Morning Wrap: ASX 200 to rise, S&P 500 at record highs + Copper, nickel and lithium stocks set for further gains

ASX 200 futures are up 29pts (+0.33%) as of 8:30 am AEDT.

In this article

ASX 200 futures are up 29pts (+0.33%) as of 8:30 am AEDT.

In a nutshell:

S&P 500 and Russell 2000 closed at record highs, while the Nasdaq is within 2% of 29-Oct-25 all-time high

Commodity prices bounced after Thursday's broad pullback, notable gains from nickel (+4.3%), silver (+3.8%), copper (+1.4%) and gold (+0.70%)

US December nonfarm payrolls rose less than expected, unemployment rate slipped to 4.4% vs. 4.5% consensus

Let's dive in.

Overnight Summary

Name | Value | % Chg |

|---|---|---|

Major Indices | ||

S&P 500 | 6,966 | +0.93% |

Dow Jones | 49,504 | +1.08% |

NASDAQ Comp | 23,671 | +1.18% |

Russell 2000 | 2,624 | +2.99% |

Country Indices | ||

Canada | 32,613 | +1.22% |

China | 4,120 | +3.82% |

Germany | 25,262 | +1.58% |

Hong Kong | 26,232 | -0.44% |

India | 83,576 | -2.18% |

Japan | 51,940 | +0.21% |

United Kingdom | 10,125 | +1.20% |

Name | Value | % Chg |

|---|---|---|

Commodities (USD) | ||

Gold | 4,510.61 | +0.72% |

Copper | 5.8555 | +1.90% |

WTI Oil | 59.12 | +2.35% |

Currency | ||

AUD/USD | 0.6681 | -0.09% |

Cryptocurrency | ||

Bitcoin (USD) | 90,535 | +0.12% |

Ethereum (AUD) | 4,652 | +0.75% |

Miscellaneous | ||

US 10 Yr T-bond | 4.171 | +0.14% |

VIX | 14.49 | -2.75% |

US Sectors

Sector | % Chg |

|---|---|

| Consumer Discretionary | +3.76% |

| Materials | +3.59% |

| Consumer Staples | +2.45% |

| Communication Services | +1.64% |

| Health Care | +1.46% |

| Industrials | +1.35% |

Sector | % Chg |

|---|---|

| Real Estate | +0.22% |

| Information Technology | +0.18% |

| Utilities | -0.45% |

| Energy | -0.53% |

| Financials | -0.77% |

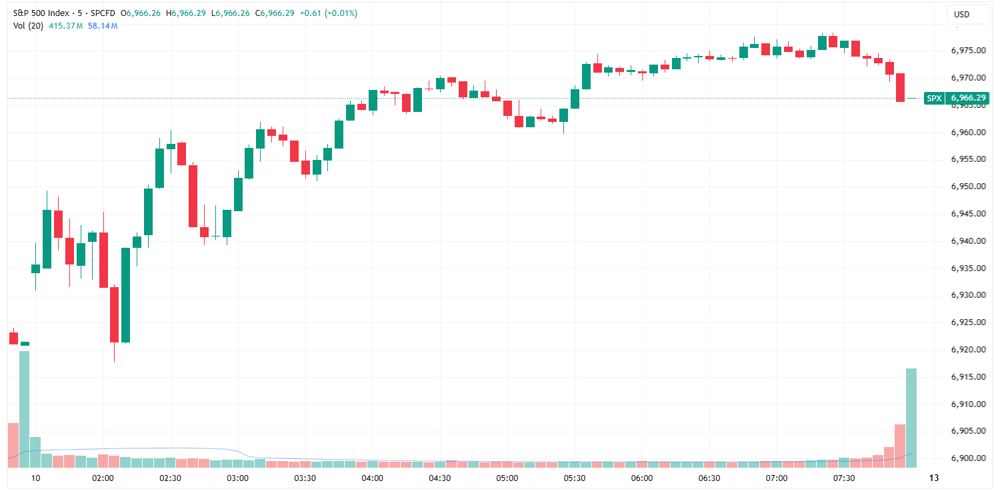

S&P 500 SESSION CHART

S&P 500 trended higher to close near best levels (Source: TradingView)

OVERNIGHT MARKETS

Major US benchmarks higher and closed near best levels

S&P 500 and Russell closed at record highs, Nasdaq less than 2% from record highs

US weekly recap: Russell 2000 (+4.62%), Dow (+2.32%), Nasdaq (+1.88%), S&P 500 (+1.57%)

Commodity prices bounced after Thursday’s broad pullback, with nickel up 4.3% to US$17,689/t, copper up 1.4% closing just shy of US$6.0/lb, aluminium up 1.9% to the highest since Apr-22 and silver up 3.8%, capped off 9.7% weekly gain

Market’s path of least resistance remains higher off the back of more reasonable positioning and sentiment, a broadening rally and cyclical outperformance, Trump focus on affordability via rates, housing and mortgages and cooling Venezuela tensions

Mag-7 dominance may be fading as earnings growth slows and AI capex continues to soar (BBG)

Companies tap bond market at fastest pace since pandemic, setting up record year of debt sales (FT)

Hedge funds looking for opportunities around Venezuela, Cuba, Greenland as Trump seeks to dominate Western hemisphere (WSJ)

Asian tech stocks rally to start the year on AI demand optimism and more reasonable valuations (BBG)

Many investors betting on further gains in gold, flagging waning confidence in developed market currencies and further central bank buying (BBG)

Investors pivot out of tech into cyclicals and defence as economic reacceleration hopes drive broadening market rally (WSJ)

STOCKS

Merck in talks to buy Revolution Medicines for up to $32bn (FT)

