Life360 pulls back after 27% rally as investors lock in gains

An FY25 beat and FY26 MAU guidance sparked a 27% spike, but the stock is still down sharply from its peak and trading on ~150x earnings.

Source: Shutterstock

Mentioned

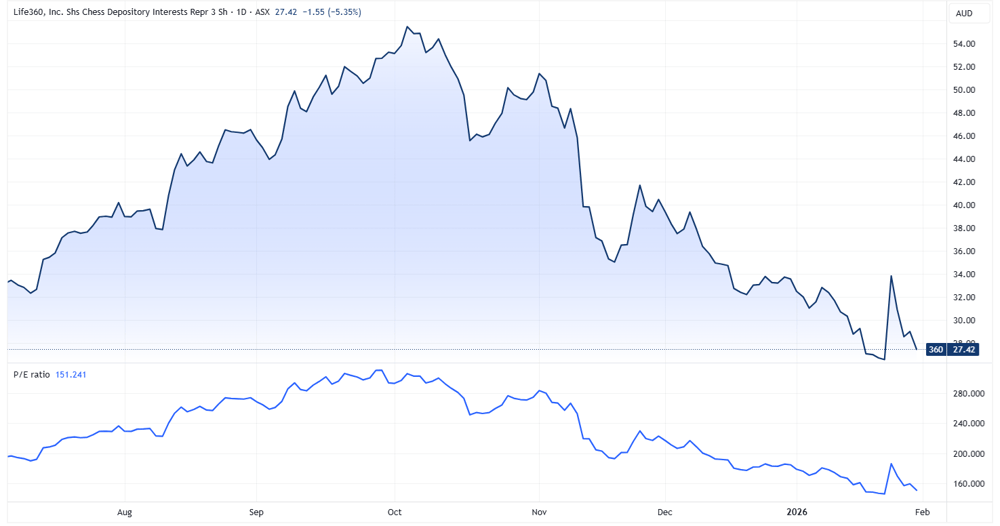

The S&P/ASX 200 Tech sector is down about 35% since July 2025, and Life360 (360) has not been spared. The stock traded down as much as 53% from its October 2025 peak, alongside a sharp valuation reset, with its trailing price-to-earnings compressing from about 300x to 150x.

The September quarter result on 11 November accelerated the sell off, after management flagged softer -than -expected monthly active user growth, particularly in the US, with the stock falling 17.6% across the following two sessions.

However, last Friday’s preliminary Q4 and FY25 update changed the tone, delivering a clear beat and raise across users, monetisation and margins. This drove a sharp 27% one day jump, though that bounce has already started to fade.

Life360 price chart with price-to-earnings | Source: TradingView)

Q4 and full-year highlights

FY25 revenue: US$486 million to US$489 million (31-32% growth)

FY25 adjusted EBITDA: US$87 million to US$92 million vs US$85 million est (4.1% beat)

EBITDA margin: about 18% to 19% vs 17.0% ests (150 bp beat at the midpoint)

FY25 net subscriber additions: 2.8 million subscribers, up 26% by 576,000.

FY26: MAU growth guided at about 20% vs 16.5% ests (350 bp beat)

Two things stood out from the September quarterly result. Firstly, FY25 MAU growth finished stronger-than-feared, which helped unwind the “US softness” narrative that emerged after the September quarter result. Secondly, the 18-19% EBITDA margin outcome serves as an important signal that operating leverage is showing up alongside user growth.

From here, the debate is mostly around valuation as Life360 is still trading at an expensive 150x. Even if the stock were to halve from here, it’ll trade closer to another popular growth name – TechnologyOne, which trades at around 62x.

The recent software exodus on Wall Street doesn't help either. The iShares Expanded Tech-Software ETF fell 4.9% on Thursday, now down 22% from recent highs and down ~13% month-to-date. During that session, several household software stocks like ServiceNow, SAP, Hubspot and Atlassian all dipped more than 10% amid concerns that AI could disrupt these business models.

Life360 has effectively gone full circle since July 2025, which means a large cohort of holders are likely sitting at or below breakeven, creating plentiful overhead supply. This likely explains why the stock was sold off rather aggressively in recent sessions as holders seek to exit for a small loss or around breakeven.

The next hard catalyst is the full year result and FY26 outlook in early March. The market will be watching three datapoints: FY26 MAU growth rate versus the 20% guide, subscriber conversion and churn (especially outside the US), and whether EBITDA margins of 18-19% holds as the company scales.