All things Iran and Energy

Hi there!

Never a dull moment in markets – from record highs last week to a ~4% drop this week.

This weekender is talking all things Iran and energy, though given how fast the situation is moving, some of it may already be outdated by the time it reaches you. Nevertheless, here's a quick catch-up on Friday's developments:

Conflict has spread to 14 over countries

Strait of Hormuz has effectively shut down and zero oil tankers transited Thursday, down from 65 pre-war

US Gulf allies are running critically low on interceptors, the UAE alone faced nearly 1,150 drone and missile attacks since Saturday

Israel ordered the full evacuation of Beirut's southern suburbs and struck 80 Lebanese targets in 24 hours

Trump is now openly claiming a role in picking Iran's next Supreme Leader and says he supports a Kurdish uprising inside Iran

More importantly, what the conflict has meant for energy markets:

Strait of Hormuz is effectively closed - a key passage where 20 million barrels of oil and 20% of global LNG transits it daily, with no meaningful pipeline alternative

Analysts see US$100 oil as a floor if the closure holds, JPMorgan warns US$120 by week three and Deutsche Bank says US$200 in a full blockade.

Asia is most exposed, where 84% of Hormuz oil flows there. Japan sources 95% of its crude from the Middle East.

Europe faces a gas crisis after Qatar Energy declared force majeure, halting production. European gas futures briefly doubled in 48 hours.

Supertanker rates jumped from US$37,000 to US$177,000/day

The inflation risk is severe as energy costs feed into food, transport and manufacturing. One analyst called it potentially three times worse than the 1970s Arab oil embargo.

So what does all this mean for energy prices and markets moving forward?

Let’s dive in.

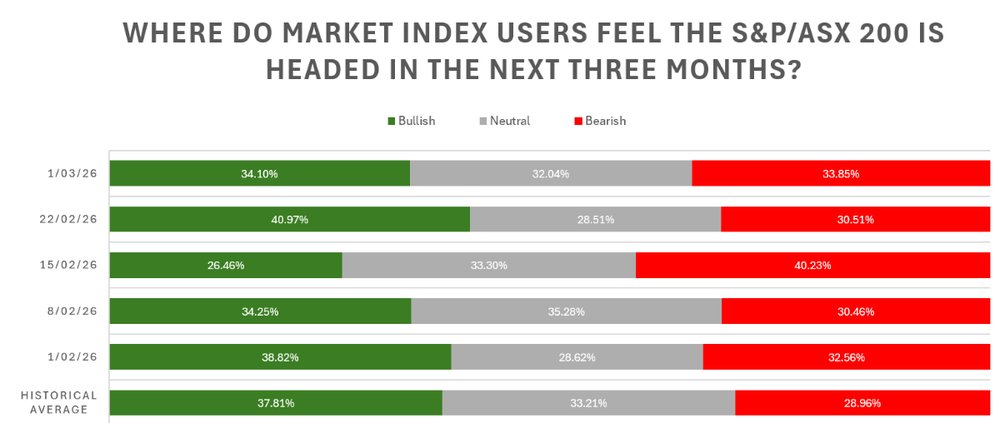

Investor sentiment survey

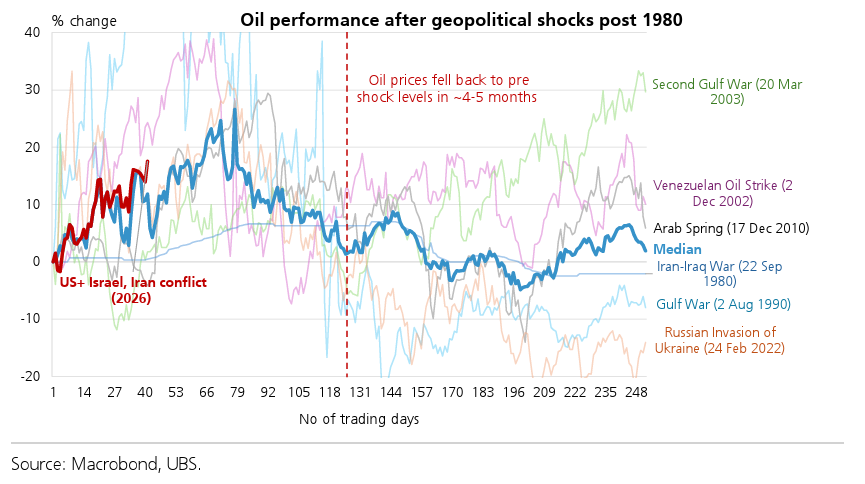

Oil prices tend to stabilise

UBS says any initial price shock from major military events since the early 1980s tend to dissipate over the next four to five months.

The impact on such geopolitical shocks used to be higher in the 1950-1980s, as OPEC controlled over 50% of global oil supply, while most countries had small to no strategic oil reserves, and few means of hedging for price shocks.

One key difference from previous crises is that crude markets are already running a decent surplus at the global level, according to UBS, with excess supply expected to persist over the next 12-15 months.

The bad news is that everything remains up in the air. Trump has suggested the conflict could last four to five weeks, though he's also flagged it could run far longer. Even if the Strait of Hormuz stays technically open, sky-high insurance costs and producer caution could choke flows through the passage just as effectively as a formal closure.

