Is Simandou really a 'Pilbara killer'? What the iron ore sell-off means for BHP, RIO and FMG

A new African mega-mine sent the iron ore price tumbling, and BHP, RIO and FMG with it. Is the Simandou threat real or overblown?

Source: Shutterstock

Mentioned

KEY POINTS

- For most of this decade, iron ore defied the sceptics, hovering near US$100 a tonne, handing ASX-listed iron ore miners years of fat margins.

- Then came April's production data from Simandou – Guinea's giant iron ore mine – showing it ramping up faster than expected. The news sent iron ore tumbling from a two-year high and triggered a major sell-off in local iron ore stocks.

- We unpack the demand and supply forces now reshaping the iron ore market, ask whether Simandou really is going to be a 'Pilbara killer', and lay out what the experts see ahead for BHP, RIO, FMG and CIA.

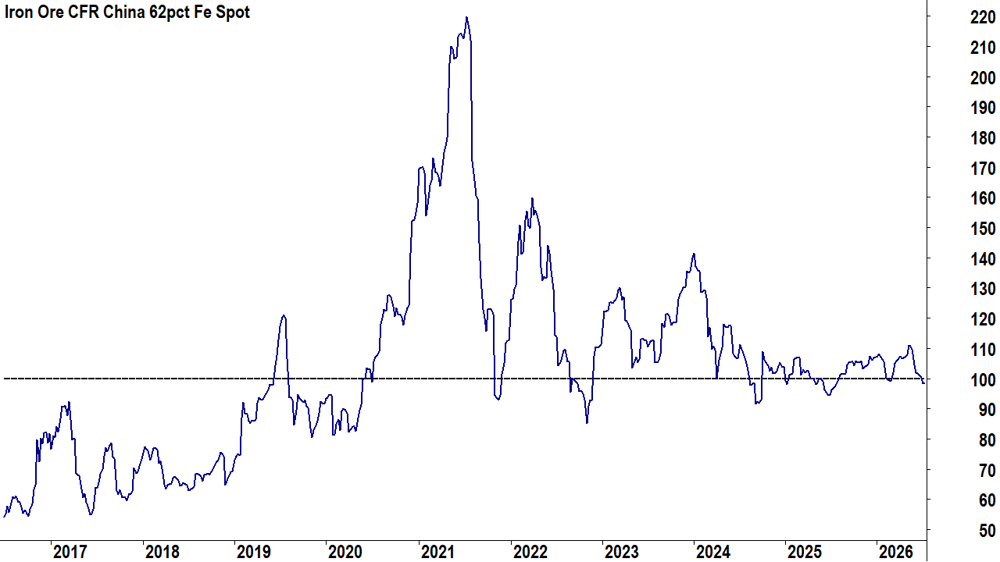

For the best part of a decade, iron ore has been the commodity that simply refused to break. Through China's property unwind, a peak in its steel output and a long grind lower in its growth rate, the price of Australia's most valuable export has now spent nearly seven years hovering around US$100 a tonne.

That resilience has underwritten enormous wealth. It has kept BHP, Rio Tinto (RIO), Fortescue (FMG) and Champion Iron (CIA) among the most reliably profitable miners on the ASX, and kept royalties flowing into federal and state coffers.

Iron ore spot price chart last 10 years. Source: Norgate Data

Yet in mid-May, the story wobbled. Fresh data showed the vast new Simandou mine in Guinea – a project two decades in the making – finally hitting its stride, and the benchmark SGX futures price slid from a two-year high of US$111.60 a tonne to as low as US$96.70 on 26 June, a fall of roughly 13% in six weeks. It has since steadied to trade near US$99.

The prices of iron ore stocks adjusted in kind. Fortescue slumped to an 11-month low and Champion Iron to levels not seen in over five years. Investors have returned to the question that has hung over the sector for years: is Simandou a "Pilbara killer" – the mine that finally breaks the stronghold Australian iron ore has enjoyed since the 1990s?

In this article we’ll look at what the latest data tells us about the two forces setting the iron ore price – Chinese demand and global supply – then turn to the question that matters most for shareholders: Just how important is Simandou really for BHP, RIO, FMG and CIA?

