariff.

Week ended 5 October: The S&P 500 and Nasdaq suffered a 2.7% and 3.5% one-day selloff respectively after Trump threatened 100% tariffs on China.

What's interesting is that each instance marked a low point, with markets bouncing over the following days. These events ultimately proved to be noise amid broader tailwinds including AI momentum, strong corporate earnings, consumer resilience, a pickup in M&A activity and steady inflation.

However, we're now at a crossroads where such tailwinds might be challenged amid AI bubble concerns (OpenAI seeking government support, circular financing questions), very weak market breadth, hawkish rate repricing and commentary, and labour market softness.

Carma flops on ASX debut

.png)

Online used car dealer Carma was one of the most hyped IPOs in recent months and hoped to replicate the success of US-listed Carvana (~$65bn market cap) and Europe’s Auto1 (~$6bn).

Instead of debuting 10-30% above the offer price ($2.70), it finished the session down 7.0% ($2.50). Let’s take a closer look.

Carma targets Australia's $118 billion pre-owned automotive retail industry by sourcing vehicles directly from consumers, auctions and fleet partners, which are transported to its Sydney reconditioning facility before being listed online.

Customers can browse real-time inventory, access transparent vehicle histories and complete purchases entirely through Carma's website, with the company generating an average margin of approximately $4,000 per vehicle sold.

The business sold 2,000 cars in FY24 but remains loss-making with annual losses sitting around $35-36 million between FY24-FY26e. Revenue grew 43.5% in FY24 to $68.9 million but slowed dramatically to just 3.6% growth in FY25 at $71.4 million, making the FY26 forecast of 78.7% revenue growth to $127.6 million appear ambitious.

Operations are currently based entirely in NSW with plans to roll out additional low-cost centres and expand into Victoria, Queensland and South Australia.

To be fair, Carma debuted into a tough backdrop with the S&P/ASX Emerging Companies Index down 12% from its 16 October record high. But at the same time, this is a roughly $400 million market cap company that will likely be loss-making for quite some time.

How'd the cap raises ago?

The recent hype behind critical metals has seen many companies tap the market for capital they couldn’t even imagine raising a few months ago.

As the hype dies down, they’ve turned many participants into … bagholders.

WA1 Resources raised $100m at $17.00, now ~$15 (11% lower)

Australian Strategic Metals raised $55m at $1.20, now ~73c (39% lower)

Arafura raised $475m at 28c, now 25 cents (10.7% lower)

Northern Metals raised $60.5m at 5.1c, now 3.5c (32% lower)

Black Rock Mining raised $10m at 2.1c, now 1.6c (24% lower)

Though there were a few success stories, including:

Meteoric Resources raised $42.5m at 14c, now 18c (29% higher)

American Rare Earths raised $15m at 32c, now 41.5c (30% higher)

Lindian Resources raised $91.5m at 21c, now 30.5c (45% higher)

I guess my key takeaways from this critical metal trade is:

Expect an avalanche of capital raising activity when a breath of life comes into a struggling sector

If a sector goes vertical and then falls sharply, the 'easy money' period is probably over and you're in for some near-term volatility.

Job market jitters

Weakening jobs data is making life hell for central banks, with the Fed prioritising the labour market while the RBA is caught in a pickle between hot inflation and cracks in the jobs market.

Two weeks ago, Australia's unemployment rate spiked to 4.5% in September from 4.3% in the prior month, marking the highest unemployment rate since November 2021. We've since seen more downbeat data:

Australian job ads fell 2.2% month-on-month in October, according to the ANZ-Indeed survey.

Job ads in October were 7.4% lower than a year ago, and remained just 8.4% higher than pre-pandemic levels.

There were strong gains in retail and food sectors ahead of the Christmas season, but that was more than offset by a large decline in education.

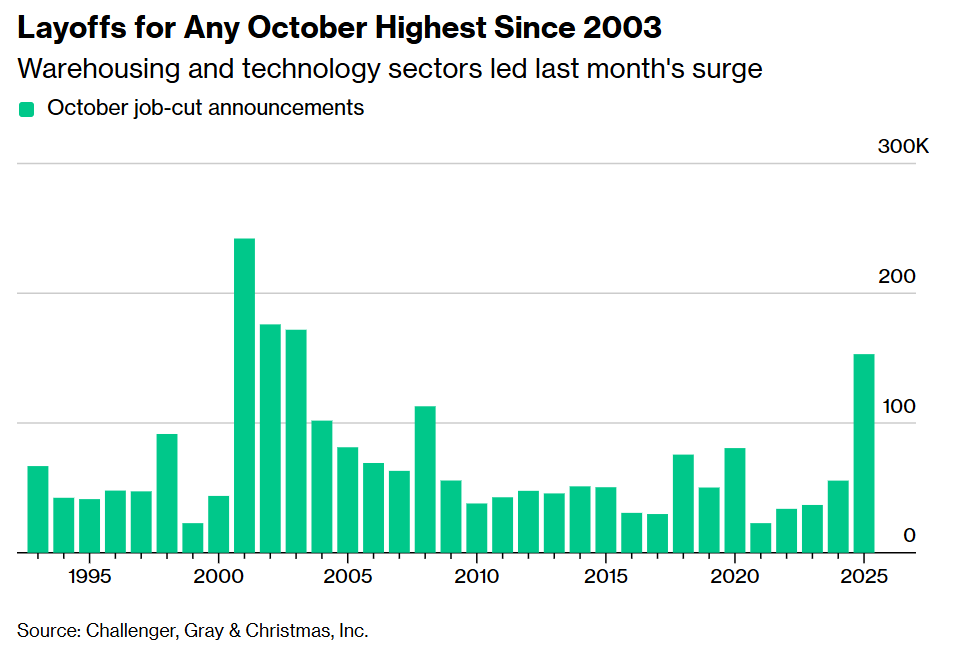

Meanwhile, US companies announced over 150,000 job cuts in October, according to data from from Challenger, Gray & Christmas Inc.

