Path to $200 WiseTech Global share price is becoming clearer says Morgan Stanley

Morgan Stanley reiterates its bullish view on WiseTech Global, discussing the major drivers for the stock to potentially reach $200/share.

Source: Shutterstock

Mentioned

KEY POINTS

- WiseTech Global (ASX: WTC) is one of the world’s leading logistics software companies, and a major ASX technology sector success story

- The company held its annual Investor Day this week, outlining its plans for achieving its earnings growth and profitability targets for 2025 and beyond

- We investigate a major broker’s rationale for plotting a path to $200 for WiseTech’s share price, as well as how other brokers viewed the company’s Investment Day.

Morgan Stanley has reaffirmed its bullish recommendation on WiseTech Global (ASX: WTC), maintaining a 12-month price target of $160 per share. This implies a tidy 25-30% upside compared to the stock’s $129.58 close on Wednesday. But, it could get substantially better if the broker’s “bull case” of $200 per share is achieved (55-60% upside).

While acknowledging the potential for short-term volatility, Morgan Stanley identifies four key reasons supporting its optimism. We review these as well as the key catalysts the broker thinks could help achieve its bull case target, and the main risks to the thesis.

4 reasons Morgan Stanley rates WiseTech as OVERWEIGHT

Morgan Stanley breaks down its reasoning for their bullish call on WiseTech into four key areas:

1. Driving Customer Profitability and Growth

WiseTech’s software solutions, led by its flagship CargoWise platform, are delivering measurable cost savings and efficiencies for its users. The company’s Investor Day, held on Tuesday, highlighted how the upcoming CargoWise Transport Optimization ("CTO") product is expected to further reduce users’ costs by around 30-50%.

Beyond cost savings, Morgan Stanley underscores that WiseTech's software enables users to improve their profit margins, reduce headcount, and accelerate revenue growth, both organically and via M&A.

2. Strengthening Leadership Position and Competitive Moat

WiseTech’s growing product suite and the increasing “network benefits” (i.e., referrals for new business from existing customers) from its vertically integrated solutions make it a clear leader in logistics software.

The company plans to reinvest 33% of its revenues in R&D, supporting new product launches and expansion into adjacent markets. This aggressive investment strategy underpins Morgan Stanley’s projected 26% revenue compound annual growth rate (CAGR) through FY27, which outpaces peers.

3. Significant Total Addressable Market (TAM) Opportunity

Although WiseTech did not provide its own TAM estimates, Morgan Stanley doubled its assessment of the company’s current TAM, to US$20 billion. Looking forward, the broker forecasts a 15% CAGR in TAM out to 2030, when it’s projected to reach US$40 billion.

4. Proven Growth and Profitability Record

Since its IPO in 2016, WiseTech has consistently exceeded consensus expectations. For instance, from FY16 to FY24, WiseTech achieved 32% CAGR in revenue (versus the broker’s forecast of 22%) and a 40% CAGR in earnings before interest, tax, depreciation and amortisation (“EBITDA”) (versus the broker’s forecast of 32%).

In FY24, EBITDA rose 28% year-on-year to $496 million, while free cash flow grew by 14% to $333 million. Morgan Stanley cites this track record as giving it substantial confidence in WiseTech’s ability to sustain long-term earnings growth.

Upcoming catalysts for WiseTech shares

Morgan Stanley highlights several key catalysts that could drive WiseTech’s share price in the near term:

Product Launches: The rollout of three major products, ComplianceWise and CargoWise Next in the current half, and CTO in the first half of next year.

H1 FY25 Results: WiseTech is due to report its first-half FY25 results in February 2025. These results, and updated guidance for the full year, will be another critical event that could sway investor sentiment.

Management Appointments: The announcement of a permanent CEO and CFO will be closely watched, as it should stabilise the current leadership uncertainty following recent management and board changes.

Risks to Morgan Stanley’s “path to $200” thesis

Despite its confidence, Morgan Stanley outlines several risks that could challenge its optimistic outlook:

Delays or Weak Uptake of New Products: Any delays in launching the three major software products or disappointing adoption rates could undermine revenue growth expectations.

Management Transition Risks: Recent management and board changes add uncertainty to the company’s leadership effectiveness, particularly with respect to recent c-suite indiscretions.