Iron ore demand side factors: the China dilemma

Let’s start with a first principle. Iron ore has essentially one customer: the steel industry. And China makes more steel than the rest of the world combined. So, when investors talk about iron ore demand, they're really talking about the health of Chinese steel.

When it comes to Chinese steel, the country’s massive property sector is the swing factor. Leading natural resources analytics firm Wood Mackenzie estimates construction has accounted for as much as 60% of Chinese steel demand at its peak, with housing contributing about 40% in 2020 – a share it expects to fall towards 23% over the long term as the sector shrinks. When Chinese property builds, iron ore miners prosper – right now, it’s doing the opposite.

The latest read on the Chinese property sector is sobering. Morgan Stanley's China team notes new property starts fell 24.7% year-on-year in May and floor space sold dropped 14.1%, while fixed-asset investment fell 12.5% and retail sales turned negative – indicating a two-speed economy in which export-led factories hold up while domestic demand keeps sinking. The team has second-quarter GDP tracking at just 4.4%.

That weakness is feeding straight through to Chinese steel mills. Maritime data analytics firm Signal Ocean reports Chinese crude steel output fell 2.5% year-on-year in May, to 84.4 million tonnes. Profitability is thinner still: margins on rebar – the reinforcing bar buried in every concrete slab and apartment tower – sit close to their lowest in a decade, and futures prices suggest no sign of relief before year-end. Meanwhile the ore keeps piling up, with Chinese port inventories at roughly 160 million tonnes and the market in surplus since mid-2025 – a surplus Signal Ocean expects to persist through the rest of this year.

Nor can Chinese steel mills lean on the rest of the world. Morgan Stanley reports China shipped 10.3 million tonnes of steel offshore in May, but that was 2% less than a year earlier – suggesting the export valve that has long absorbed China's surplus steel is narrowing. Signal Ocean notes that fresh tariffs on Chinese steel exports would shut that valve further, backing up inventories at home, weighing on steel prices, and squeezing mill margins harder still.

None of this is fatal for iron ore on its own. But the direction of travel on the demand side is unmistakably soft, and it leaves the iron ore price leaning heavily on the supply side of the ledger for support.

