88% of the ASX 200 is bleeding

Hi there!

I went to the servo – and left feeling bullish on bikes, EVs and vegetable oil.

It's certainly getting rougher by the week. Markets are holding up well (all things considered) and seemingly desperate to rally off any good news, though reality continues to play out in the opposite direction. One of the odd data points that really stood out this week was a sub-component of the US February Producer Price Index – a 48.9% jump in the cost for fresh and dry vegetables. Though economists noted such data is highly volatile and often doesn't fully reach consumers.

The outcome for markets feels increasingly all-or-nothing – but there's no telling whether the Iran conflict will continue to boil over. Markets are certainly pricing in a more positive outcome, while our wallets – not so much.

Let’s dive in.

On a side note: I’m away for the next two weeks (Malaysia, Singapore). Coincidentally, all of my prior holidays have coincided with market weakness (the latest three being: Nov-25 was a brief rotation out of tech and US government shutdown uncertainty, Mar-25 right before Liberation Day and Dec-24 when Powell pushed back on rate hikes).

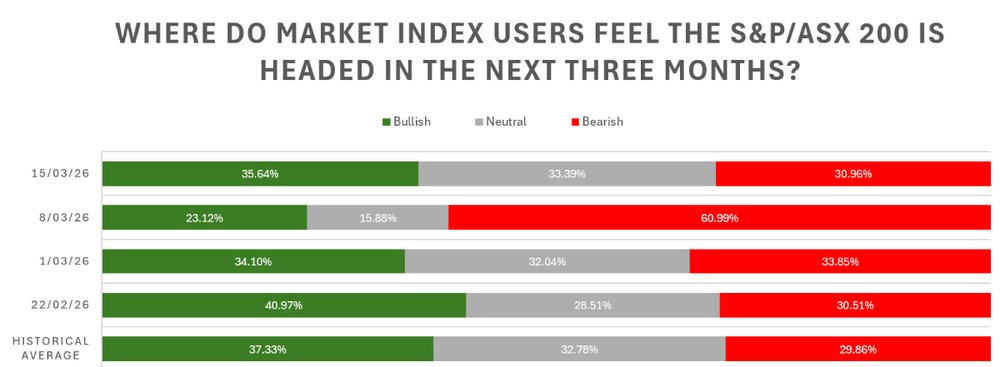

Where did the bears ago?

.png)

Our Investor Sentiment Survey saw an abnormal spike in bearish respondents for the week ended 8 March, hitting 60.99%, only to halve the following week to just 30.96%, even as market conditions continued to deteriorate.

I've plotted the survey outcomes (measured as the spread between bulls and bears) against the ASX 200, and no immediate trend stands out.

What is interesting is the sample size. The bearish spike came from only ~700 respondents, while the most recent week (15 March) drew more than quadruple that number.

Investor Sentiment Survey

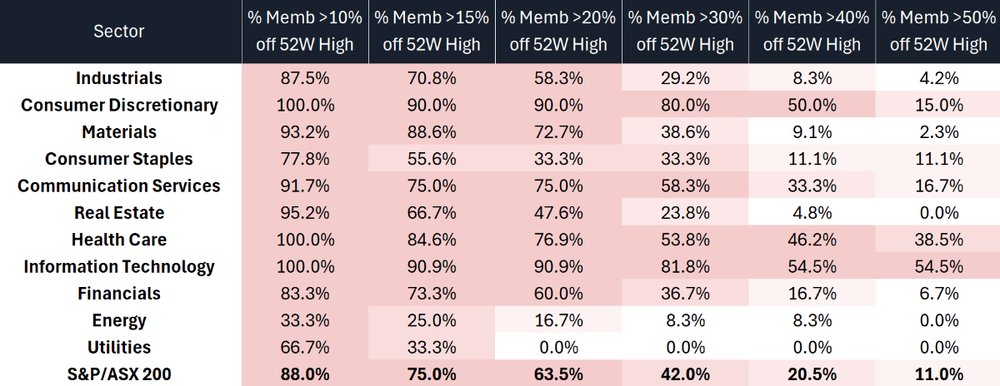

Aussie breadth check

The ASX 200 is down ~8% from recent highs and down 3% YTD but things are far more depressing beneath the surface.

The above table observes how far a percentage of ASX 200 constituents are trading away from their 52-week highs.

At a glance:

88% of the ASX 200 is more than 10% off its 52-week high

42% are more than 30% off, confirming rather broad market weakness

Tech and Health Care are the hardest hit, with 100% of members down more than 10% and over 50% down more than 40%

Consumer Discretionary is under serious pressure, with every member down more than 10% and 80% down more than 30%

Energy and Utilities are the standout defensive pockets, with only 33% of Energy names down more than 10% and no Utilities member having fallen more than 20%

The Big Four banks is the main reason why the Index is holding up relatively well, with CBA, NAB and Westpac still up ~9.7%, ~7% and ~5% year-to-date.

