Should you buy the dip on Megaport shares?

Megaport shares plunged after its FY24 results, with a weaker FY25 outlook to blame. Is this a chance to buy the dip? We investigate.

Source: Shutterstock, Market Index

Mentioned

KEY POINTS

- Megaport is viewed as major potential beneficiary of strong AI, cloud, and data storage trends

- Shares have performed strongly since the beginning of last year, but very recently have taken a dive, now trading around half of their 2024 peak following a poorly received FY24 result

- We check in with the big brokers, who have just updated their forecasts, ratings and price targets for Megaport to see if they think investors should buy the dip

Megaport (ASX: MP1) has been a market darling since the AI craze kicked off last year, and this has helped its share price more than triple over that time. Yesterday, however, MP1’s share price plunged after the release of the company’s FY24 results – and are now trading at roughly half of their peak.

So, is this a good time to buy “quality on sale” as many wise investors tell us to do? We check the latest research from the big brokers to see if they think if MP1 is a buy, hold, or sell.

Megaport price chart (For full size image: Click here)

{kind=link}

FY24 key numbers & takeaways

Revenue: $195.3 million vs guidance $190-$195 million and consensus* $195.6 million

Earnings before interest, tax, depreciation and amortisation (EBITDA): EBITDA $57.1 million vs guidance $56-$58 million and consensus $54.2 million

Underlying net profit after tax (NPAT): $9.6 million

Full year dividend: No dividend was declared (same as previous corresponding period)

FY25 Guidance:

Revenue: $214-$222 million vs consensus $231.5 million

EBITDA: $57-$65 million vs consensus $71.1 million

Key Takeaways:

First ever year of positive net cash flow (+$28 million)

Business saw growth across all operating regions, but particularly in North America which is the company’s largest business (57% of total revenue)

Increase in revenue driven by organic growth and impact of pricing changes implemented in FY23 having a full year to run

Net revenue retention declined, however, due to global trends and internal pricing issues – recent pricing adjustments are expected to improve customer expansion

*Consensus numbers supplied by Street Account by Factset

Individual broker views

UBS: Downgrade to NEUTRAL from BUY | Target price: cut to $10.15 from $15.85

FY24 result was “solid” underpinned by cost cutting, price increases and historical growth from maturing client base, however results from large investment in sales team is “taking longer than anticipated”

The key disappointment in the results was FY25 guidance, up 12% at the midpoint versus consensus estimates around up 19%

Broker notes they like the “business, its market leadership position, upside from expanding customer wallet and the cloud/AI structural thematic”, but is concerned about FY25 earnings downgrade, and therefore wants to see more stabilisation in existing customer base

Macquarie: Retain OUTPERFORM | Target price: cut to 13.60 from $15.60

Broker acknowledges FY25 guidance is “soft/conservative”, but opines “this is already in the price”.

MP1 is “A genuine first-mover in a large and rapidly growing global end market”, broker says

Goldman Sachs: Retain BUY | Target price: cut to $12 from $14

Broker notes FY24 numbers were in line with consensus, but revenue was 1% and EBITDA was 7% below its own forecast, however third quarter trends were positive

Broker acknowledges FY24 guidance is around 11-15% below consensus, and this “implies a deceleration in either subscriber growth or average revenue per user (ARPU) growth”

“Despite the soft operational trends in recent periods, we expect still robust top-line growth, with the increased focus on profitable growth supporting an attractive earnings profile over FY24-26.”

Jefferies: Retain BUY | Target price: cut to $13.40 from $17.51

Broker notes that FY25 guidance is the main disappointment in results release, putting this down to challenges in Net Revenue Retention. Broker believes management are addressing these issues, and guidance could be conservative

Broker anticipates margins will expand as revenue growth accelerates

Despite its near-term challenges, MP1’s remains a solid investment case as the company stabilises its cost base, this leads the broker to reaffirm its positive outlook

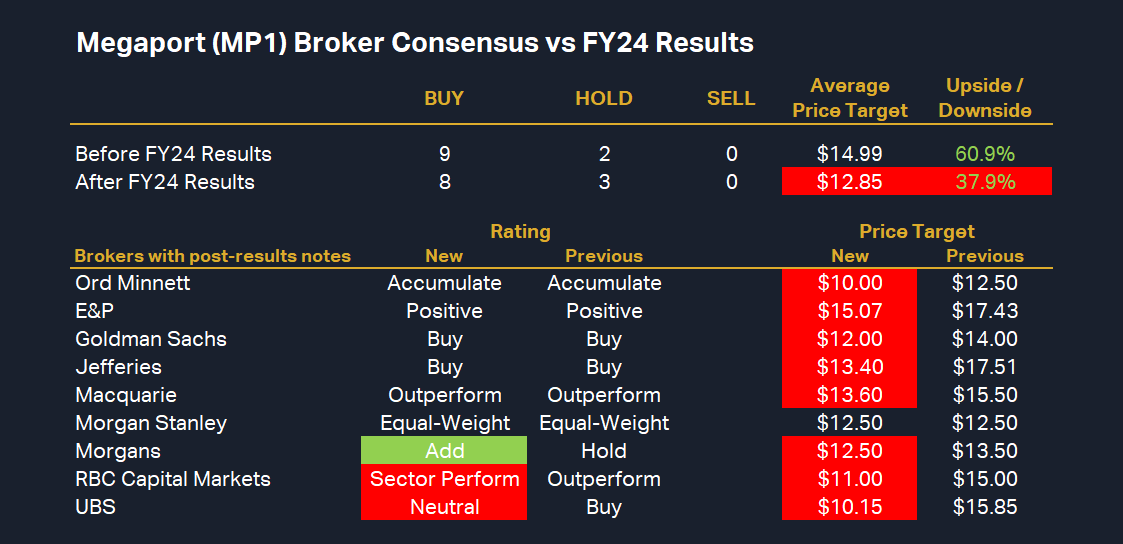

Megaport broker consensus: Buy, Hold, or Sell?

%20Broker%20Consensus%20vs%20FY24%20Results.png)

Megaport broker consensus (For full size image: Click here)

{kind=link}

The above table shows all ratings and targets for MP1 from broker research notes since May 1 (to keep it current). To obtain MP1’s Broker Consensus Rating, we assigned a value of +1 to any rating better than HOLD/NEUTRAL/MARKETWEIGHT, a value of 0 for any rating equivalent to HOLD/NEUTRAL/MARKETWEIGHT, and a value of -1 to any rating worse than HOLD/NEUTRAL/MARKETWEIGHT.

We then take the average of all assigned rating values and assign a Broker Consensus Rating of BUY to average rating values greater than +0.5, a rating of HOLD for average rating values between -0.5 and +0.5, and a rating of SELL for average rating values less than -0.5.

Using this model, MP1’s average rating value is +0.73, down from +0.82 prior to its FY24 results, resulting in its Broker Consensus Rating remaining at BUY.

MP1’s consensus (average) target price is $12.85, down a substantial 14.3% from $14.99 prior to its FY24 results. This suggests brokers believe the stock is around 38.9% undervalued based upon the closing price on 21 August of $9.32.

It’s worth noting that the consensus price target may fall further over the next few days as the two brokers we have on file who have not yet updated their analysis on MP1 post-results may do so. Both brokers have a price target on file in excess of $15, and if the cuts at other brokers are anything to go by, we could see the current $12.85 consensus target price ease a little further.