UBS cuts 2026 oil price forecast, sees US$60 bottom before second-half recovery

UBS forecasts Brent at $62/bbl in 2026 as 1.9Mb/d surplus peaks early before narrowing, with geopolitical risks key swing factor.

Source: iStock

Mentioned

KEY POINTS

- UBS forecasts Brent crude will average US$62 per barrel in 2026, bottoming at US$60 in the first quarter when surplus peaks at 1.9 million barrels per day before gradually recovering through the year.

- Geopolitical disruptions in Russia, Iran or Venezuela could push prices into the mid to high US$60s, while peace agreements or faster Venezuelan recovery could drive Brent to the mid-US$50s.

- OPEC+ plans to resume unwinding production cuts from April but effective increases expected to be only 40% of headline figures at around 0.7 million barrels per day due to capacity constraints.

UBS has downgraded its 2026 oil price forecast, projecting Brent crude to average US$62 per barrel –down US$2 from previous estimates – as the market faces a persistent supply glut of 1.9 million barrels per day throughout the year.

The investment bank expects prices to bottom at US$60 per barrel in the first quarter, when the surplus peaks, before stabilising and recovering later in the year. This pattern differs markedly from 2025, when the surplus remained constant.

In 2026, the surplus is forecast to narrow over the course of the year, potentially setting up a recovery in the second half.

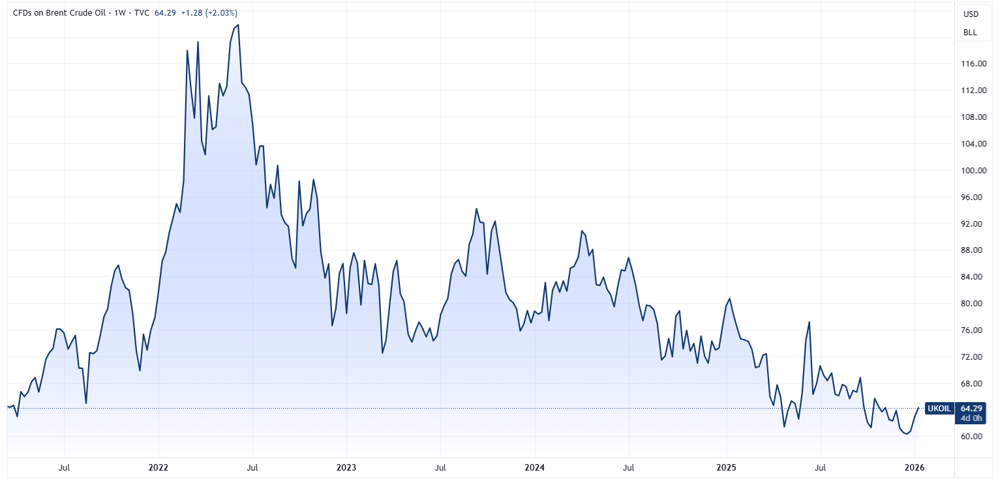

Brent crude daily price chart (Source: TradingView)

Near-term pressure, mid-year recovery

The analysts see a weak first quarter, with seasonally lower demand and higher OPEC+ production keeping markets oversupplied. However, as the surplus narrows through the year, UBS expects investor focus to shift from oversupply concerns to dwindling spare capacity. This transition could support prices in late 2026 and into 2027, with Brent forecast to reach US$70.

The analysts maintain their longer-term view of US$75 from 2028 onwards, based on slowing non-OPEC supply growth.

Geopolitical wildcards could swing prices

UBS sees geopolitics as the key swing factor for oil markets in 2026, with regional supply disruptions capable of pushing prices well outside its base-case range.

Russia: Output is already running about 0.5mbpd below OPEC+ targets due to infrastructure attacks, with further downside risk if the EU moves towards tighter sanctions, including a potential ban on maritime services.

Iran: Production has been stable near 3.3mbpd, but intensified US pressure on Iran’s shadow fleet could cut supply by up to 0.5mbpd.

Venezuela: Production fell to around 0.7mbpd in December from 1.0mbpd in October due to US sanctions, though a rollback could see production rapidly rebound to 1.0 mbpd or higher.

Downside Risks Appear Limited

Despite the bearish supply outlook, UBS sees limited downside from current levels. With oil prices near multi-year lows and positioning already extremely bearish, the investment bank argues the market has largely priced in negative scenarios.

The primary downside risk would come from resolution of current geopolitical tensions. A Russia-Ukraine peace agreement could push prices below US$60 by reducing the risk premium and adding modest Russian supply. Combined with faster Venezuelan production recovery, this could take Brent to the mid-US$50s.

A global economic slowdown that reduces demand by 0.5 million barrels per day vs. forecasts could compound these pressures. In a recession scenario, OPEC+ might aggressively chase market share, potentially driving prices briefly below US$50.

However, UBS notes several factors limiting downside risk. OPEC+ retains significant spare capacity of approximately 4.1 million barrels per day (excluding Iran and Venezuela), meaning voluntary cuts could unwind more quickly if prices fall too far. At prices in the mid-US$50s, the bank expects further slowdown in non-OPEC+ supply and a potential pause or reversal in OPEC+ production increases.

OPEC+ Policy Remains Key Uncertainty

The bank still expects OPEC+ to resume unwinding its 1.65 million barrels per day voluntary cuts from April 2026 at the previously announced pace of 137,000bpd per month through December.