Competitive Pressures: Changes in the competitive landscape, such as increased competition from other cloud-based software providers, could limit WiseTech’s ability to win new customers and expand its market share.

Macroeconomic Headwinds: A downturn in global trade, freight volumes, or economic growth could negatively impact demand for logistics solutions, posing a risk to WiseTech’s earnings.

Valuation Sensitivity: At high valuation multiples, WiseTech’s shares are vulnerable to broader market sell-offs, particularly in the high-flying US technology sector. This factor also makes it more sensitive to “negative news that could trigger a de-rating”. Here, Morgan Stanley points out failure to achieve cost efficiencies and a stated improvement in EBITDA margins.

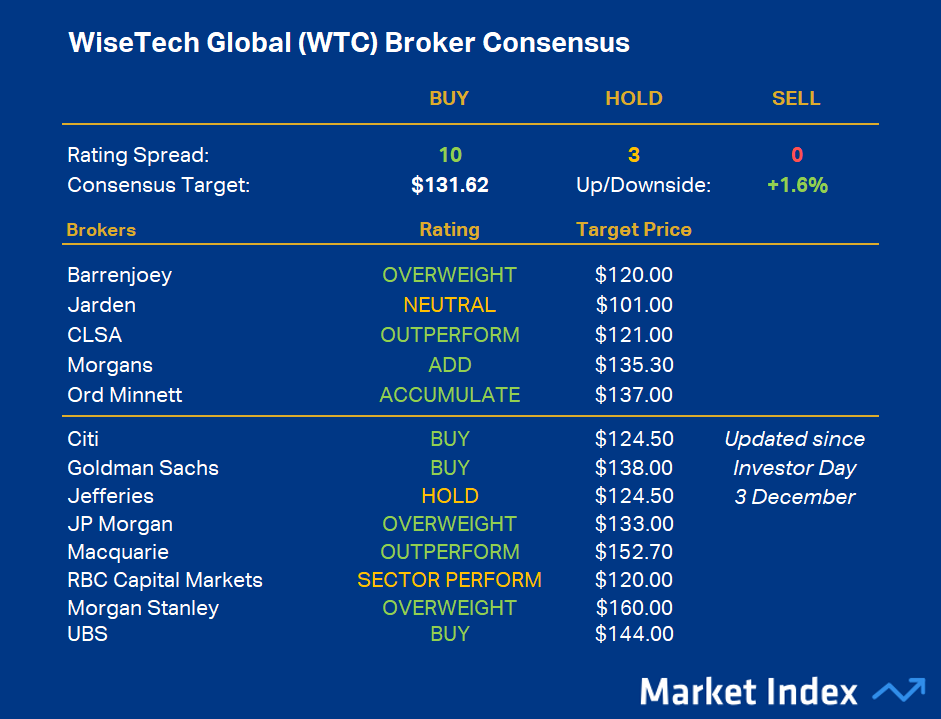

WiseTech Global Broker Consensus

Let’s take a quick look at the latest Broker Consensus for WiseTech following its Investor Day earlier in the week. All broker ratings and targets are taken from broker research notes collected since July 1 for currency.

To obtain a stock’s Broker Consensus Rating, we assign a value of +1 to any rating better than HOLD/NEUTRAL/MARKETWEIGHT, a value of 0 for any rating equivalent to HOLD/NEUTRAL/MARKETWEIGHT, and a value of -1 to any rating worse than HOLD/NEUTRAL/MARKETWEIGHT.

We then take the average of all assigned rating values and assign a Broker Consensus Rating of BUY to values greater than +0.5, a rating of HOLD for values between -0.5 and +0.5, and a rating of SELL for values less than -0.5.

%20Broker%20Consensus_UPDATED.png)

WiseTech Global Broker Consensus (upside / downside as at close price for WTC Wednesday 4 December of $129.58) (click here for full size image)

{kind=link}

WTC’s broker consensus rating is +0.75, resulting in a Broker Consensus Rating of BUY. Its Consensus (average) target price is $131.62. This suggests brokers collectively believe the stock is around 1.6% undervalued based upon the closing price on Wednesday 4 December of $129.58.