Mortgage pain warning as oil price surge has markets expecting two RBA rate hikes by October

Oil has surged above US$100 and markets now see two RBA rate hikes by October. Is this be the prick that bursts Australia’s housing bubble?

Source: Market Index using ChatGPT 5.2

KEY POINTS

- Oil prices have surged more than 25% amid escalating Middle East tensions, reviving fears of another global energy shock and the inflation pressures that historically follow major supply disruptions.

- Interest rate markets have responded swiftly. ASX cash rate futures now imply the RBA could lift the official cash rate to around 4.35% by October, effectively pricing two additional rate hikes in the months ahead.

- If markets are right, mortgage holders may face renewed repayment pressure. This article explains why oil shocks matter for inflation, how traders are pricing the RBA outlook, and what it could mean for Australia’s economy and housing market.

Oil prices are surging, markets are scrambling to reassess inflation — and the humble Australian mortgage holder may be about to discover just how connected global geopolitics has become to their monthly repayments.

Over the past two weeks, the conflict in the Middle East has delivered a shock to global energy markets. Oil has surged more than 25% in a matter of days, a move that immediately raises alarm bells for central banks already fighting stubborn inflation.

But markets are not just reacting to the spike itself. They are reacting to what history suggests comes next.

New research from Canaccord Genuity shows that sharp oil shocks like the one unfolding today rarely fade quickly. Instead, they tend to persist — and often escalate — with significant consequences for inflation, interest rates, and ultimately economic growth.

And if the latest market pricing is right, the Reserve Bank of Australia (“RBA”) may soon face an extraordinarily difficult decision about interest rates.

Oil shocks rarely fade quickly

According to the latest research from Canaccord Genuity, the current oil spike is occurring against a highly sensitive geopolitical backdrop [1].

Roughly 20 million barrels of oil per day — about 25% of global seaborne oil trade — passes through the Strait of Hormuz, one of the world’s most critical energy choke points. Any disruption to shipping in the region would have immediate consequences for global supply and pricing.

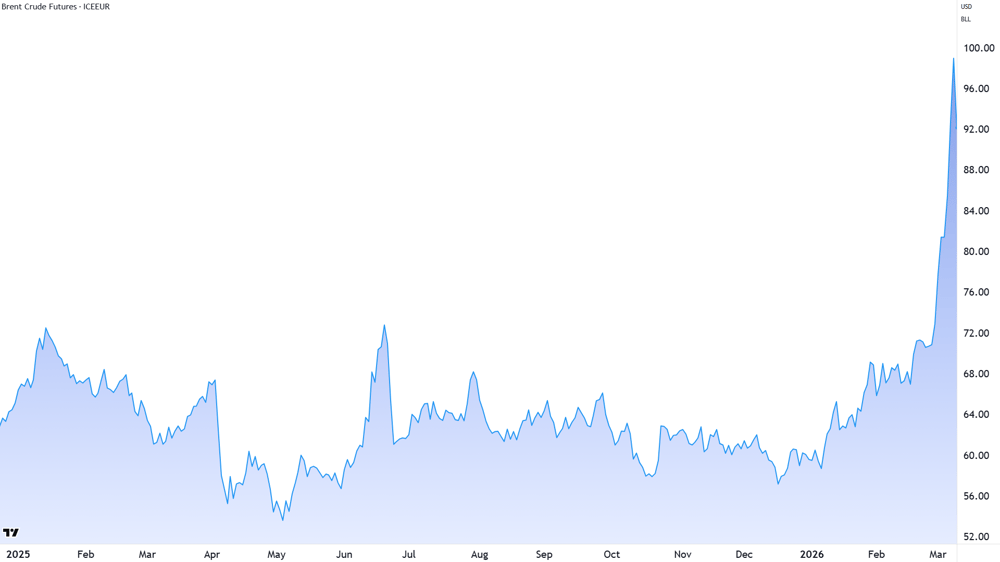

That risk has already begun to manifest in crude oil prices, as regional producers warn of possible disruptions and the prospect of prolonged military engagement. The price of the benchmark Brent crude oil futures contract has surged more than 25% to over US$100 per barrel in just a week.

Benchmark Brent crude oil futures NYMEX as at 10 pm AEDT, 10 March

History suggests that may only be the beginning. Canaccord analysed previous instances since 1996 where crude oil jumped more than 25% within a single week. In four out of five cases, oil prices were still trading significantly higher one year later.

In other words, markets may be dealing with a shock that is not temporary, but structural. That matters enormously for the global inflation outlook.

Energy costs flow directly through to transportation, manufacturing, and food prices. Canaccord estimates that a 25% surge in crude oil could translate into 25 to 50 basis points of additional pressure on inflation gauges like the consumer price index (“CPI”) in the months ahead.

And that’s precisely the kind of development central banks fear the most — an external supply shock that forces them to tighten policy even as economic growth slows.