Iron ore supply side factors: the Simandou question

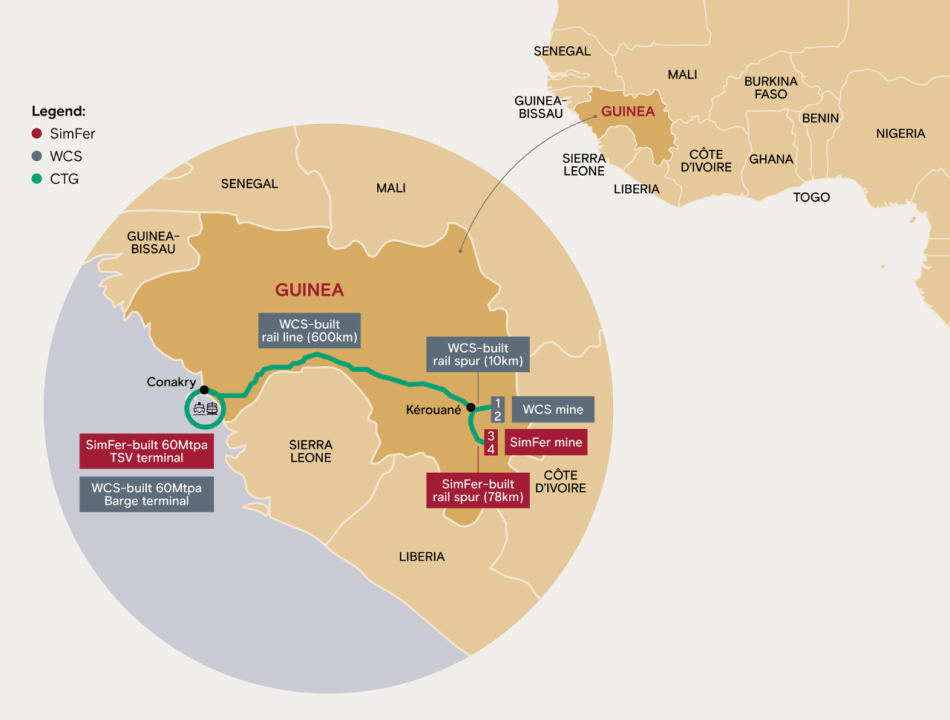

Which brings us to the elephant in the room. Simandou is the largest high-grade iron ore deposit in the world, buried in the hills of south-eastern Guinea and stalled for decades by politics and the sheer cost of building a mine, railway and port from scratch. It is now real: a Rio Tinto-backed venture (SimFer) and a Chinese-led consortium (Winning Consortium Simandou) shipped first ore in December 2025, and once fully optimised the operation can move around 10 million tonnes a month – roughly 120 million tonnes a year of premium, high-iron-content ore.

Simandou Iron Ore project, Guinea. Source: Rio Tinto

The April data are what spooked the market. Maritime data analytics firm Signal Ocean reported on 12 May that Guinean shipments had breached 1.2 million tonnes for the first time – a record since the mine came online.

The ramp has only accelerated since. UBS estimates shipments stepped up to a run-rate of about 30 million tonnes a year in May, more than double the pace of the preceding three months. Crucially, that outpaces what the market has penned in. UBS's own 2026 shipment forecast of 22 million tonnes now carries upside risk on its reckoning, while Macquarie's production model has the project delivering just 6 million tonnes across the year.

The iron ore price is perhaps the clearest read on how surprised the market was by the data – and it fell hard. The one near-term caveat is weather. Guinea's wet season runs from July to October, and Signal Ocean reports June loadings already dipping to 1.5 million tonnes as rain reached the Morebaya stockpile – a reminder that the ramp will not be a straight line.

So, is Simandou likely to be a "Pilbara killer"? On the evidence, the fear looks overdone. As Rio Tinto's iron ore chief Matt Holcz told the Australian Financial Review Mining Summit in Perth in late May – after Simandou's April production data was released – "the demise of the iron ore price has been greatly exaggerated over recent years." His argument is one of scale: the seaborne market needs to replace roughly 800 million tonnes of ageing production over the next decade, and even at full tilt, Simandou will supply only about a sixth of that.

Holcz's observation suggests that Simandou backfills natural depletion more than it floods the market. Its high-grade ore also serves somewhat different customers to Pilbara fines, letting the two products co-exist – though Fortescue's Andrew Forrest has warned Pilbara ore is the less suited of the two to the more efficient and lower emissions electric-arc furnaces China is now rolling out.

The most important support factor for the iron ore price, though, is cost. UBS puts the current price at roughly 5% inside the global cost curve, meaning around 85 million tonnes of high-cost supply already sits near or below break-even. The Middle East conflict has lifted diesel prices, sharpening that effect. As the price falls, that marginal, diesel-heavy tonnage is forced out – which is why the price has repeatedly found a floor near US$90–100 a tonne.

For shareholders, BHP and RIO sit among the world's lowest-cost producers, with FMG, CIA and Mineral Resources (MIN) further up the curve, but still comfortably profitable around US$90 a tonne. UBS makes the same structural point, but notes that in any further downturn the lower-cost majors would prove far more resilient than their higher-leverage peers.