Walmart and Google announce collaboration to search and buy products through Gemini (CNBC)

Boeing on track to report highest number of deliveries since 2018, set to ramp output further (CNBC)

TSMC revenue beats estimates, bolstering hopes for continued global AI spending in 2026 (BBG)

Nvidia-backed Lambda seeks $350m pre-IPO funding to support 2H26 IPO plans (TI)

J&J strikes deal with Trump to lower drug prices, gains tariff exemptions (WSJ)

GM discloses $7bn hit from EV transition and China restructuring challenges (FT)

TARIFFS

Importers prepare for possible $150bn tariff refund, pending Supreme Court ruling on tariffs (RT)

Taiwan-US trade surplus to hit record high as trade deal negotiations continue (BBG)

CENTRAL BANKS

BOJ to raise growth forecasts at January meeting due to PM Takaichi stimulus package (BBG)

GEOPOLITICS

Trump cancels second Venezuela attack, citing improved cooperation (FT)

Venezuela does not give Beijing precedent over Taiwan, 'but it is up to Xi', says Trump (RT)

Nearly 20 oil execs to meet Trump about rebuilding Venezuela's energy sector, Trump flags $100bn investment (BBG)

Trump signs executive order to safeguard Venezuelan oil revenue in US Treasury account (BBG)

ECONOMY

US December nonfarm payrolls increased by 50,000 vs. 60,000 consensus, unemployment rate was 4.4% vs. 4.5% consensus (BBG)

US January consumer sentiment improves to 54.0 vs. 52.9 in December and 53.5 consensus, highest reading since September and up for a second straight month (BBG)

Trump says he will cap on credit card rates of 10% for one year (POL)

China's CPI accelerates to 0.8% year-on-year, led by food costs, but deflationary risks persist (BBG)

Industry ETFs

Name | Value | % Chg |

|---|---|---|

Commodities | ||

| Silver | 72.38 | +3.83% |

| Strategic Metals | 84.98 | +3.07% |

| Copper Miners | 77.54 | +2.54% |

| Uranium | 50.31 | +1.62% |

| Gold Miners | 92.56 | +1.11% |

| Lithium & Battery Tech | 68.21 | +0.19% |

| Steel | 87.715 | -0.63% |

Industrials | ||

| Construction | 99.0117 | +3.18% |

| Aerospace & Defense | 232.97 | +2.44% |

| Global Jets | 29.47 | +1.62% |

| Agriculture | 25.78 | -0.88% |

Healthcare | ||

| Biotechnology | 172.39 | +0.08% |

Name | Value | % Chg |

|---|---|---|

Cryptocurrency | ||

| Bitcoin | 12.52 | -0.71% |

Renewables | ||

| Hydrogen | 36.09 | +2.39% |

| CleanTech | 57.47 | +1.58% |

| Solar | 50.3 | -0.20% |

Technology | ||

| Semiconductor | 328.78 | +2.88% |

| Electric Vehicles | 31.83 | +1.43% |

| Robotics & AI | 38.23 | +1.33% |

| Video Games/eSports | 104.16 | +0.44% |

| E-commerce | 33.99 | +0.28% |

| Cybersecurity | 30.67 | +0.03% |

| FinTech | 30.42 | -0.23% |

| Cloud Computing | 22.58 | -0.27% |

| Sports Betting/Gaming | 20.52 | -0.63% |

ASX TODAY

ASX 200 set to open higher, a rather encouraging lead from Wall Street that featured solid breadth and Materials as the best performing S&P 500 sector. Price action continues to be rather dicey (e.g. XJO closed -0.03% on Friday vs. intraday high of +0.48%). But the index continues to trade on the right side of key moving averages (above the 20, 50 and 200 day) and still marking higher highs.

Boss Energy holder Sprott Inc. increases holding to 12.1% from 9.1% (BOE)

Light & Wonder to compensate Aristocrat Leisure for $127.5m for infringement of IP relating to Dragon Train game (LNW)

Rio Tinto and Glencore to hold buyout talks to create $207bn mining giant (FT)

Southern Cross Media holder 19 Cashews lowers holding from 14.4% to 7.5% (SXL)

WHAT TO WATCH TODAY

Homebuilders: SPDR S&P Homebuilders ETF up 5.1% overnight, now up 9.1% in the last two sessions to the highest since 19-Sep-25. Trump called on Fannie and Freddie to buy US$200bn in mortgages, driving broad rally for housing-related stocks. NYSE-listed James Hardie shares up 6.1% overnight to highest since 20-Aug-25, likely to see strength follow through today for other US housing exposed names like REH, RWC, GWA etc.

Miner gains: Broad-bounce for most commodities overnight after last week's pullback (e.g. PLS -3.1% and NIC -4.6% on Friday vs. Rare Earth/Strategic Metals and Nickel Miners ETF both up 3.0% overnight).

BROKER MOVES

Ramelius Resources upgraded to Buy from Neutral; target up to $5.35 from $4.30 (GS)

Vault Minerals downgraded to Neutral from Buy; target up to $6.30 from $5.27 (GS)

Key Events

Stocks trading ex-dividend:

Mon 12 Jan: Dominion Income Trust (DN1) – $0.561

Tue 13 Jan: Sandon Capital (SNC) – $0.005

Wed 14 Jan: Tower (TWR) – $0.144

Thu 15 Jan: None

Fri 16 Jan: None

Other ASX corporate actions today:

Dividends paid: None

Earnings: None

IPOs: Unity Metals (UM1) at 12:00 pm

AGMs: None

Economic calendar (AEDT):

11:30 am: ANZ-Indeed Job Ads (Dec)