Morgan Stanley cuts gold target to US$5,200 as yields take control and Fed rate cut hopes fade

Morgan Stanley says the brutal six-week selloff in gold was a supply shock story. Now the investment bank has cut its target.

Source: Shutterstock

Mentioned

KEY POINTS

- Gold has declined ~8% since the Middle East conflict began on 28 February, performing worse than equities, bonds and Treasuries.

- The selloff reflected a supply shock that lifted inflation risk and pushed out Fed rate cut expectations, with gold re-establishing its historical inverse correlation with real yields after years of breakdown.

- Morgan Stanley has cut its second-half 2026 gold target to $5,200/oz from a prior bull case of $5,700/oz, with potential Fed cuts in September and December the key catalyst for any recovery from here.

Gold has dropped around 8% since the Middle East conflict began on 28 February and it hasn't bounced back the way investors expected. At the same time, equity have powered ahead, with the S&P 500 and Nasdaq rallying past pre-conflict levels to fresh all-time highs.

Morgan Stanley has cut its second-half 2026 gold target to US$5,200/oz from a prior bull case of US$5,700/oz. The investment bank argues the case for owning gold has shifted, and investors who bought it as a geopolitical hedge are getting an expensive lesson in what kind of shock the metal actually protects against.

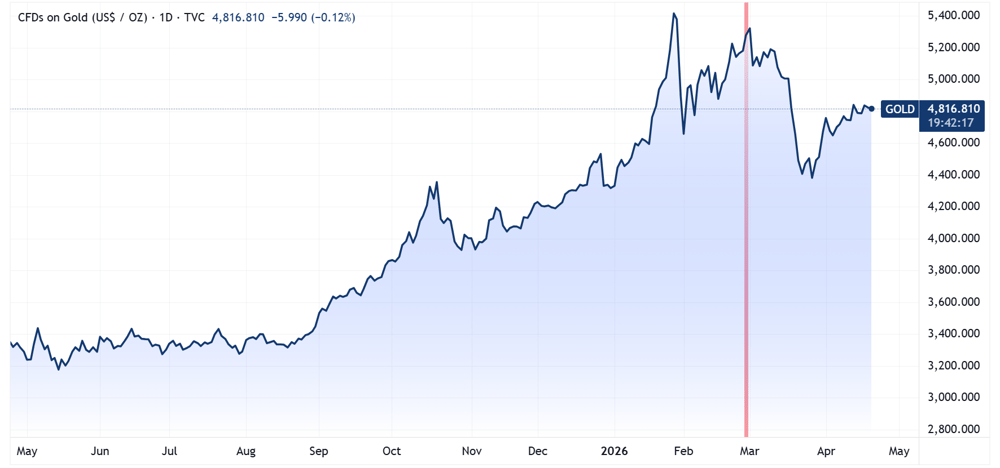

Gold price chart with conflict start date marked in red (Source: TradingView)

Why gold underperformed

Before the conflict began, gold was in the middle of a generational run, climbing as high as US$5,500/oz and more than doubling since the start of 2025.

"However, as the rally continued into 2026, it was getting more difficult to explain the continued strength. The WGC recorded an 83% year-on-year increase in investment demand in 2025 and the initial price performance this year suggests this speculative momentum had continued, making the price more vulnerable to shocks," the analysts noted.

The Middle East crisis triggered the largest global energy supply shock on record. Most of the crises gold investors cite as proof of its safe-haven status were actually demand shocks, where equities sell off, growth fears build, central banks ease, real yields fall, and gold benefits from the lower opportunity cost of holding a non-yielding asset.

A supply shock works differently, where oil prices spike, inflation risks climb and real yields rise. The analysts observed that in "previous demand driven shocks, gold typically benefited from falling 2-year yields, as markets moved to price weaker growth and earlier Fed easing. The opposite has been true this time."

"This was also seen in 2022 ... gold posted limited gains as the US entered a rate hiking cycle. The macro backdrop is different in 2026, but the sensitivity to rates remains."

This macro backdrop was then compounded by three selling forces.

Turkey's central bank sold 52 tonnes of gold between 27 February and 27 March, according to Bloomberg. India's government also delayed approvals for bullion imports, likely to ease pressure on the rupee. Other central banks slowed their buying, with January and February running at roughly 31 tonnes a month against an average of 50 tonnes through 2025.

ETFs bought 150 tonnes in January and February, but sold 90 tonnes in March as rate cut expectations evaporated.

Gold tested its 50-day moving average in mid-March and broke through. It then cut through the 100-day moving average, triggering systematic CTA selling. The World Gold Council recorded consecutive daily outflows from 17 March, peaking at 14 tonnes on 19 March, nearly double ETF outflows on the same day.

Gold finds a floor

Gold stopped falling at its 200-day moving average, which Morgan Stanley reads as a sign long-term conviction has held. ETFs also bought back roughly 39 tonnes of what they sold in March. While China's PBOC added 5 tonnes in March, running at four to five times the pace of the prior six months and pointing to buying on the pullback.

Morgan Stanley's economists still forecast two 25 bp cuts this year, in September and December. If those land, ETFs should resume buying and gold, now realigned with real yields, should benefit.

The easy money is gone

The revised US$5,200/oz target sits roughly 8% above the current price of US$4,825, but well below the previous US$5,700 bull case. Morgan Stanley says gold's structural drivers, including central bank demand, currency debasement and geopolitical tensions, are all in play. The path higher now depends on the Fed delivering rate cuts and the conflict not worsening.

The analysts flag four risks to watch:

Conflict re-escalation pushes bond yields higher again

Persistently high oil prices feed from headline into core inflation, forcing the Fed to hold or hike

A renewed equity selloff triggers margin calls and forced gold liquidation

Even in a resolution scenario, the upside is capped because the price level itself reduces purchasing power for ETFs, central banks and consumers

The bottom line: Gold looked unstoppable in January, but the picture is a lot more complicated now.