RBA set to hike again as energy shock clouds ASX 200 outlook

Morgan Stanley forecasts an RBA hike today, warning of de-rating risk for banks, weaker housing prices and margin pressure for retailers.

Source: Shutterstock

KEY POINTS

- Morgan Stanley expects the RBA to hike rates by 25 bps to 4.1% this week, with market pricing above 70% for a back-to-back hike driven by an energy supply shock that could add around 70 basis points to headline inflation.

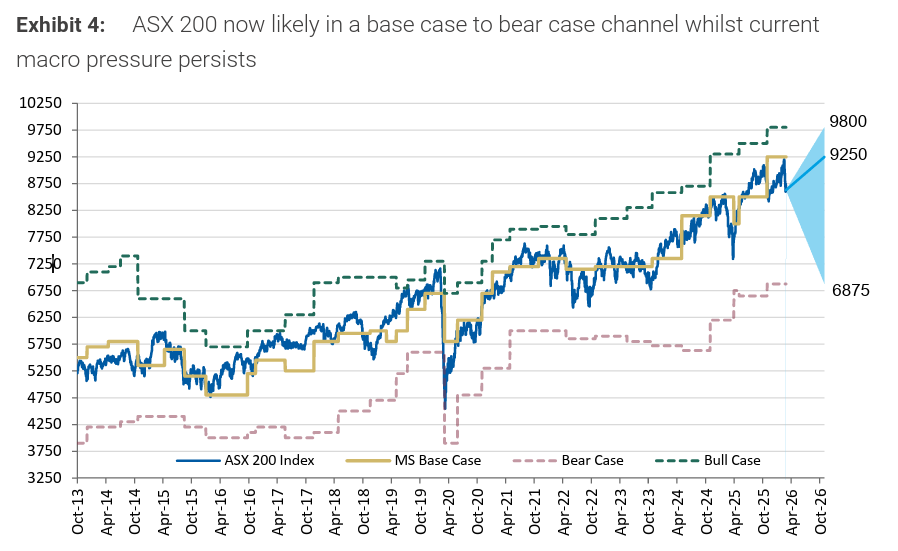

- The ASX 200 is trading at 17x forward earnings, above its long-run average of 14.8x, and in a worst case scenario, Morgan Stanley sees a potential 34.5% decline to its bear case valuation.

- Banks, consumer-facing businesses, and housing-exposed stocks carry the most downside risk.

It's getting harder to make the bull case for Australian equities, with the RBA set to hike rates for a second consecutive meeting, alongside a historic energy supply shock that's making the inflation problem worse. Morgan Stanley warns the combination could push the ASX 200 materially lower from here.

More rate hikes

The energy supply shock linked to the Iranian conflict has driven market pricing for a back-to-back hike above 70%, and the RBA appears increasingly unwilling to look through supply-side inflation pressures. Morgan Stanley estimates that oil at US$100 per barrel would add approximately 70 basis points to headline inflation, at a time where the RBA's June 2026 forecast was already sitting at 4.2%.

"The RBA is not well placed to look through a supply shock. Inflation was already above target and had risen further over the past six months, which was the key catalyst for the RBA to shift back to tightening at the February meeting," notes Morgan Stanley.

The analysts expect the RBA to say that it is willing to accept slower growth in exchange for bringing inflation back to target faster. A contractionary tilt from monetary policy is also likely to be reinforced by fiscal consolidation in the upcoming Federal Budget.

Where the ASX stands

The ASX 200 is down approximately 1.5% year-to-date, and 6.5% from early March highs. The 12-month forward price-to-earnings multiple currently sits at 17x, above the long-run average of 14.8x. Though consensus expects some solid earnings growth over the next two years, with EPS growth of 13.9% for FY26 and 9.4% for FY27.

Morgan Stanley draws a pointed comparison to the April 2025 sell-off, when the index touched 7,343 and fell 8.2% peak-to-trough amid tariff uncertainty. That period, however, was cushioned by low inflation and accommodative policy. This time, the macro backdrop is tighter, the policy response is restrictive, and Morgan Stanley sees a further 34.5% downside to their bear case valuation from current levels if conditions deteriorate.

