Magellan surges on Barrenjoey merger as strategy tilts toward investment banking

Magellan shares surged today on its proposal to merge with Barrenjoey, despite a mixed response from brokers.

Source: Shutterstock

Mentioned

KEY POINTS

- Magellan shares have closed strongly after a trading halt, as the fund manager unveiled a proposal to merge with Barrenjoey.

- The merger is a strategic pivot away from a funds management business facing sustained net outflows, into a more market-facing, investment banking earnings stream.

- This article breaks down Magellan’s 1H26 result, unpacks what brokers are saying about the deal, and what to watch next.

Magellan Financial Group (ASX: MFG) shares surged after emerging from a trading halt, closing nearly 22% higher after the fund manager unveiled a plan to merge with Barrenjoey, an Australian investment bank, in a largely scrip-based deal.

The transaction would give Magellan full ownership of the business, bringing an already fast-growing earnings stream in-house.

The announcement landed alongside Magellan’s 1H26 result, which showed the core funds management business still battling fee pressure, while earnings from strategic partnerships — particularly Barrenjoey — continue to scale.

Against that backdrop, the deal looks like a logical next step: consolidating a successful investment that is increasingly central to the group’s earnings mix.

The big brokers’ verdicts are now in — and while many see strategic merit in the shift, views diverge on valuation, execution risk, and how quickly the benefits of this transformation can be realised.

Key data and company outlook commentary

Reported metrics:

Revenue: $121.0 million, broadly in line with estimates

Operating income: $83.1 million, flat year-on-year

Interim dividend: $0.395, up from $0.264

Management fees: $111.0 million, down 8.3% year-on-year

Performance fees: $31,000, down 99.5% year-on-year

Service fees: $0.7 million, up 9.2% year-on-year

Adjusted expenses: $54.1 million, slightly higher year-on-year

Ending AUM: $39.9 billion, up 0.8%

Retail AUM: down 6%

Institutional AUM: up 5.7%

Net flows: $200 million

Guidance:

Expense growth expected to remain below inflation in H2 2026

Average fee margin guided to ~54 basis points over the next 12 months

Continued investment in AI and systems to be funded within the existing cost base

Buyback remains active, supported by ~$500 million in available capital

Broader outlook:

Strategic pivot toward earnings diversification, reducing reliance on core funds management

Barrenjoey expected to deliver more resilient and scalable earnings via diversification and operating leverage

Fee margin pressure expected to persist, driven by mix shift toward lower-margin institutional flows

Expansion of product offering, including potential fixed income strategies, to support growth

Increased exposure to market-facing revenues introduces greater cyclicality and earnings variability

Medium-term growth dependent on successful execution of the merger and integration, with initial dilution expected before longer-term accretion

Management framed the result as evidence of “earnings quality strengthening through diversification,” citing growth in strategic partnership income.

CEO and managing director Sophia Rahmani said the group would “maintain focus on operational efficiency and excellence including investment in AI to simplify and automate our investment and non-investment operations.”

