Missed out on the lithium bull run? Here are two ideas

Lithium prices have surged 200% since June. Here are two names that offer leverage to the battery metal.

Source: Shutterstock

Mentioned

KEY POINTS

- Lithium spot prices have surged almost 200% since June 2025, with Chinese lithium carbonate futures hitting limit up for two consecutive sessions earlier this week

- Delta Lithium trades at near-zero enterprise value as its $180 million market cap roughly equals its cash holdings and Ballard Mining stake, effectively valuing its lithium projects at nothing

- PMET Resources' project NPV could jump to C$4.98 billion at current spodumene prices of $2,200 a tonne, compared to the C$1.6 billion base case that uses US$1,221 a tonne

Lithium is staging a epic comeback after a brutal plunge from historic highs in late 2022 to multi-year lows that left producers reeling and explorers pivoting to other commodities. The battery metal's spot prices are now surging again, up almost 200% since last June.

This resurgence has sent lithium stocks sharply higher over the past six months, with smaller-cap names like Argosy, Lake Resources and Global Lithium topping the leaderboards. Meanwhile, large-cap producers have also posted strong gains, with bellwether PLS Group up 194%.

Ticker | Company | % Chg | Price |

|---|---|---|---|

AGY | Argosy Minerals | 360.0% | $0.12 |

LKE | Lake Resources | 263.6% | $0.12 |

GL1 | Global Lithium Resources | 205.0% | $0.61 |

PLS | PLS Group | 194.0% | $4.90 |

CXO | Core Lithium | 192.7% | $0.32 |

WR1 | Winsome Resources | 162.3% | $0.58 |

LTR | Liontown | 152.3% | $2.20 |

MIN | Mineral Resources | 112.0% | $60.84 |

PMT | PMET Resources | 91.9% | $0.71 |

IGO | IGO | 84.0% | $9.13 |

INR | Ioneer | 69.6% | $0.21 |

DLI | Delta Lithium | 56.3% | $0.25 |

VUL | Vulcan Energy Resources. | 51.0% | $4.68 |

Share price performance of ASX-listed lithium stocks over the past six months, performance as at Wednesday 14 January 2026 (Source: TradingView)

As the rally continues to build momentum (Chinese lithium carbonate futures hit limit up for two straight sessions earlier this week), here are two under-the-radar stocks worth watching.

Delta Lithium

Delta Lithium (ASX: DLI), or Red Dirt Metals back in the day, went viral for two very different reasons.

The stock surged 103% in a single day on 28 September 2021 after announcing its recently acquired Mt Ida Project, originally a gold asset, had significant lithium potential. Mt Ida now sits at a lithium and tantalum resource of 14.8Mt.

The company's Diggers and Dealers Presentation (8-Aug-23) in August 2023 featured slides that called its Yinnetharra Lithium Project "big and very good." Those were literally the only words on screen.

Delta has caught my attention because of its capital structure and balance sheet.

Delta's market cap is currently ~$180 million

Latest cash balance was $55 million as at 13 November 2025

Delta separated its critical minerals/gold assets into a separate ASX-listed company named Ballard Mining, in July 2025

Despite the demerger, Delta retains gold exposure via a 41.4% holding in Ballard. These shares are subject to a 24 month escrow from the date they were quoted on the ASX

Ballard has a market cap of approximately $285 million (valuing Delta's stake at ~$120 million)

The result is a company with an effectively zero enterprise value, as its market cap ($180m) roughly equals its cash and Ballard Mining stake ($55m plus $120m).

Of course, that cash position will slowly trend lower and the Ballard stake is subject to escrow and not liquid. But the market appears to be pricing in near zero value for Delta's Mt Ida and Yinnetharra Projects, both of which have JORC lithium resources and are progressing key exploration programs and mining studies. You're essentially buying the assets for nothing.