What the experts make of the major ASX iron ore stocks

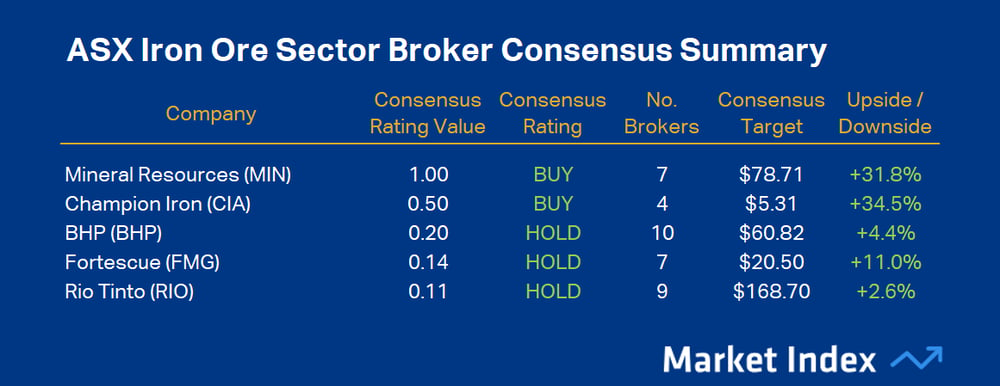

Step back from the price, and the broker community is relatively sanguine – but there is no single favourite, with each research team landing on a different name. The consistent thread is a preference for low-cost, diversified balance sheets over highly geared pure-plays if the price grinds lower. Morgan Stanley names BHP its preferred exposure, while UBS prefers MIN. Macquarie prefers RIO but singles out Fortescue and Champion Iron as its stronger picks on self-help cost-out plans – a reminder that even in a softening market, the cheapest stocks can offer the most upside.

ASX Iron Ore Sector Broker Consensus Summary. Source: Market Index Broker Consensus. To obtain a stock’s Broker Consensus Rating, we assign a value of +1 to any rating better than HOLD/NEUTRAL/MARKETWEIGHT, a value of 0 for any rating equivalent to HOLD/NEUTRAL/MARKETWEIGHT, and a value of -1 to any rating worse than HOLD/NEUTRAL/MARKETWEIGHT. We then take the average of all assigned rating values and assign a Broker Consensus Rating of BUY to values greater than +0.5, a rating of HOLD for values between -0.5 and +0.5, and a rating of SELL for values less than -0.5. The Broker Consensus Target is simply the average of the target prices we have on file for each broker. Typically, brokers define their target prices as a 12-month forecast. Each target price is based on fundamental valuation assumptions.

Note that a Consensus Rating Value of 1.0 implies unanimous buy ratings among the brokers surveyed, demonstrating the strength of consensus for MIN. CIA sits precisely at the 0.5 cut-off for a buy, and at 0.20, 0.14, and 0.11 respectively, BHP, FMG and RIO could be described as 'solid holds'.

As for price growth upside to Consensus Target, CIA is seen to have the greatest potential for price appreciation (+34.5% to Consensus Target), with MIN also seen as substantially undervalued (+31.8% to Consensus Target). FMG's +11.0% 12 month forecast return still sits above the ASX 200's long-run average annual return, but if the consensus is correct BHP and RIO may struggle to deliver market-beating returns over the next 12 months.

When using broker consensus data, consider that stocks with greater coverage are likely to have the most reliable metrics. I’ve used a minimum cut off of three brokers to calculate a consensus, and there is a 3-month cut off on recency to ensure we are dealing with the latest broker data. Broker ratings and targets are subject to change, and indeed, change regularly, so be sure to keep an eye on our Broker Consensus page.

Conclusion: expectations versus reality

The market didn't learn in May that Simandou existed – the mine has been in plain sight, and in everyone's forecasts, for years. What jolted the price was the gap between a modest expected ramp-up and a developing reality that likely dwarfs it. The gap is the real story: from here, the iron ore price will respond to expectations versus reality, not to the spectre of Simandou's existence.

For now, the experts are not calling for a collapse. UBS and Macquarie both see the price near US$100 a tonne this year, drifting only to the mid-US$80s to mid-US$90s by the end of the decade – levels at which the Pilbara's low-cost majors stay comfortably profitable, and at which the "Pilbara killer" headline looks overblown.

But the risk is asymmetric. If Simandou keeps beating expectations, those long-term forecasts – and the valuations built on them – will be marked lower. Moving forward, investors should keep an eye on the Simandou ramp data and any news on Guinea’s wet season as well as China's steel and property numbers.

This article draws on institutional research from UBS (June 2026), Morgan Stanley (June 2026) and Macquarie (June 2026); shipping and steel market data from Signal Ocean (May and July 2026); and Chinese steel demand data from Wood Mackenzie. Global steel production data sourced from the World Steel Association.