The ASX 200 is holding up. The stocks inside aren't

The ASX 200 is barely down for the year, but beneath the surface 84.5% of stocks are off their highs and blue-chip blowups are stacking up.

.jpg)

Source: Shutterstock

KEY POINTS

- The ASX 200 is down just 1.3% year-to-date, but 84.5% of its constituents are more than 10% off their 52-week highs and nearly one in eight has been more than halved

- Discretionary, Tech and Health Care are the most damaged sectors, with every member trading off its highs and Discretionary trading as if consumers are in for a hard landing

- With the RBA flagging rising inflation risks, money markets pricing further hikes and no AI thematic to lean on, the path of least resistance for the local market remains lower

The S&P/ASX 200 is down 2% year-to-date and up just 2.8% in the last twelve months. Yet for many investors it feels like absolute carnage out there, with another supposed "blue-chip" blowing up by the day.

The index is holding up against an increasingly fragile backdrop of soaring oil prices, sticky inflation, rising bond yields and the fallout of the Federal Budget. But beneath the hood, things are rather (unsurprisingly) abysmal.

Index up, stocks ... not so much

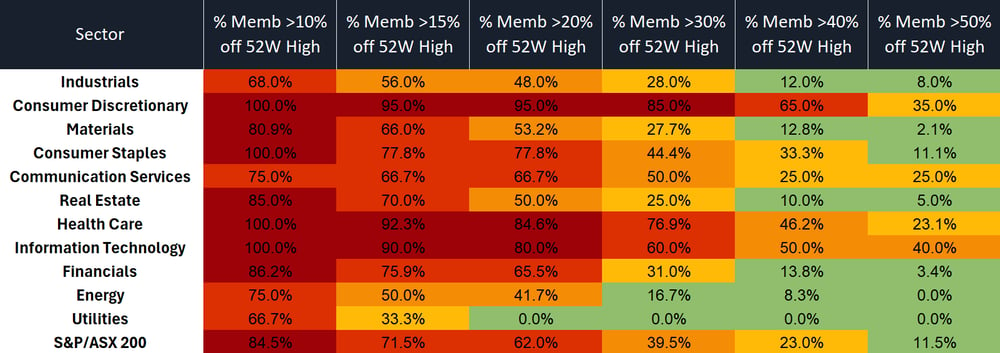

There's some severe pain beneath the surface. As of Monday, 84.5% of ASX 200 constituents were trading more than 10% below their 52-week highs, and 39.5% were down more than 30%.

Nearly 1 in 8 ASX 200 stocks has been more than halved. 11.5% of the index is trading more than 50% below its 52-week high.

Health Care, Tech and Discretionary have been hit hardest. Every member of all three sectors is trading more than 10% off its highs, and between 23% and 40% of names in each have been more than halved.

Discretionary is the most damaged sector, with 85% of members down more than 30% and 35% off by more than half.

Energy and Industrials are holding up better. Both have a meaningful share of members still within 30% of their highs and almost no battered names. Energy has none down more than 50%, Industrials just 8%.

The "average" stock is in a deeper drawdown than the index suggests. With more than half the market down more than 20%, the typical ASX 200 name is closer to bear-market territory.

Source: Market Index

Downgrades galore

Large-cap corporate updates and results have disappointed in recent weeks. The point of the blue-chip label starts to look thin when so many of them are falling double digits in a single session. The below is not an exhaustive list but captures several high-profile names and themes.

Brambles (18-May): Shares down 20% after downgrading FY26 guidance, with sales growth cut to 2-3% (from 3-4%) and underlying profit growth to 3-5% (from 8-11%) on a ~$60m earnings hit from US repair capacity constraints.

CBA (13-May): Q3 cash NPAT of ~$2.7bn (flat QoQ, +4% pcp) missed elevated expectations on flat revenue and a $200m top-up to collective provisions, with shares falling 10.4%, the largest one-day drop on record.

CSL (11-May): Shares fell 15.9% after guiding FY26 revenue to ~$15.2bn (4% below consensus) and NPATA to ~$3.1bn (7% miss), with ~$5bn of non-cash pre-tax impairments flagged across FY26 and FY27, driven by US immunoglobulin channel destocking (~$300m), China albumin pricing (~$200m) and other headwinds (~$150m).

