Macquarie lifts copper forecasts, backs Sandfire as its top ASX pick

Macquarie's copper price upgrade is set to supercharge miner earnings — with Sandfire and Capstone the picks to cash in.

Source: iStock

Mentioned

KEY POINTS

- Macquarie has lifted its 2026-28 copper price assumptions by as much as 33%, boosting copper miner earnings expectations by double-digit percentages.

- Sandfire Resources (SFR) is Macquarie's preferred ASX copper play, with its target price raised to $21 from $19.30 on steady, low-cost production and strong cash flow.

- Capstone Copper (CSC) had its target lifted 10% to $18, with Mantoverde earnings and a healthier balance sheet underpinning leveraged Americas exposure.

Macquarie has lifted its copper price assumptions for 2026-28 by as much as 33%, which bolsters copper equities earnings expectations by double digit percentages. In other words, the analysts expect miners to start printing some serious cash.

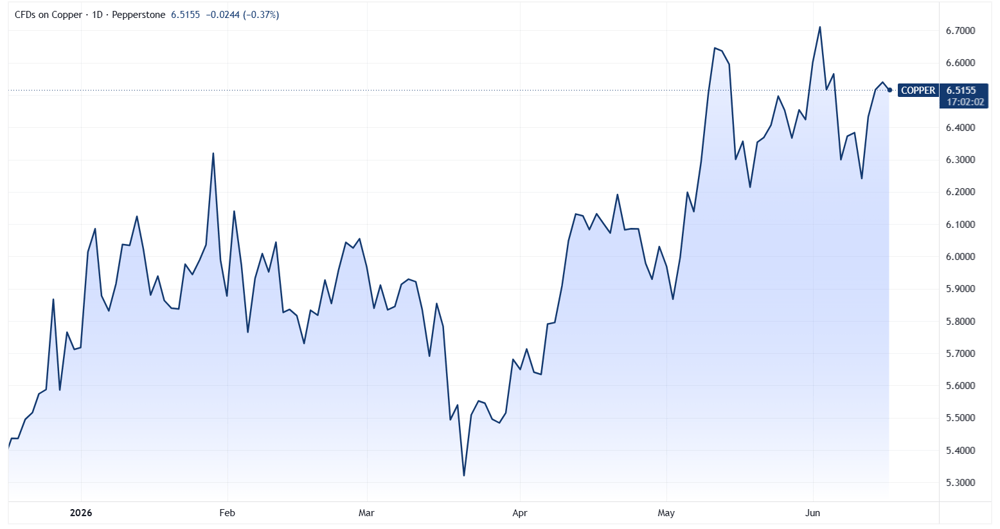

Copper prices are up 13% year-to-date, hitting a record high of US$6.71/lb on 2 June. Prices have had a volatile year, as the US–Iran conflict has driven unpredictable moves in the US dollar, inflation expectations and bond yields

Copper price chart (Source: Market Index)

Macquarie released a 15 June note lifting prior copper price assumptions by:

9% to US$6.06/lb in 2026

33% to US$6.16/lb in 2027

and 14% to US$5.43/lb in 2028

This translates to higher target prices for all copper equities under its coverage, with Sandfire Resources (SFR) highlighted as the preferred copper exposure.

Macquarie's copper ratings and target prices

Ticker | Company | Rating | Target price old | Target price new |

|---|---|---|---|---|

CSC | Capstone Copper | Outperform | $16.40 | $18.00 |

SFR | Sandfire Resources | Outperform | $19.30 | $21.00 |

AIS | Aeris Resources | Outperform | $0.70 | $0.73 |

FFM | FireFly Metals | Outperform | $2.30 | $2.50 |

29M | 29Metals | Neutral | $0.25 | $0.26 |

Source: Company Data, Macquarie, June-26

Closer look at Sandfire

Sandfire is the largest remaining pure-play copper miner on the ASX and its key projects are Motheo Copper Mine in Botswana and MATSA in Spain. The stock is up 16.1% year-to-date.

Macquarie cites in its thesis that: “Sandfire offers liquid ASX copper exposure with a diversified operating base across MATSA in Spain and Motheo in Botswana, supported by improving balance sheet capacity and a growing copper-focused project pipeline."

Macquarie raised Sandfire's target price to $21 from $19.30, on the back of improved earnings and valuation. Its appeal comes from steady production, low operating costs, and strong cash flow that benefits directly from rising copper and by-product prices.

Capstone offers leveraged exposure

Capstone Copper (CSC) is a Vancouver-based, Americas-focused copper mining company with a dual listing on the Toronto Stock Exchange and the ASX. It operates a portfolio of producing mines across the US, Mexico, and Chile.

“Capstone offers a more leveraged copper exposure through a diversified Americas portfolio, with near-term earnings increasingly underpinned by Mantoverde and a visible brownfield/organic growth pipeline,” says Macquarie.

The analysts lifted their target price for the miner 10% to $18.00, citing higher expected earnings and a better valuation on the back of a stronger copper price outlook. The balance sheet is improving too. Net debt fell to US$738 million in early 2026, and the company can tap US$290 million in funding from partner Wheaton to help fund its Santo Domingo project once an earlier advance is repaid.