Eight OPEC+ countries confirmed a pause for February and March due to seasonality, but UBS believes the full unwinding remains likely given OPEC's optimistic market outlook.

Importantly, UBS expects effective production increases to remain well below headline figures, at approximately 40% or around 0.7 million barrels per day. This pattern is in-line with the initial phase of cuts reversal, where only 70% of announced increases were implemented due to capacity limitations and elevated production in certain countries.

The most important event of the year is likely to be the full OPEC+ meeting in late November, where the group will need to agree on a new production framework for 2027 and beyond.

Demand Growth Moderately Constructive

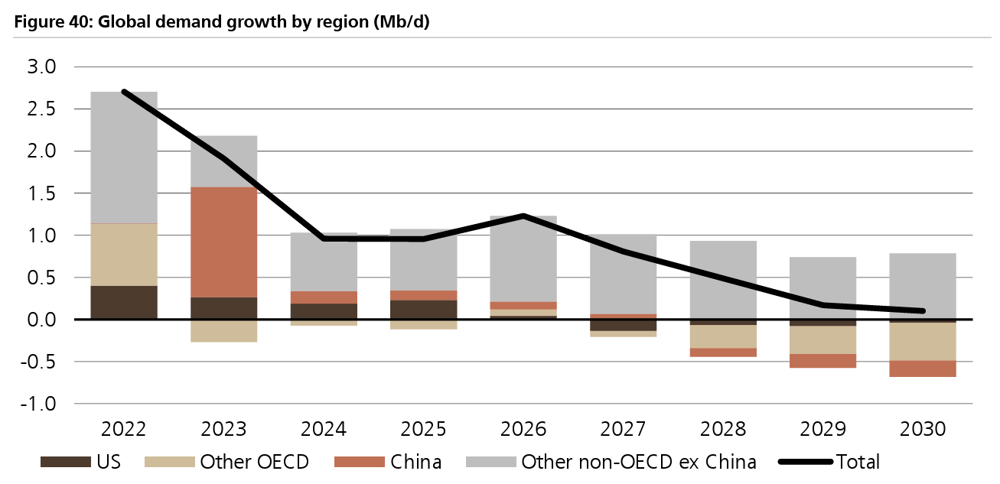

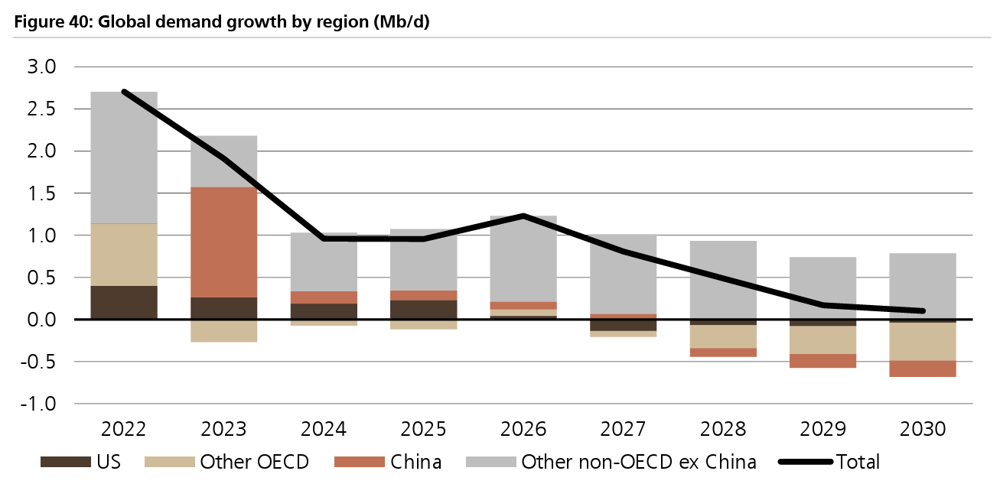

UBS projects global oil demand growth of 1.2 million barrels per day in 2026, an improvement from 1.0 million barrels per day in 2025, driven entirely by non-OECD countries. This sits near the midpoint of agency forecasts ranging from 0.9mbpd (IEA) to 1.4mbpd (OPEC).

Global demand growth by region, with post-2024 growth driven largely by non-OECD ex-China countries (Source: UBS)

Chinese demand remains the biggest uncertainty. UBS estimates China's demand grew just 0.1mbpd in 2025, down from initial forecasts of 0.2mbpd, despite GDP growth coming in slightly higher than expected. This reflects accelerating energy transition, with electric vehicle sales expected to exceed 50% of total new car sales in 2026, accounting for nearly 65% of global EV sales.

Putting it all together

The below table shows a breakdown of the various upside and downside drivers to UBS' forecast and the relative importance of the catalysts.

Brent price forecast based on various upside/downside drivers (Source: UBS)

Looking Beyond 2026

UBS expects peak oil demand to be reached by 2030, though this is likely to be followed by a long plateau rather than a sharp decline as rising efficiency and EV adoption take effect.

As non-OPEC supply growth slows more rapidly than demand, global spare capacity should decline, limiting negative price impacts and supporting the forecast of higher prices from 2027 onwards.

The transition year of 2026 is shaping up to be one of two halves, with near-term weakness giving way to stabilisation and recovery as fundamentals gradually improve and market focus shifts from surplus to spare capacity constraints.