What a week for gold

What a rough one – The All Ords Gold Index is down ~32% from its 2 March record high, effectively wiping three months worth of gains in just three weeks (and now down 15% YTD). Truly, a staircase up, elevator down moment.

What you might find odd is how gold is struggling against a backdrop where it should, in theory, be soaring. Here are some ideas why:

Gold's historic drivers (real rates, volatility, liquidity) have been replaced by sovereign reserve accumulation flows since 2022, when the freezing of Russian reserves pushed surplus countries to seek alternatives to US Treasuries. Gold became the primary "neutral" reserve asset

This shift made gold pro-cyclical, meaning it rallies when surplus economies generate strong export revenues and accelerates reserve accumulation, and sells off when that surplus generation is disrupted, which is exactly what the Hormuz blockade is doing to Gulf export revenues

China, the world's largest oil importer, facing slowing growth and compressed surpluses, with the same dynamic rippling through Korea, Taiwan, Japan and the rest of Asia, collectively weakening the reserve accumulation bid

Leveraged funds and CTAs are selling gold to cover margin calls elsewhere given it ran ~66% in 2025 and remains the most liquid asset with the largest embedded gains, making it the first cab off the rank in a forced liquidation

A firmer US dollar, rising real yields (a headwind for non-yielding assets), a hawkish Fed, and systematic long liquidation

Mike Henry steps down

BHP CEO Mike Henry is stepping down after a legendary run. Let’s take a look at his key achievements over his ~6 year tenure.

Jansen project approval (Aug-21): Approved the massive Jansen Stage 1 project in Saskatchewan, Canada. While costs have blown out from US$5.7bn to US$8.4bn (Jan-26), it still gives BHP a long-life entry into the world's best potash basin, a commodity with strong long-term demand tailwinds from food security.

DLC unification (Jan 2022): BHP dismantled its historic dual-listed company structure, consolidating under a single Australian listing. This complex restructuring streamlined governance and enhanced capital allocation flexibility.This also made it easier to use BHP scrip for M&A.

Woodside Petroleum merger (Jun-22): BHP divested its petroleum business to Woodside Energy in a deal valued at around $40bn, allowing the company to exit fossil fuels and sharpen its focus on "future-facing commodities”. BHP shareholders received 1 Woodside (WDS) share for every 5.5340 BHP shares held.

OZ Minerals acquisition (2023): BHP acquired copper miner OZ Minerals in FY23, bolstering its copper portfolio. The ~US$6.4b deal added Prominent Hill and Carrapateena to BHP's copper book.

Other worthwhile mentions include:

Anglo American bids (2024): Worth noting as a swing-and-miss.Henry presided over two failed attempts to buy rival Anglo American, last November walking away from a deal just 18 months after its previous ill-fated approach.

WAIO cost leadership: Under his watch, BHP's Western Australia Iron Ore business improved operational performance and increased its lead as the lowest cost, highest margin major iron ore producer in the world.

Becoming the world's largest copper producer: The company became the world's largest copper producer, with more than half of recent first-half earnings coming from copper.

BHP’s Americas President Brandon Craig will now take the reins, inheriting a pretty strong hand, with the right commodity mix for the decade ahead. Though it doesn’t come without a few headaches surrounding Jansen, iron ore headwinds, geopolitical complexities and the Samarco dam liability.

US airlines lift earnings guidance

Big oil spikes typically weigh on airline shares. Take Qantas for example:

11-13 Jun 2025: Brent up ~12%, Qantas down 4.2%

26 Sep – Oct 2024: Brent up ~9.8%, Qantas down 6.6%

24 Aug – 19 Sep 2023: Brent up ~14%, Qantas down ~12%

24 Feb – 8 Mar 2022: Brent up ~31%, Qantas down 12.2%

The above chart is simply the Qantas share price dividend by Brent, it's largest input cost. When it's falling, it implies oil is spiking faster than Qantas or because the market is pricing in something negative, like margin compression. All the above time stamps coincide with the above dates, suggesting the market doesn't really trust their hedging book and pricing power.

What’s fascinating is that US airline companies have been upgrading their earnings guidance in recent days, including:

Delta lifted Q1 revenue growth guidance to high-single digits (from up to 7% previously), with bookings up 25% year-on-year and eight of the top 10 sales days in company history occurring this quarter

American Airlines raised Q1 revenue growth guidance to more than 10%, up from 7-10% previously, also absorbing a roughly $400m fuel cost hit but offsetting it with stronger-than-expected demand across all cabin classes

JetBlue lifted operating revenue guidance to 5-7% growth, up from 0-4%, citing strengthening demand and improvement across premium and core cabin segments

Though none of them mentioned what this means for net profits. Only Delta reaffirmed its profit guidance.

Last laughs

Viva Energy and Ampol might be national treasures right now. The two companies operate Australia's only two remaining refiners – the Geelong Refinery in Victoria and Lytton in Brisbane.

So why don't we just build a few more refineries to fix the diesel shortage?

This chart (I don't know who made it) has been doing the rounds on X, explains why.