Oz Minerals contemplates $205m copper buy

Oz Minerals is focused on adding multiple options, like Kalkaroo, to its growth pipeline

Mentioned

KEY POINTS

- Oz Minerals is looking to acquire Havilah’s 100% owned Kalkaroo copper-gold-cobalt deposit

- Kalkaroo is understood to be one of the country's largest undeveloped open pit copper-gold deposits

- By taking projects from an early study phase through development and into operation, Oz Minerals plans to unlock significant value for stakeholders

Oz Minerals Limited (ASX: OZL) recovered some lost ground at the open, up 1.23% - after falling 15% since mid-April - following revelations this morning that the copper, gold, and nickel miner has identified a new $205m project to add to its portfolio.

Subject to 18 months of assessment, Oz Minerals and Kalkaroo project owner Havilah Resources (ASX: HAV) have signed a term sheet and options deal to give the former sufficient time and space to kick the tyres on such a deal before a 100% acquisition.

Assuming the deal goes ahead, it provides a deferred contingent consideration of $65m, upon a 30% uplift in Kalkaroo’s Measured and Indicated Resource estimate plus a copper price linked contingent payment in each year of production up to a maximum cumulative amount of $135m.

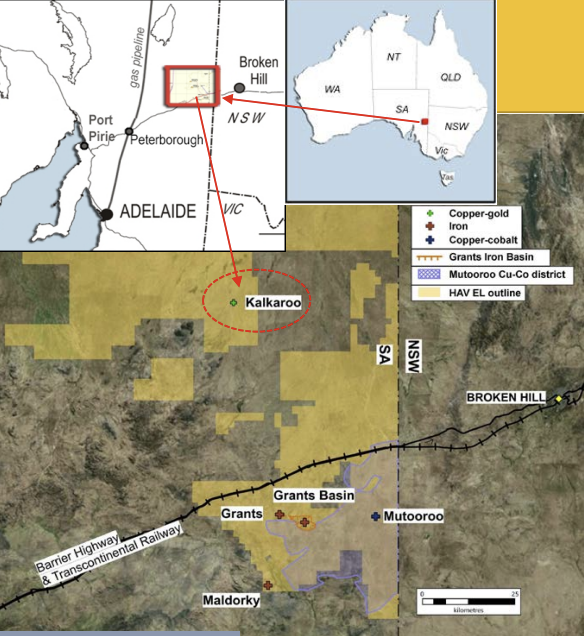

Kalkaroo copper-gold-cobalt deposit

Havilah’s 100% owned Kalkaroo copper-gold-cobalt deposit, contains JORC Mineral Resources of 1.1m tonnes of copper, 3.1m ounces of gold and 23,200 tonnes of cobalt.

It has an open pit JORC Ore Reserve of 100.1m tonnes of which 90% is in the Proved category.

Kalkaroo is at pre-feasibility study stage and is understood to be one of the country's largest undeveloped open pit copper-gold deposits.

Transaction overview

Oz Minerals will pay Havilah $1m per month during the option and alliance period, with 50% of the payments directed towards Havilah identifying and advancing nearby exploration opportunities within the in the copper-rich Curnamona Province of north-eastern South Australia.

Including the monthly payment, Oz Minerals has earmarked up to $76m during the 18 months to undertake studies and for exploration activities at the Kalkaroo project and on alliance activities.

The aim of the study is to improve Oz Minerals understanding and confidence in the project and will include an infill drilling program to confirm the current Mineral Resource estimate, prior to deciding whether to acquire the Kalkaroo project or not.

Unlocking significant value

Oz Minerals CEO Andrew Cole told investors that by taking projects from an early study phase through development and into operation, the company plans to unlock significant value for stakeholders.

"Something we have demonstrated with Carrapateena, now in its third year of operation, and continue to show with West Musgrave as we approach a final investment decision on the project later this year," he adds.

“We remain focused on adding multiple options, like Kalkaroo, to our growth pipeline.”

Oz Minerals share price over three months.

Shortly after the open this morning Havilah Resources share price was up around 97% to $0.35.

Havilah Resources: A three month share price snapshot.

What brokers think

Consensus on OZ Minerals is Hold.

Based on Morningstar’s fair value of $22.86, the stock appears to be undervalued.

Based on the brokers that cover Oz Minerals (as reported on by FN Arena) the stock is trading with 18.7% upside to the target price of $25.46.

Despite a more challenging outlook for 2022 production and costs, Goldman Sachs (22/4/22) rates Oz Minerals a Buy based on valuation – trading below NAV at 0.9x, a positive view on copper – US$5.3/lb price forecast for 2022, and production growth outlook – increasing production by around 50% over the next five years. (Price target $27.50).

Based on concerns over cost inflation and "frothy markets", Ord Minnett (04/05/22) retains a Lighten rating and price target of $22.20.

Citi remains bullish (26/04/22) on copper for 2022 with global supply appearing squeezed and retains a Buy rating and $30.50 target.

To reflect the production in the March quarter, Credit Suisse lowered FY22 net profit estimates by -5% (26/04/22) and retains Underperform rating and target of $21.