IPO Watch: Boresight lit up June, yet most 2026 ASX floats can't hold their pop

ASX IPOs are popping on debut then fading fast. The first nine listings of 2026 are all now trading in the red.

Source: iStock

Mentioned

KEY POINTS

- Nineteen IPOs have listed in 2026, debuting 33.7% higher on average and trading up 76% of the time. Strip out the big runners and that debut pop falls to just 8.1%.

- Defence tech play Boresight had an epic debut, closing 60% higher on day one and 70% higher on day two. Demand faded by day three, finishing up 9.1%. It is now trading back at debut price levels.

- New listings are struggling to hold gains. The first nine debutants of 2026 are all underwater, down 26% on average, with a busy July pipeline still ahead.

June kept 2026's IPO revival ticking over, with three more debuts pushing the year-to-date count to 19.

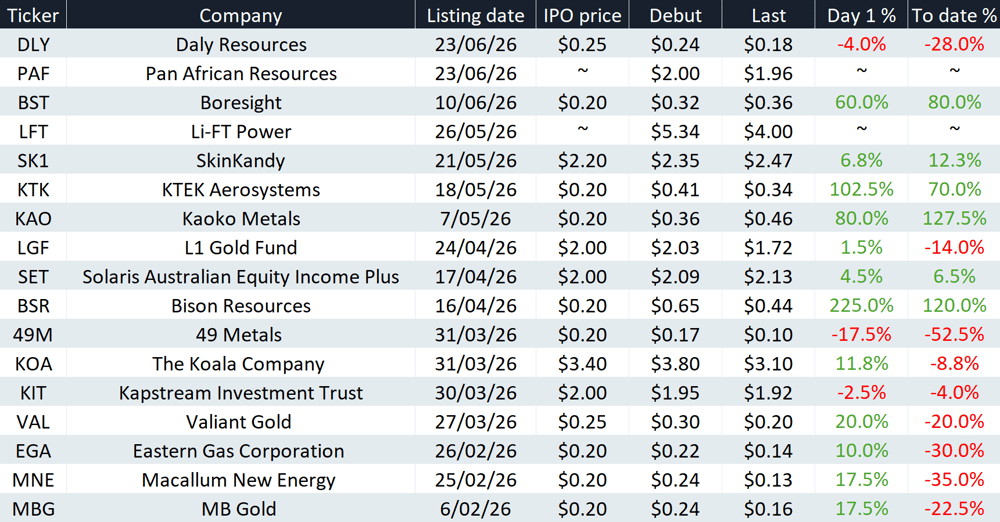

Ticker | Company | Listing date | IPO price | Debut | Last | Day 1 % | To date % |

|---|---|---|---|---|---|---|---|

DLY | Daly Resources | 23/06/26 | $0.25 | $0.24 | $0.18 | -4.0% | -28.0% |

PAF | Pan African Resources | 23/06/26 | ~ | $2.00 | $1.96 | ~ | ~ |

BST | Boresight | 10/06/26 | $0.20 | $0.32 | $0.36 | 60.0% | 80.0% |

Share price performance as at Tuesday, 30 June 2026

Daly Resources is a Northern Territory-focused explorer targeting fluorite, copper and zinc, with an immediate focus on the Huckitta fluorite-copper project, where Sandfire Resources is a major shareholder.

Pan African Resources is an established mid-tier gold producer with underground mines and tailings retreatment operations across South Africa and Australia. The company is listed on both the London Stock Exchange and South Africa's JSE.

A closer look: Boresight

Boresight is an Australian defence tech company selling low-cost, "attritable" (designed to be destroyed) drone targets that let militaries run realistic live counter-drone training without sacrificing expensive platforms or relying on unreliable hobby drones.

It has a very niche value proposition, betting that drone warfare has outpaced the systems built to train against it. The pitch revolves around selling targets cheap enough to shoot down, standardised enough to pass certification, and sovereign enough (aka non-Chinese) to clear procurement in allied markets.

Boresight's June 2026 investor presentation highlights a land-embed-expand-lock-scale flywheel built on recurring consumption:

Land: Low-cost targetry sold at unit level bypasses slow procurement, giving an instant entry point.

Embed: Drones are consumables destroyed in annualised training cycles, so reorders recur and Boresight becomes part of training doctrine.

Expand: Upsell into the BS-350 attritable ISR (intelligence, surveillance and reconnaissance) platform, swarm capability, payload variants, spares and consumables.

Lock: Integration with certification/training, AI swarm-control subscriptions and performance-data capture creates high switching costs.

Scale: Volume drives down COGS, strengthens the sovereign manufacturing moat, and supports a licensing model for allied markets (Europe, UK and US).

Its prospectus showed revenue climbing 57% in FY25 to $4.36 million from $2.76 million, though the net loss widened sharply to $722,430 from $99,919 a year earlier.

The hype behind the defence sector arguably peaked in October 2025, when DroneShield was up around 760% year-to-date and carried a $5.7 billion market cap. The stock is now down about 60% from its all-time high but still holds a commendable $2.2 billion valuation, and recent quarterly earnings have continued to set records while staying cash flow positive. Defence peers like Electro Optic Systems and Elsight have held up well too, sitting within 10-15% of their own record highs.

With that in mind, Boresight had a strong debut, closing its first session up 60% from the offer price to 32 cents. Day two proved even more volatile, opening flattish before finishing 70% higher at 54.5 cents. The third day hinted at fading demand, with the stock closing 9.1% higher at 59.5 cents despite rallying as much as 34% intraday. It's now back at the mid-30 cent mark.

Boresight price chart (Source: TradingView)

IPOs so far this year

IPOs have debuted 33.7% higher on average this year and traded higher 76% of the time. The debut average drops to just 8.1% if you exclude the massive runners like Bison Resources, KTEK Aerosystems, Kaoko Metals and Boresight.

Share price performance as at Tuesday, 30 June 2026

However, new listings have struggled to hold on to initial gains, with the first nine stocks that debuted this year all trading in negative territory, down 26% on average.

A very busy July

July will be the busiest month yet, with IPOs spanning more than just 20 cent explorers. There are currently nine companies scheduled to debut this month, including:

AI Opportunities Trust (AIX): Pengana-run listed trust giving Australian investors access to private, unlisted AI companies (e.g. OpenAI, Anthropic, ByteDance) via a self-liquidating structure.

Alurion Resources (ALU): Brazilian Rare Earths demerger holding the Amargosa bauxite-gallium project in Brazil, positioned as a standalone bauxite and critical minerals developer.

Ceretas (CER): Australian medtech commercialising a non-invasive therapeutic ultrasound device for dementia, Alzheimer's and other neurological conditions.

FDC Consolidated Holdings (FDC): Long-established national commercial construction and fit-out group, expanding into data centres and retirement living, one of 2026's largest ASX floats.

Monvia (MNV): Insurance software company (formerly Axe Group) offering a fully-managed SaaS platform covering policy administration, claims management and new business, primarily for life and general insurers.

IPOs continue to post strong debuts, but the key challenge is holding onto those big one-day gains against thin liquidity and a lack of fresh newsflow. Let's see if those Jan-Mar debutants can bounce back to breakeven, and how the next wave of listings performs.