ResMed’s Q2 margins keep climbing, while valuation sits below history

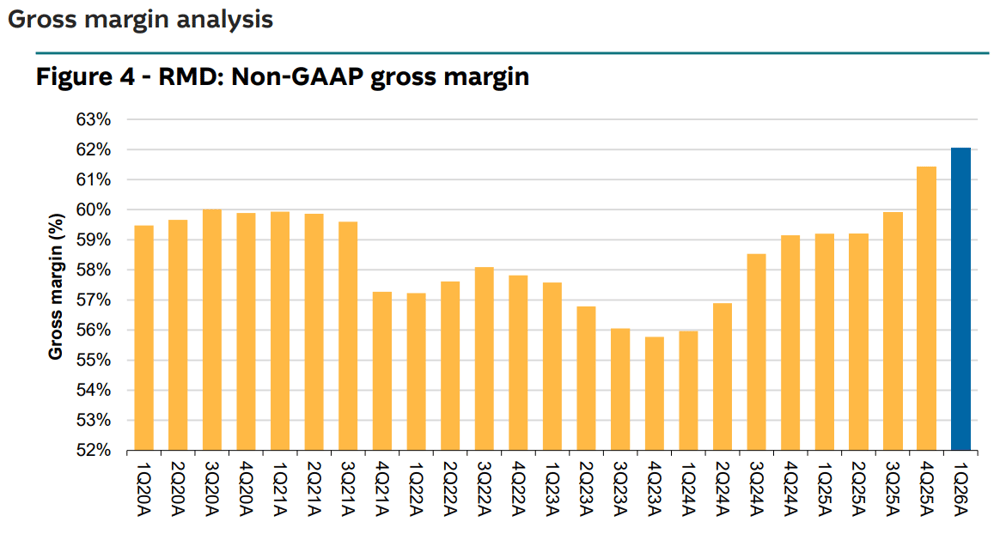

ResMed’s gross margin has climbed 62.3%, while investors are still valuing the stock on a low 20s P/E, well below 2020-21 peak.

Source: Shutterstock

Mentioned

ResMed (RMD) reported its Q2 FY26 result this morning, extending its run of operating leverage through the December quarter. The sleep apnea and respiratory care group delivered double digit revenue growth and another step up in gross margin, despite valuations remaining well below its 2020-21 peak.

Key Numbers

Revenue up 11% to $1.42bn vs $1.40bn ests (1.4% beat)

Non-GAAP gross margin up 310 bps to 62.3% vs. 61.9% ests (40 bp beat)

Operating profit up 19% to $517.2m vs $503.9m ests (2.7% beat)

EPS ex-item sup 16% to $2.81 vs $2.74 ests (2.6% beat)

Operating cash flow of US$340 million

ResMed’s Chairman and CEO, Mick Farrel said the gross margin lift was primarily driven by manufacturing and logistics efficiencies and lower component costs.

He said “these results reflect strong ongoing demand for our market-leading sleep and respiratory care devices, as well as the growing impact of our digital health ecosystem that spans more than 140 countries."

Yet despite the continued margin expansion, the stock’s valuation still screens below its long-term average, according to Morgan Stanley.

.png)

Source: Morgan Stanley, November 2025

The company's profit margins improved even though they spent more money on operations. Selling, general, and administrative expenses (SG&A) increased from 18.8% of revenue last year to 19.6% this year, driven by the VirtuOx acquisition plus continued spending on marketing and technology.

A Macquarie report from November 2025 noted gross margins to “remain at 62%” through the remainder of FY26.

Source: Macquarie, November 2025

ResMed’s Q2 non-GAAP gross margin of 62.3% suggests the company is already operating around that projected FY26 level. Meanwhile, the stock's forward price-to-earnings is sitting in the low 20s, below its historical average of 29x and well-below pandemic peaks of 45x.

In short, ResMed is churning higher margins, but the market is still valuing it closer to the lower end of its historical range.

ResMed returned capital during the quarter, paying US$88 million in dividends and buying back 704,000 shares for US$175 million. The company’s stock price was up 4.2% to $37.93 in morning trade.