Stagflation hits the ASX, and UBS picks miners over banks

UBS expects no RBA cut until November 2027 and is staying out of banks, REITs and retailers, favouring miners and industrials.

Source: Shutterstock

KEY POINTS

- UBS expects the RBA to hike 25 basis points in August and hold until a first cut in November 2027, well later than the market is positioning for.

- Every ASX sector except resources is now seeing earnings estimates cut, which UBS thinks will limit any rally in banks, REITs and consumer stocks.

- Miners and industrials are the key Overweights, with the investment bank keeping its year-end ASX 200 target at 8800.

In this article

UBS is telling clients to stay out of banks, REITs and retailers and to keep their money in miners and industrials, betting that a stagflationary economy and a central bank stuck on hold will drag the domestic-facing parts of the market further behind the rest of the world.

The call, from strategist Richard Schellbach, rests on a view well outside consensus. While parts of the market are starting to position for the next RBA move being a cut, UBS expects the opposite.

Schellbach's team sees another 25 bp hike in August, then nothing until a first cut in November 2027. That's more than a year later than many are penciling in, and it reshapes the entire sector argument.

Earnings momentum flips negative

The more immediate problem is the market's earnings outlook. Outside resources, every sector on the ASX is now seeing analysts cut forward profit expectations, and UBS expects those downgrades to keep coming.

The latest batch of Australian economic data certainly smells like the stagflationary mix that weighs on consumers and squeezes corporate margins.

April unemployment was 4.5%, up from 4.3% in March and above market expectations of 4.3%. This marks the highest unemployment print since late 2021

April CPI was up 4.2% year-on-year, down from 4.6% in March following the reduction of the fuel excise (from 52.6c to 20.6c at the beginning of the month)

April trimmed mean ticked up to 3.4% and services inflation was at 3.5%, all above the RBA's 2-3% band

Today's Q1 GDP was up 0.3% quarter-on-quarter and 2.5% year-on-year, below market expectations of 0.5% and 2.7% respectively

Fair Work Commission also lifted the minimum wage by 6.0% and modern award wages by 4.75%

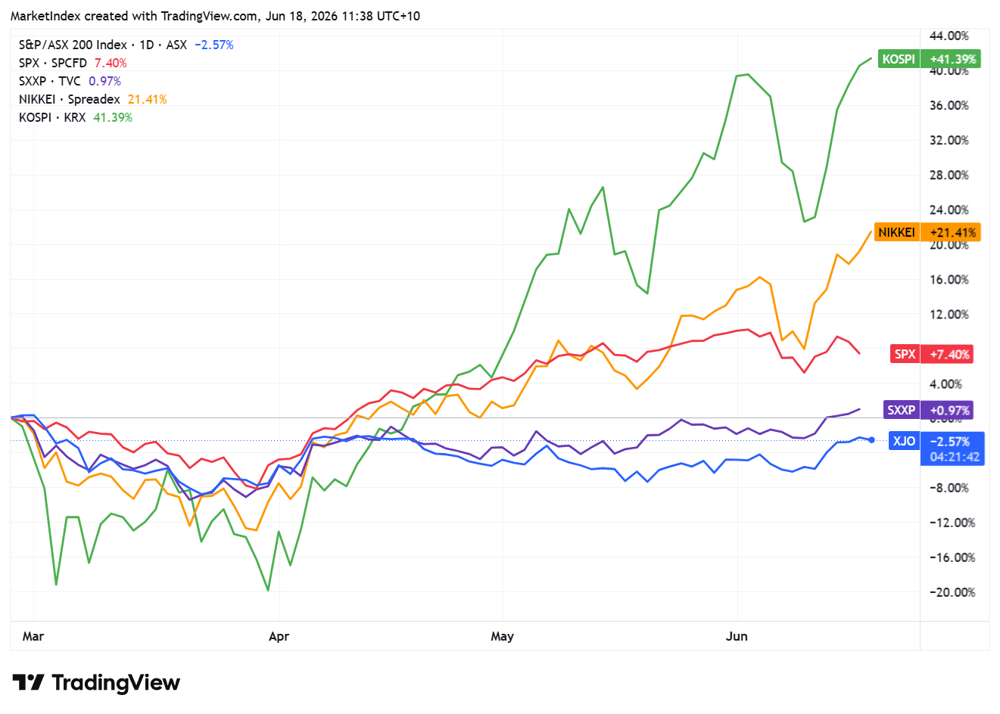

With a stagflationary economy at home and estimates still falling, UBS argues that ability to look through the cycle is running out. This downbeat view coincides with the ASX 200 falling more than global peers during the first month of the Iran conflict, then bouncing far less, once hard-leading fears eased.

ASX 200 (blue) vs. Kospi (green), Nikkei (yellow), S&P 500 (red) and Stoxx 600 (purple) since 26-Feb-26 | Source: TradingView

A frothy starting point

The harder fact is that all this is happening from expensive starting prices. The median ASX 200 industrial stock trades above its long-run average price-to-earnings multiple, and well above the range that held before COVID. REITs and consumer names have de-rated over the past six months, which would normally start to rebuild the case for them. But UBS isn't convinced.

If earnings downgrades keep landing, the recent rally in those sectors will quickly run out of steam. Banks look the most exposed of all, still trading on rich multiples while credit growth faces clear downside risk.

The below UBS sector scorecard shows the divide:

Banks: 18.6x forward earnings for 2026

Discretionary: 26.0x, the priciest of the domestic-facing groups

Real Estate: 18.8x despite the downside risk to earnings

Materials: the preferred hunting ground, trades on 17.5x

Industrials: 25.3x, which UBS holds despite the full multiple

The ASX 200 as a whole trades on 19.7x forward 2026 earnings, with the index's profits expected to grow about 12% that year.

Where UBS wants to be

Miners stay the top Overweight. Schellbach concedes valuations look full, but argues prices can push higher anyway as money rotates out of the banks and into resources. It is less a call that miners are cheap than a call on where the money has to go.

Industrials are the other Overweight, where UBS likes the sector for the government spending and investment behind it, and frames it as a way for local investors to get indirect exposure to the AI and data centre build-out without buying the offshore tech names directly.

Here's a full breakdown of their sector ratings:

Overweight: Mining, Industrials, Healthcare, Insurance, Small Caps, TMT (technology, media, and telecommunications)

Neutral: Energy, Consumer Staples, Infrastructure and Utilities

Underweight: Banks, Consumer Discretionary, Real Estate

UBS held its year-end ASX 200 target at 8,800, a level that leaves the local market behind, while the global equity bull market continues charging ahead. The research report comes back to the central idea that as long as the economy carries that stagflationary feel, and earnings keep getting cut, the parts of the market tied to the Australian housing and consumers stay a hard place to make money.