Monadelphous jumps on clean half year beat, but valuation bites back

MND beat earnings and dividend expectations and lifted its FY26 revenue outlook, but the stock slid 5.4% in the session after the result.

Mentioned

KEY POINTS

- Monadelphous’ first half result beat expectations on earnings and dividends, with margins holding up and FY26 revenue guidance tracking ahead of estimates.

- After a sharp run-up alongside industrial peers, valuation is looking fuller, making the stock more sensitive to any slowdown in margins, cash flow or contract timing.

- This article explains what drove the “clean” beat, how brokers interpreted the guidance and margin commentary, and what to watch next.

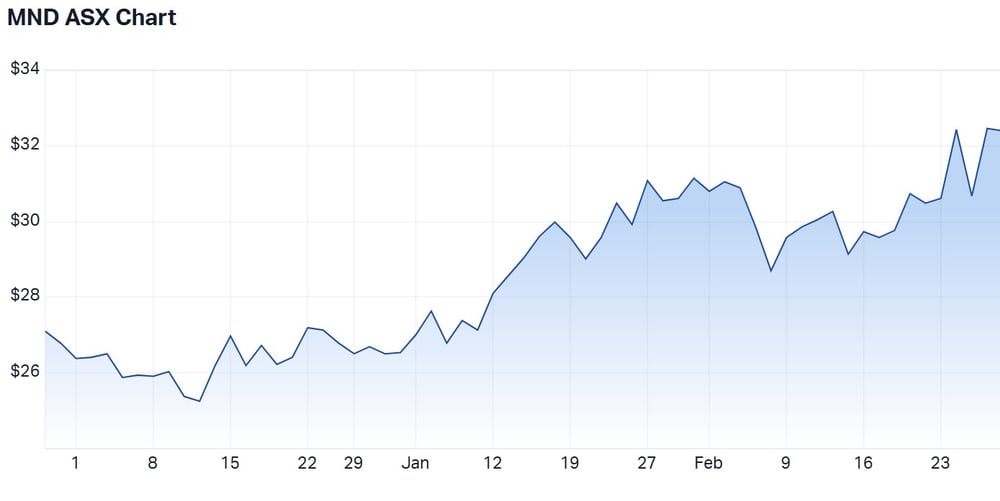

Monadelphus Group (MND) experienced arguably the most whip-saw-like price action this reporting season as a better-than-expected 1H26 result was hosed down by valuation concerns and broker downgrades.

MND delivered the fundamentals, but the stock initially moved on valuation and positioning, not the headline numbers. When MND’s sector peers found support, the stock bounced with them.

The stock is now in a tug of war between bulls backing a clean 1H26 beat, upgraded FY26 revenue guidance and intact margins, and bears pointing to a rich 30x multiple after a near 100% rally over the past year.

MND opened 10.4% higher at $33.80 on results day and pushed a further 9% to an intraday high of $36.88, before reversing sharply to close at $32.43, 12% below the session high.

The stock has stayed volatile, opening around $32 on Wednesday before sliding to $30.60 at the close, then rebounding on Thursday with shares up 5.77% to $32.45.

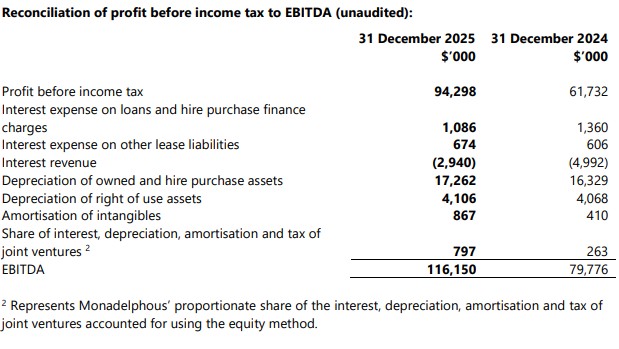

Key numbers from 1H FY26:

Revenue $1.53b, +45.6% vs PCP and vs $1.49b ests (3% beat).

Adjusted EBITDA $116.2m, +45.6% vs PCP and vs $103.8m ests (12% beat).

Underlying NPAT $64.9m, +52.6% vs PCP and vs $56.3m ests (15% beat).

Interim dividend 49c fully franked, +48% vs 1H FY25 and vs 45.5c ests (8% beat).

FY26 guidance: revenue about 30% higher year on year, with 1H operating margins maintained

Managing director Zoran Bebic struck an upbeat tone on the outlook, saying: “Long-term demand in the resources and energy sectors is expected to continue, supported by an improved global economic growth outlook.”

Mr Bebic added that Monadelphous is forecasting FY26 full year revenue to be “approximately 30 per cent higher” than the prior period, with margins maintained, pointing to a healthy pipeline across resources, energy and energy transition work.

Source: MND first half results, 24 February 2026.

Engineering construction revenue came in at $677.8m, slightly below estimates. Maintenance and industrial services printed $852m, ahead of ests $798m, reflecting strong demand across energy and iron ore customers.

Why did MND shares dip despite a good result?

Investors largely embraced Monadelphous’ 1H beat, but the stock slipped as the market shifts from celebrating the print to stress-testing what’s already priced in.

The price action two days after the result is a reminder that strong numbers do not automatically translate into sustained upside when valuation re-rates sharply.

The earnings result itself was hard to fault.

So why the pullback? The main tension is that the market is now looking through the half and asking whether this is as good as it gets.

At $32.41, MND trades on around 30.6x forward earnings, versus its FY21 to FY25 average P/E of 22.2x and a long run median of 23.9x, leaving less room for further re-rating without another upgrade cycle.

Monadelphus Group (MND) price chart

What Analysts think

Several brokers warned 1H may represent peak growth, with the risk that some maintenance activity was one-off in nature and that order book replenishment needs to continue to sustain momentum into FY27.

UBS struck a more measured note on what the market should do next. The broker described the print as “beat and raise” but warned “valuation is demanding.”

They flagged MND on 28.9x FY26E P/E versus 18.5x in FY25 and maintained a Neutral stance and $32 target.

Morgans downgraded the stock to Hold from Buy despite lifting its target price. It argued the result may mark a peak growth phase and that future upside hinges on major new contract awards.

E&P also stepped back on rating, pointing to strong execution and contract momentum but flagged the stock now trades above long-term valuation averages.

CLSA lifted its target sharply, highlighting strong demand across resources and energy, a guidance upgrade likely to drive estimate revisions, standout cash flow and balance sheet strength. But they still kept a Hold on the basis that a premium multiple already captures much of the upside.

That framing helps explain Wednesday’s dip: the result was strong, yet the stock has already re-rated hard, with investors increasingly sensitive to any hint that margins could roll over or growth could normalise.

What is next

The debate now centres on sustainability beyond the first-half beat.

Several brokers warned 1H may represent peak growth, flagging the risk that some maintenance activity was one-off and that further order book replenishment is needed to sustain momentum into FY27.

Morgans went on to add that future upside hinges on winning major contract awards.