#2 PMET Resources

PMET Resources (ASX: PMT), formerly Patriot Battery Metals, is developing the Shaakichiuwaanaan Project in Canada. The company completed a feasibility study for the project in October, which showcased the project's massive scale and significance. Here are some of the key highlights from the study:

Largest undeveloped hard rock lithium pegmatite Mineral Resources in the Americas, positioning to become the 4th largest spodumene producer globally, with up to ~800ktpa

World's largest known pollucite-hosted caesium pegmatite Mineral Resource and one of the largest known tantalum pegmatite Mineral Resources globally

Estimated mine life of around 20 years

Project net capex of C$1.51 billion (US$1.12bn)

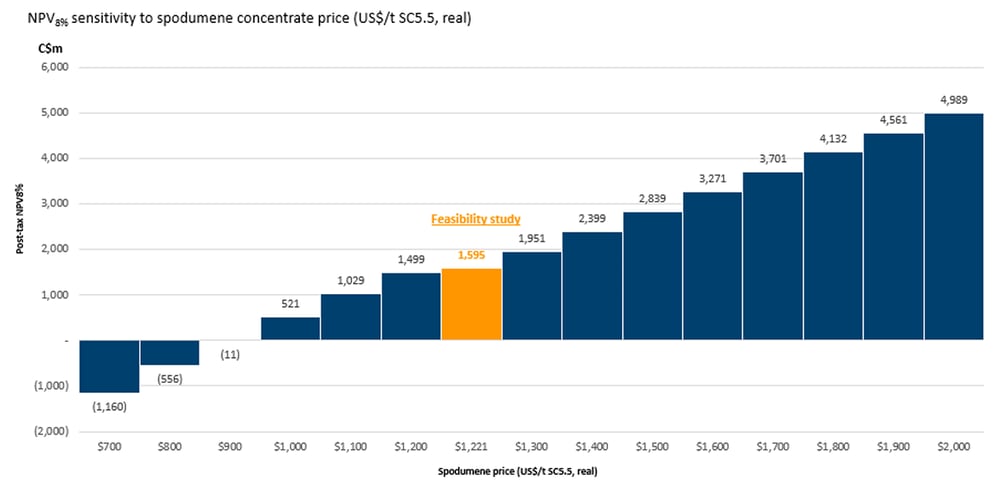

After-tax NPV of C$1.6 billion (US$1.2bn), assuming spodumene price of US$1,221 a tonne (SC5.5)

PMET is trading at a market cap of $1.17 billion, which is relatively in line with the project's NPV. But given the project's size, it remains highly sensitive and leveraged to the lithium price.

One of the slides from the feasibility study presentation shows how the post-tax NPV changes for every US$100 increase or decrease in spodumene prices. If the project assumed a US$1,300 spodumene price vs. the US$1,221 used in the study, the NPV jumps 22% to C$1.95 billion.

Shaakichiuwaanaan Project feasibility study presentation (Source: PMET Resources)

Spodumene prices are now fetching US$2,200 a tonne, according to the Shanghai Metals Market. This price point doesn't even appear in the sensitivity chart, but even at US$2,000 spodumene, the NPV of C$4.98 billion is 212% higher than the base case assumption.

One reason PMET hasn't rallied more is that it is still currently very far from production. The company is currently exploring a lithium-only feasibility study to fast-track development plans. Even then, a final investment decision only comes as soon as late 2027, with commissioning in late 2029. With the timeline so far out, the market is expressing skepticism about how sustainable the current lithium revival is.

The bottom line

These two lithium stocks both highlight leverage to lithium prices. Delta Lithium via its near-zero enterprise value, and PMET via its massive lithium resource and production aspirations.

The lithium market has some PTSD over what happened during the previous bull market, where lithium prices effectively started to move like a forward looking equity as opposed to a commodity driven by supply and demand.

The skepticism around giving these emerging names full value is understandable and explains why the best performing names are either large cap producers or developers nearing or at production. It'll be interesting to see how these leveraged names play out if lithium prices continue to stand tall or trend higher.