Source: Morgan Stanley | Data as of 12 March 2026

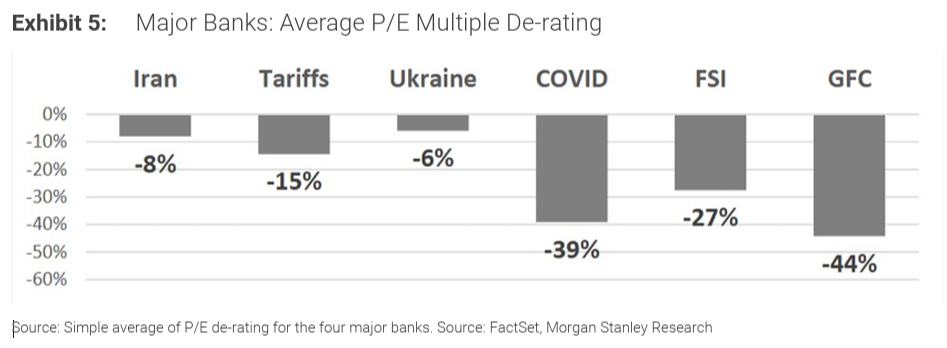

A potential de-rating for banks

Major bank share prices have fallen just 2-3% from their 25 February peak, a rather modest re-rating relative to previous risk-off episodes. Morgan Stanley warns that because today's starting valuation (price-to-earnings of ~20x and price-to-book of around 2.4x) is materially higher, it leaves more room to fall should conditions deteriorate.

The investment bank flags that current geopolitical and market conditions increase the likelihood of further de-rating triggers, including slowing credit growth, more competition, and execution risk.

Consumers at risk

The latest February reporting season showed that consumers finished 2024 in reasonable shape, but with clear signs of sequential slowing through December and January. Shoppers are becoming more selective on value, and volume growth is proving difficult to sustain without price reinvestment. Promotional intensity is rising across various formats, and retailers are increasingly explicit about the trade-off between protecting margins and defending market share.

Another rate hike, combined with fiscal tightening, is expected to intensify these pressures, most likely at the expense of earnings margins in discretionary categories.

Housing slowdown

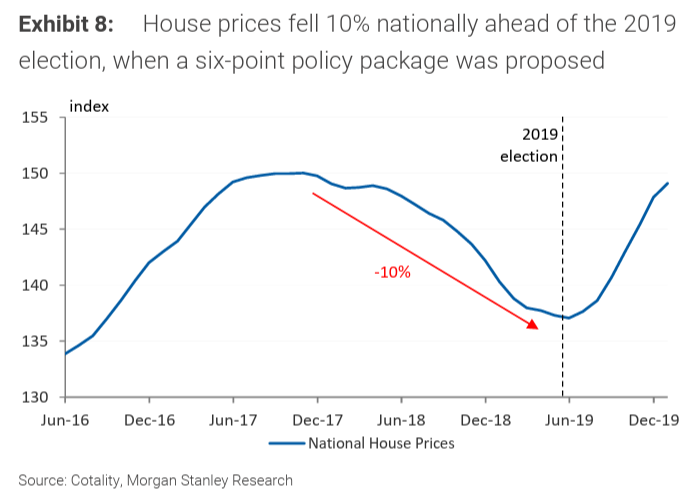

The housing market has been strong over the past 12 months, but the RBA's hawkish shift has already begun to show up in the data, where sentiment measures have softened, auction clearance rates are lower, and the pace of price increases has slowed.

Compounding the rate pressure, the government is considering changes to the capital gains tax discount and negative gearing rules. Morgan Stanley points to the 2019 federal election cycle as a relevant reference point. During this time, similar policies were proposed and national house prices fell 10%, without any change in the cash rate.

Bottom Line

The combination of a tightening RBA, elevated equity valuations, a slowing consumer, housing market softness, and an energy-driven inflation shock presents a more difficult environment for Australian equities. Morgan Stanley warns that key sectors like banks, consumer-facing businesses, and housing-exposed stocks are all carrying meaningful downside risk under a scenario where the energy supply disruption lasts much longer than expected.