Markets now see at least two rate hikes ahead

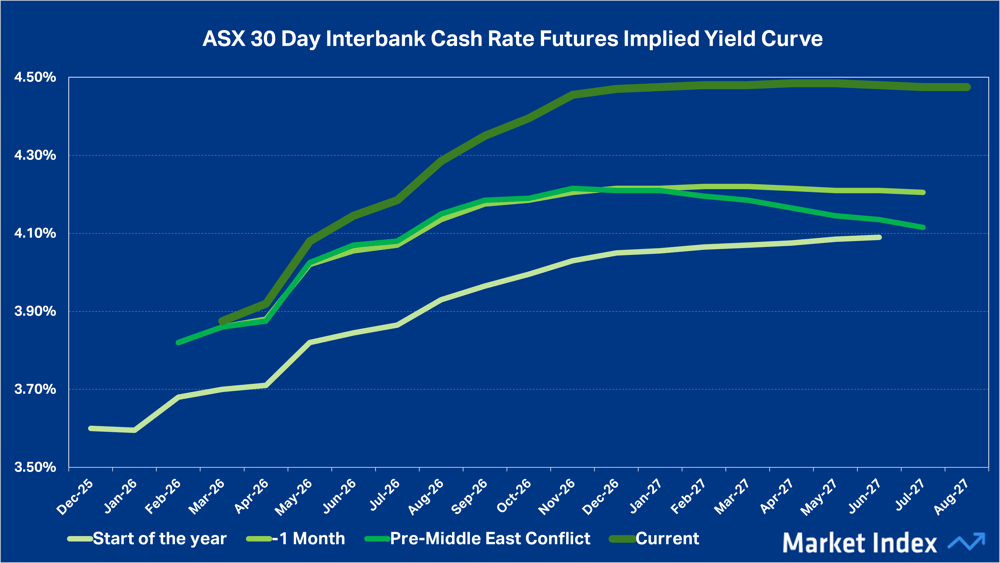

Financial markets have wasted no time adjusting their expectations for inflation and official interest rates. Data from the ASX 30 Day Interbank Cash Rate Futures market — the key instrument traders use to bet on the future path of RBA policy — shows a sharp upward shift in rate expectations since the Middle East conflict erupted.

The RBA’s official cash rate currently sits at 3.85%, following its most recent increase from 3.60% in early February. But futures markets now forecast last month’s hike will go down as the first in a potentially extended RBA hiking cycle.

ASX 30 Day Interbank Cash Rate Futures as at market close 9 March. The implied yield curve has shifted sharply higher since the start of the year, with the current curve (dark green) spiking higher in the wake of the Middle East conflict. By October, it reaches 4.35%, indicating markets are pricing roughly 50 basis points of additional RBA tightening, equivalent to two 25 basis point rate hikes.

Current market pricing suggests the cash rate could reach around 4.35% by October this year, effectively signalling two additional 25 basis point rate hikes over the coming months.

Beyond that, markets see the tightening cycle extending further. The implied peak in the futures curve sits at approximately 4.48% by August 2027 — about 62.5 basis points above the current cash rate.

In simple terms, traders are now betting that the RBA will be forced to raise interest rates up to three times again to counter the inflationary impact of higher energy prices.

For the average mortgage holder, that may sound like financial jargon. But the implications are straightforward: higher interest rates mean higher borrowing costs across the economy — from business lending to household mortgages.

A highly leveraged housing market

Few parts of the economy are more sensitive to interest rates than housing. Australia is one of the most indebted household sectors in the world, largely because of its reliance on mortgage borrowing.

Household debt now sits at roughly 112% of GDP, one of the highest ratios globally and well above many advanced economies. Measured another way, the average Australian household owes around twice its annual disposable income in debt, the vast majority of which is tied to housing. That leverage magnifies the impact of interest rate changes.

In recent years, surging house prices have also forced borrowers to take on larger loans relative to income. Some estimates suggest new mortgage repayments now consume around 45% of the typical household’s pre-tax income, nearly double the level seen only five years ago.

This leaves the system particularly sensitive to even small changes in official interest rates. If the RBA were to deliver the hikes now priced into markets, mortgage repayments would rise further — tightening financial conditions for households already grappling with high living costs.

For mortgage holders, the risk is a painful double whammy: even greater pressures on living costs due to higher energy prices, plus higher mortgage repayments if the RBA responds with further rate hikes. A sharp pullback in discretionary spending could then ripple through the economy, squeezing business revenues and ultimately lifting unemployment.

Any deterioration in the labour market would place further pressure on highly leveraged households and could prove to be the pin that pops Australia’s housing market bubble.

A delicate balancing act

The situation remains highly fluid. If tensions in the Middle East ease and oil prices retreat, the inflation shock may fade before central banks have to act. But if energy prices remain elevated — as history suggests they often do after major supply shocks — policymakers may have little choice but to respond.

For the RBA, that would mean confronting one of the most uncomfortable scenarios in monetary policy: raising interest rates even as economic momentum weakens. Markets, for now, are betting that the inflation threat will win that argument.

One thing is clear: the ripple effects of an oil shock thousands of kilometres away are already washing up on Australia’s financial shores. Both mortgage holders and investors may want to hope for the best, but plan for the worst.

[1] Source: Canaccord Genuity, Strategic Insights – Light at the other end of the Iran tunnel, but it may have just become longer, 9 March 2026.