Silver prices are surging and this ASX silver giant is hiding in plain sight

South32’s Hermosa and Cannington projects could shift earnings from aluminium to silver-lead-zinc as prices climb.

Source: iStock

Mentioned

KEY POINTS

- Hermosa project has the highest NPV of any South32 asset, with first production expected in H1 2027 and a 28-year mine life.

- Cannington contributes less than 5% of NPV, has six years of reserves, but remains a strong short-term base metals producer.

- Rising silver prices could materially increase South32’s EBITDA and EPS, potentially shifting focus from aluminium to silver-lead-zinc.

South32 (ASX: S32) is a staple name within the ASX's resource complex. Investors most commonly associate it with aluminium production and the leftover base metal assets that BHP did not want in its 2015 spinoff. But one of South32's greatest assets and a potential factor to watch moving forward is its silver production via the Cannington and Hermosa projects.

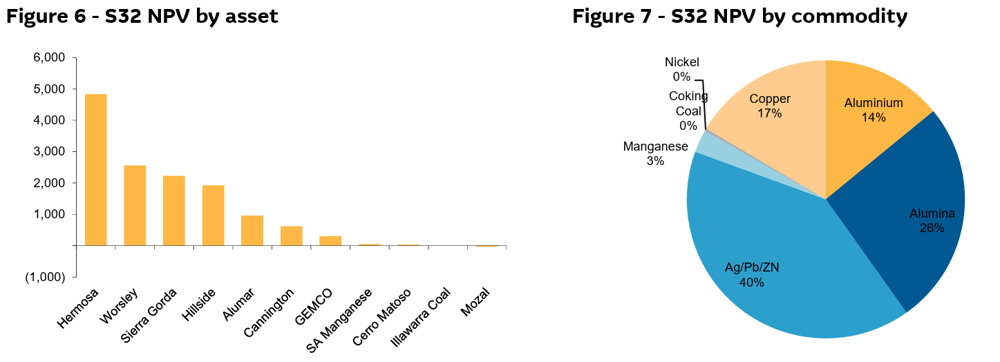

According to Macquarie's latest modelling, Hermosa has the highest net present value (NPV) of any South32 asset. In terms of NPV by commodity, silver-lead-zinc now makes up 40%, on par with aluminium and alumina combined.

Source: Macquarie Research, January 2026

At present, South32 does not derive much of its earnings from silver. Its Cannington project produced 12.7 million ounces in 2024, alongside 92,400 tonnes of lead and 44,500 tonnes of zinc.

The company's latest half-year 2025 results reported Group EBITDA of US$1.01 billion, with Alumina and Aluminium businesses accounting for US$543 million (54%) and US$136 million (13.5%) respectively.

However, as silver prices trend higher and South32 continues to advance Hermosa towards production, there may come an inflection point where silver-lead-zinc contributes more to the company than aluminium.

Hermosa in a nutshell

South32 owns the Hermosa project in Arizona, acquired through its takeover of Arizona Mining in 2018, where the remaining 83% was acquired for approximately US$1.3 billion in cash.

Hermosa hosts multiple deposits, with the Taylor zinc-lead-silver deposit being the first to be developed, and the Clark deposit targeted for battery-grade manganese.

The project was hit by a US$1.3 billion write-down in July 2023 due to higher development costs, pandemic impacts and significant water-logging challenges. The Board approved development of the Taylor project with capital expenditure of US$2.2 billion in February 2024. First production is targeted for the first half of 2027, with an initial mine life of 28 years.

Macquarie forecasts the following production profile:

2027e | 2028e | 2029e | 2030e | |

|---|---|---|---|---|

Silver (Moz) | 0.7 | 4.1 | 7.7 | 9.7 |

Lead (kt) | 11.7 | 70.4 | 133.0 | 168.3 |

Zinc (kt) | 10.5 | 63.2 | 119.3 | 150.9 |

Source: Macquarie, January 2026

If you napkin maths the revenue outlook at current silver prices (US$90/oz) – Hermosa becomes quite the cash cow.

Cannington Mine

The Cannington mine accounts for less than 5% of South32's NPV. The project has approximately 10 million tonnes in ore reserves, supporting only six years of production, though various life-extension options are currently being explored.

Nevertheless, Cannington remains a strong base metals producer in the short to medium term.

2027e | 2028e | 2029e | 2030e | |

|---|---|---|---|---|

Silver (Moz) | 8.7 | 10.6 | 9.0 | 8.7 |

Lead (kt) | 90.0 | 92.8 | 78.5 | 76.1 |

Zinc (kt) | 44.0 | 49.6 | 42.0 | 40.7 |

Source: Macquarie, January 2026

The bottom line

South32 is still three to four years from reaching peak silver production. However, the surging silver price is making it increasingly difficult to ignore the material earnings impact on Cannington and Hermosa.

On Thursday, UBS said "silver is expected to be strongly supported by fundamentals and speculative flows, which sees us upgrade prices up to around 40%... forecasting an average of US$79/64/oz for 2026-27."

"As a result, South32's Cannington mine EBITDA lifts by up to 38%, Group underlying EBITDA by up to 7% and EPS by +14/10/5% in 2026/27/28e."

The analysts also noted: "The upcoming transition of the CEO role, with Matthew Daley set to start 2 February 2026, has fuelled speculation around portfolio simplification including a potential part or full sell-down of Cannington, given record high silver prices."

There was no mention of Hermosa in the note.

South32 now sits at an interesting juncture, where aluminium prices are also breaking out to near four-year highs while silver becomes an increasingly important part of the company's value proposition.