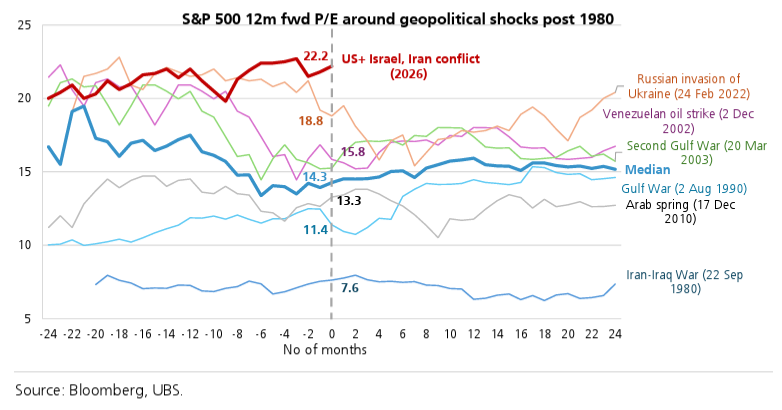

Little room for error

Markets have historically shrugged off geopolitical shocks, but the starting point this time is very different. UBS notes the S&P 500's median multiple heading into prior oil shocks since 1980 was 14.3x against 22.2x today. The ASX 200 is similarly stretched, trading at a forward price-to-earnings of 18.7x.

What you don't want is a situation where an elevated multiple meets deteriorating earnings forecasts.

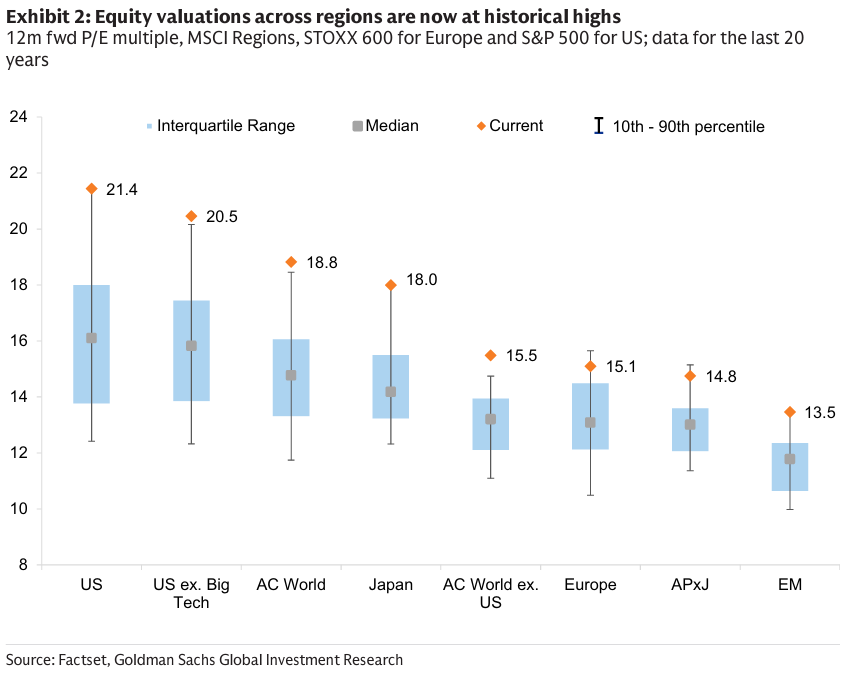

Speaking of valuations

On valuations, a Goldman Sachs chart shows how the broadening of equity returns beyond the US over the past year has pushed every major region well above its longer-term average.

So really, jumping from the US to say, Europe, is just going from one expensive market to another.

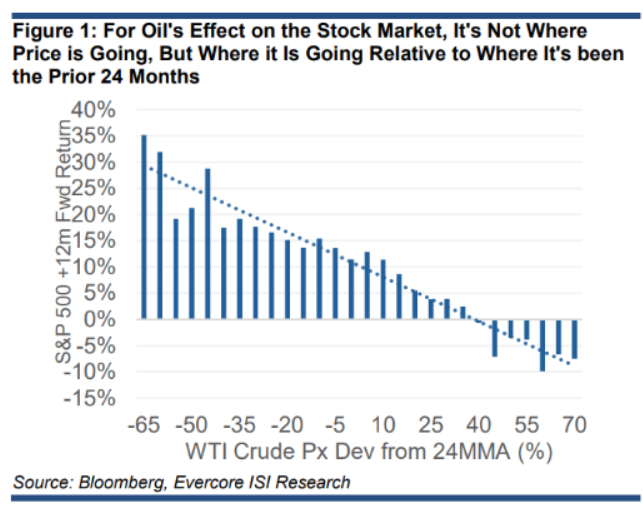

Oil's not the problem (yet)

According to Evercore ISI, what matters for equities isn't the oil price in isolation, it's where it sits relative to its 24-month moving average.

When oil trades 35-50% above that average, 12-month forward equity returns have historically turned negative.

At 10-20% above, returns compress but stay positive.

Right now, oil above US$75 sits roughly 9% above its 24-month average, exerting only mild downward pressure.

The danger zone for stocks, based on data back to 1985, kicks in somewhere between US$93 and US$97 a barrel.

Time to make some cash?

The recent resource rally is a timely reminder that in most cycles, miners spend years in the trenches, a few grinding along in mediocrity, and only one or two in genuine glory.

You only need to look as far as the past couple of years for lithium, nickel, oil and gas (and more) to get what I mean.

Could the Iran crisis bring about a replay of FY22 for the energy sector?

Last laughs

While the Iran war broke out last Saturday, EU Commission President Ursula von der Leyen basically said "hold up, we don't work on weekends, let's circle back on Monday."

The internet had a field day with this.

One of the most liked comments from her posted was:

"The EU must prepare a 12 points white paper to ensure current war is fought in compliance with ESG, GDPR, Digital Services Act (DSA), Corporate Sustainability Due Diligence Directive (CSDDD), EU Migration and Asylum Pact and all green initiatives. If not, new regulation on all future wars fought will be adopted."

.png)