This represents an almost 100% increase vs. the prior month, nearly triple that of October 2024 and the most since 2003

Year-to-date job cuts have exceeded 1 million, up 65% year-on-year and up 44% from all of 2024

Planned hires for the year totaled just 488,000, down 35% from the prior year and marking the weakest hiring outlook since 2011

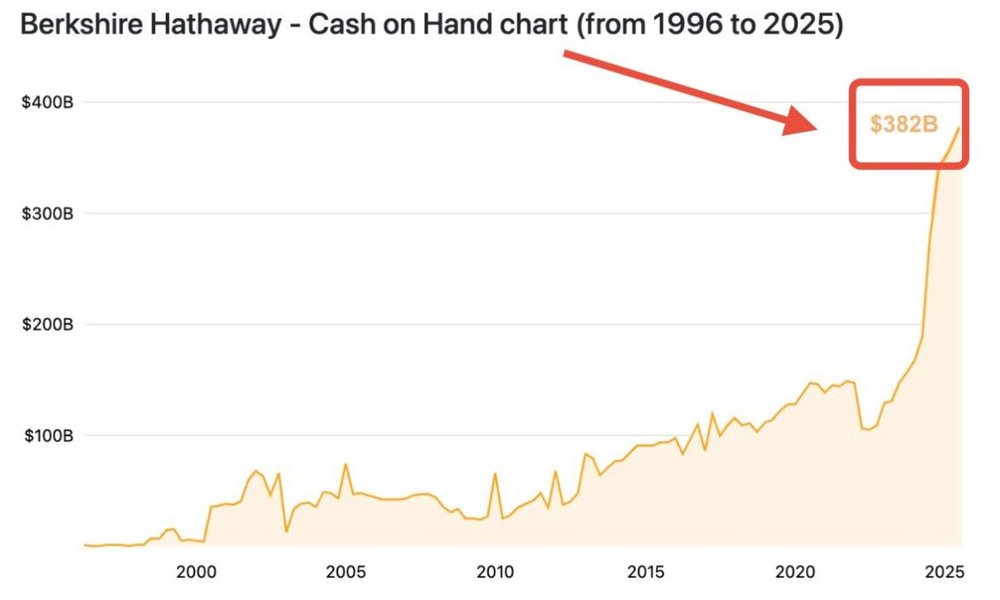

Buffett’s cash stash

Berkshire Hathaway reported a record high cash balance of US$381.7 billion last quarter. But the fine print is even more wild.

Buffett sold a net US$6.1 billion worth of stocks last quarter and trimmed major positions in Apple and Bank of America

Buffett has halted share repurchases for five straight quarters (despite Berkshire sitting ~16% off its 2-Apr record high)

Berkshire is trading at a ~70% premium to book value, which is beyond Buffett’s historical comfort zone for buybacks

The Buffett Indicator recently hit ~220%, meaning the total stock market is trading at historically stretched levels relative to GDP

Investing vs. gambling

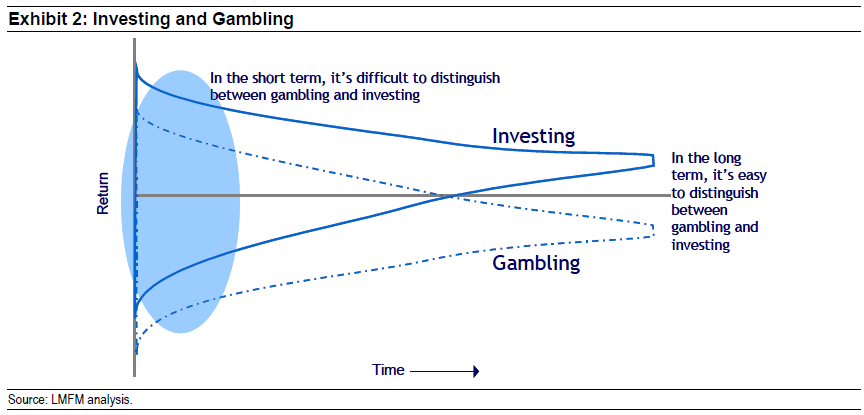

This chart by Michael Mauboussin crossed my feed this week – it’s a really great exhibit of how skill and luck influence outcomes in different domains and time frames.

In essence:

Gambling outcomes are random and independent of skill

You cannot improve your gambling odds in the long run as the house always has an edge

Investing is not purely skill-based and luck plays a big role in short-term outcomes

Edge, repeatability and process will turn investing outcomes in your favour over time

Personally, I feel like I dabble between both (unfortunately). Sometimes I execute near-perfect, process-driven trades backed by experience, technicals and fundamentals. Other times, I don't think twice and enter some random position (that tends to go south more often than not).

Last laughs

It's that time of the year again.