JB Hi-Fi (6-May): Q3 FY26 delivered consistent sales growth across JB Hi-Fi Australia (+4.0%, comp +2.6%), JB Hi-Fi NZ (+23.2%, comp +15.2%) and The Good Guys (+2.5%, comp +2.5%), broadly in line with the first-five-weeks update. The key management comment here was: "We are seeing significant supplier component related cost increases and stock availability shortages, along with heightened competitive activity". The stock fell 6.2% on the day.

Endeavour Group (4-May): Q3 retail sales +2.9% and hotels +3.7% (boosted by Easter timing), though hotels momentum has softened with March-April growth of just 1.5%, a ~$400m inventory build to buffer Middle East supply disruption.

Woolworths (30-Apr): Provided its Q3 trading update, most of which was in-line with market expectations. This was the main line that triggered a 7.7% selloff: "Reported FY26 Australian Food EBIT growth is still expected to be in the mid to high single digit range but no longer at the upper end of the range. This reflects incremental costs associated with direct fuel exposures in Q4 as well as investments to support customers in managing their budgets in a period of rising inflation including the Price Freeze announced today."

Cochlear (22-Apr): Shares nosedived 40% after the company cut FY26 underlying NPAT guidance by ~30% to $290-330m (from $435-460m at the low end) on soft developed market implant volumes, lower gross margins, Middle East supply chain headwinds and $18-25m of restructuring costs.

Interestingly, a long list of consumer-facing companies flagged late March as a clear inflection point. Endeavour, Accent Group, Super Retail, Vicinity Centres and others all pointed to an abrupt moderation in sales and forward-looking expectations.

Where to from here?

Such poor breadth is not the mark of a healthy market, and unfortunately Australia has no leverage to the AI thematic propping up the S&P 500, South Korea's KOSPI and Taiwan's TWSE at all-time highs.

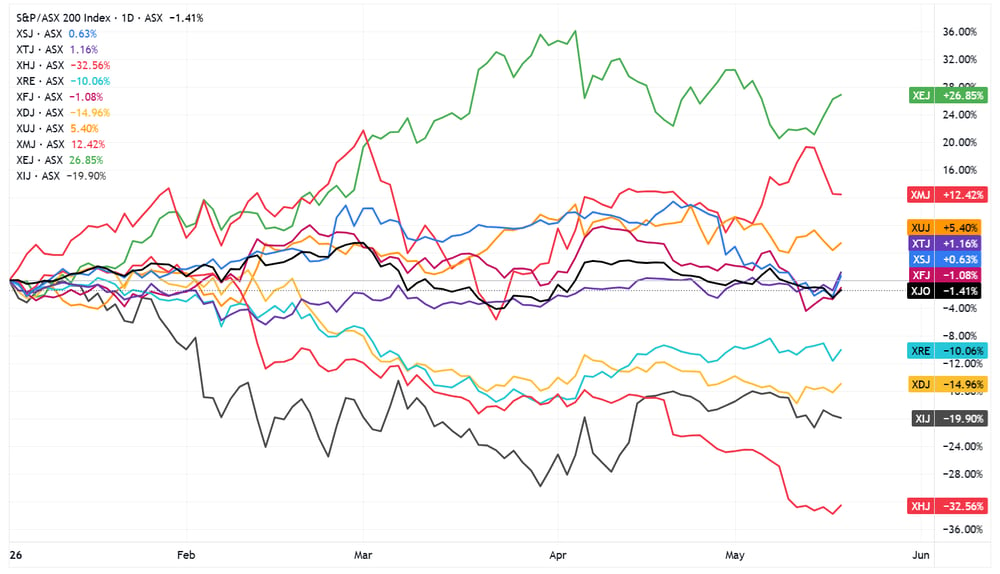

A look at S&P/ASX 200 sector performance shows Energy and Materials battling to offset softness in banks and heavy weakness across Discretionary, Tech and Health Care.

S&P/ASX 200 vs. sectors (Source: TradingView)

This is taking place against a highly inflationary backdrop, where RBA Assistant Governor Sarah Hunter warned this morning that the central bank is "more worried now than we have been in the past" about inflation expectations becoming unanchored amid successive supply shocks. Money markets are now pricing at least one more hike this year, with around a 40% chance of a second.

With re-accelerating inflation, soaring bond yields, a fragile Middle East, global central banks widely expected to hike rather than cut, and the fallout from the Federal Budget still working through, the path of least resistance for markets is lower. The Strait of Hormuz could reopen and inflation could peak. However, for now, markets have a wall of worries to climb, and plenty of stocks already carry the scars.