Expert views

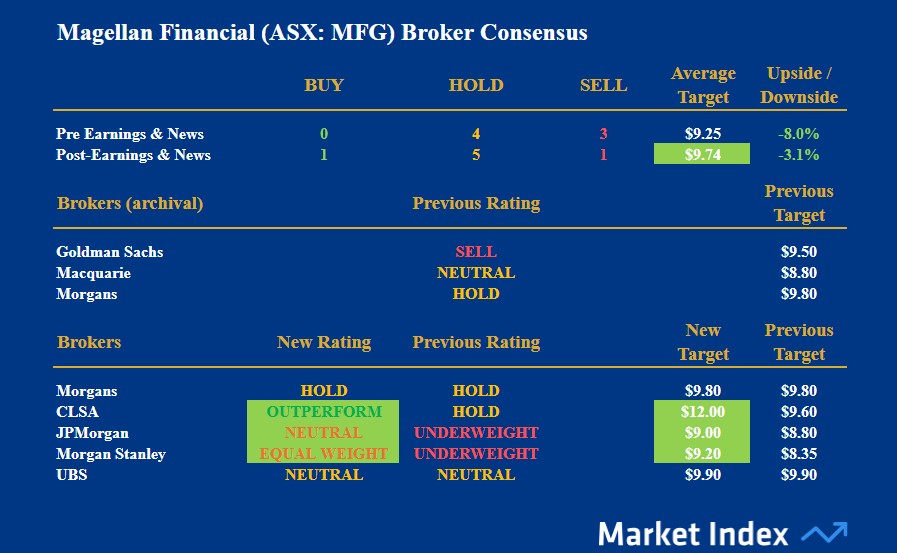

Morgan Stanley

Rating: Equal-weight (from Underweight) | Price Target: $9.20 (from $8.35)

View: Morgan Stanley sees the merger as strategically logical, arguing it “diversifies and improves earnings growth prospects” by increasing exposure to Barrenjoey’s higher-growth, market-facing businesses. The broker lifts medium-term earnings estimates and expects the deal to shift the group toward a more balanced growth profile, with operating leverage supporting double-digit earnings growth over time. While the transaction is initially dilutive and increases cyclicality risk, it is expected to become accretive from FY28. Valuation remains broadly in line with peers, limiting near-term upside but supporting the upgrade.

CLSA

Rating: Outperform (from Hold) | Price Target: $12.00 (from $9.60)

View: CLSA views the transaction as a “game changer,” arguing it materially reshapes Magellan’s investment case by accelerating its transition toward a diversified financial services platform. The broker highlights the improved earnings growth outlook and believes the combined entity offers a more compelling narrative than the standalone funds management business. It sees the strategic pivot as positioning the group closer to a Macquarie-style model, with multiple growth levers emerging from investment banking and capital markets activities.

JPMorgan

Rating: Neutral (from Underweight) | Price Target: $9.00 (from $8.80)

View: JPMorgan takes a more measured stance, noting the deal is broadly in line with peer valuations but highlighting limited disclosure around earnings adjustments and quality. While the broker acknowledges the potential for value creation if Barrenjoey’s growth trajectory is sustained, it prefers to wait for greater clarity post-transaction approval before turning more positive. The upgrade reflects improved strategic positioning, but conviction remains tempered by execution risk and uncertainty around earnings visibility.

UBS

Rating: Neutral | Price Target: $9.90 (unchanged)

View: UBS describes the strategic pivot as somewhat “bittersweet,” acknowledging the diversification benefits while questioning the attractiveness of deal terms. The broker highlights limited synergies and relatively opaque earnings visibility as key concerns, suggesting upside may be constrained despite the improved growth profile. While the merger addresses structural challenges in the legacy funds management business, UBS remains cautious on whether the new platform can consistently deliver the earnings growth required to justify a sustained re-rating.

Broker consensus

Magellan Financial Broker Consensus

To obtain a stock’s Broker Consensus Rating, we assign a value of +1 to any rating better than HOLD/NEUTRAL/MARKETWEIGHT, a value of 0 for any rating equivalent to HOLD/NEUTRAL/MARKETWEIGHT, and a value of -1 to any rating worse than HOLD/NEUTRAL/MARKETWEIGHT.

We then take the average of all assigned rating values and assign a Broker Consensus Rating of BUY to values greater than +0.5, a rating of HOLD for values between -0.5 and +0.5, and a rating of SELL for values less than -0.5.

The Broker Consensus Target is simply the average of the target prices we have on file for each broker. Typically, brokers define their target prices as a 12-month forecast. Each target price is based on fundamental valuation assumptions.

MFG’s broker consensus rating is 0.0, resulting in a Broker Consensus Rating of HOLD (up from -0.43 prior to results / Barrenjoey news — i.e. close to a SELL). Its Broker Consensus Target is $9.74 (up from $9.25 prior to results). This suggests brokers collectively believe the stock is around 3.1% overvalued based upon the last traded price at the time of writing of $10.05.

Note these values may change as other brokers in our database update their MFG ratings and price targets.