This might be the 'cheapest' gold stock on the ASX

St Barbara trades at a 30% discount to its cash position alone, with billions in development asset value yet to be recognised by the market.

Source: Shutterstock

Mentioned

KEY POINTS

- St Barbara is approximately 70% cash-backed with $527 million in net cash against a market cap of around $740 million.

- The company holds $2 billion in asset value (NPV) across its 40% Simberi stake and 100% ownership of the Atlantic Development portfolio in Nova Scotia

- Key risks include an ongoing PNG tax reassessment and pending mining lease approvals, though PNG's 20% stake should help de-risk these issues.

A 'cheap' stock means different things to different investors. It might come in the form of a low price-to-earnings ratio, a cashed-up business trading at low enterprise value, or an M&A deal that unlocked substantial earnings accretion and synergies.

As subjective as it may be, the numbers behind St Barbara (ASX: SBM) make it a genuinely interesting stock to unpack. By the end of this piece, you'll hopefully understand what I mean by 'cheap'.

The story so far

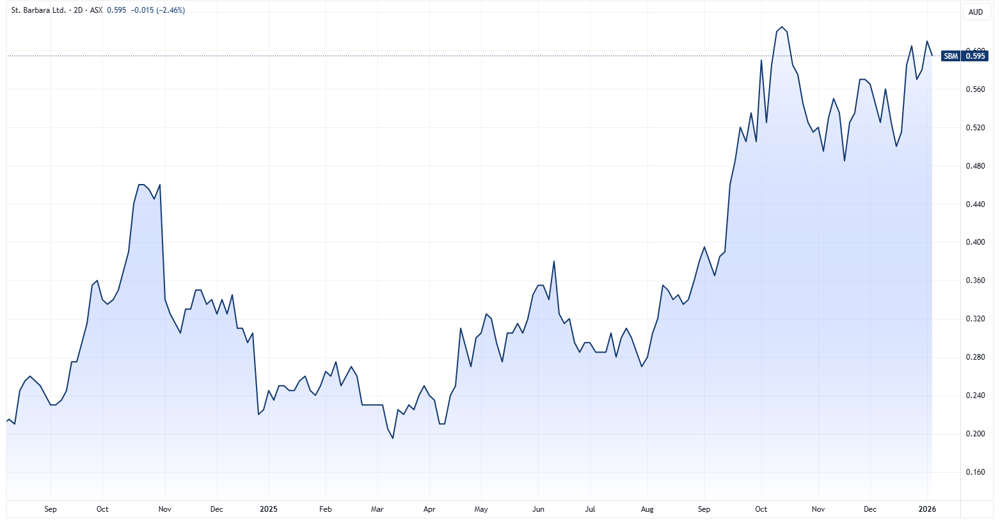

Two developments have defined St Barbara in recent months: negative catalysts that caused an almost 60% selloff between October and November 2024, and a more recent deal with the PNG Government and a major Chinese shareholder.

St Barbara price chart (Source: TradingView)

The announcements that drove the sharp selloff included:

5 November 2024 (-26%): St Barbara kicked off a $110 million capital raise to accelerate development at its Simberi mine in PNG. The offer price was 38 cents, a 17.4% discount to its last traded price.

24 December 2024 (-34.4%): PNG's Internal Revenue Commission issued a tax reassessment to St Barbara's PNG subsidiary for approximately $210 million, covering disputed tax positions and depreciation treatment going back many years. At the time, the amount owing was effectively as large as the company's market cap ($210m vs. $215m).

St Barbara lodged a formal objection to the assessment in February 2025. By August 2025, the PNG IRC indicated the previous assessment would be revoked and replaced with a revised version at a later date.

More recently, St Barbara struck a deal with PNG's state-owned Kumul Mineral Holdings and China's Lingbao Gold Group.

The company sold 20% of Simberi to Kumul for $100 million. This does not necessarily value 100% of Simberi at $500 million but represents a 'discount' for the government in return for smooth permitting and formal tax resolution. This amount doesn't even come as cash, with St Barbara providing it as a non-recourse loan to Kumul, with repayment to come from Kumul's future share of revenues.

On the same day, St Barbara sold 50% of Simberi to China's Lingbao Gold Group for $370 million cash, subject to various conditions including approval of Simberi's extended mining lease and a positive FID outcome.

What this leaves St Barbara with

A net cash position of $527 million ($157m cash with no debt as at 30 September 2025 and $370m from Lingbao)

40% ownership of Simberi and 100% of its Atlantic Development portfolio (three advanced development projects in Nova Scotia with a combined 1.4Moz in ore reserves)

The Simberi Feasibility Study (Dec 2025) reported a post-tax NPV of US$1.81 billion (A$2.6 billion), which translates to approximately A$1.0 billion for St Barbara's 40% stake. This NPV is based on US$4,000/oz gold and US$50/oz silver assumptions.

Atlantic's 15-Mile processing hub concept study had an estimated post-tax NPV of A$1.08 billion using a gold price of US$2,500. The PFS is currently underway and expected in the March quarter 2026.

The result is a company that's effectively ~70% cash backed ($527m cash vs. current market cap of ~$740m) and carrying at least A$2 billion in "value" based on its 40% Simberi stake and 100% Atlantic development portfolio.

So what's the catch?

There is no catch. It's hard to deny the value on the table, but there are a few risks to note.

Just a few months ago, the company faced a tax reassessment bill roughly equal to its entire market cap. The tax reassessment is still ongoing and while PNG's stake in the project should suggest a positive outcome, you don't know until you know. Simberi is also still pending a mining lease renewal approval. This creates a lingering overhang.

The Atlantic portfolio is also working through some of its own permitting challenges. St Barbara's latest presentation (20-Nov-25) noted:

"To date, the Company has not received a proposal for the Atlantic assets that provides St Barbara shareholders with a sufficient participation in the future potential value realisation from the 15-Mile Processing Hub Project."

The presentation did note that the "permitting environment and government support for resource development is improving rapidly and St Barbara now has the potential opportunity to re-open Touquoy mine to process low and medium grade stockpiles left at closure."

The bottom line: St Barbara is heavily cash-backed (subject to Simberi-related conditions), with the 20% divestment to PNG likely serving as a catalyst to de-risk the ongoing tax dispute and approvals required for production.