Investment banks warn Australia's real estate boom is over — what it means for property investors

House prices are showing early signs of cracking — and experts warn there’s a perfect storm brewing homeowners can’t afford to ignore.

Source: Shutterstock

KEY POINTS

- Australia's housing market has run hard, with national price growth of 9% in 2025 and over 55% since 2020, but the same investor-driven momentum that fuelled the boom is now one of its biggest vulnerabilities.

- The landscape is changing quickly: RBA rate hikes, collapsing auction clearance rates, and a Federal Budget on 12 May that may reshape the tax economics of property investment — each represent threats to the real estate market’s momentum.

- This article will explain the reasons for an impending slowdown in Australian property, the policy wildcards ahead, and what it all means for investors exposed to the housing cycle.

Australia has weathered housing downturns before. The early 1990s recession saw dwelling prices fall sharply in real terms, and it took the better part of a decade for the market to fully recover. The post-2017 correction — driven by APRA's investor lending crackdown — trimmed national prices by roughly 10% before COVID-era rate cuts to historic lows turbocharged the present cycle. Each time Aussie property has faltered, the market eventually found its footing — each time, the recovery was faster than the pessimists expected.

So even if this article’s headline is correct and the present up-cycle is over, given that Australian house prices have always recovered, is there really anything to worry about?

This time might be different. A perfect storm of factors is brewing that could send property prices into a tailspin — and keep them subdued for an extended period. Affordability has rarely been this stretched. Mortgage servicing costs for the average new buyer are on track to breach record highs. In short, the gap between what the average household can actually afford to pay and what a house costs is widening again.

Australia’s housing market has entered this possible downturn with very little buffer. The structural supports that kept prices elevated — strong investor demand, migration, and an expanded Home Guarantee Scheme — are now being tested simultaneously by higher rates and a slowing economy.

The article maps the order in which the dominoes may fall, the policy wildcards that could accelerate or deepen the decline, and the ground-level signals already visible in display homes and auction rooms across the country.

The end of the great Australian property investing boom?

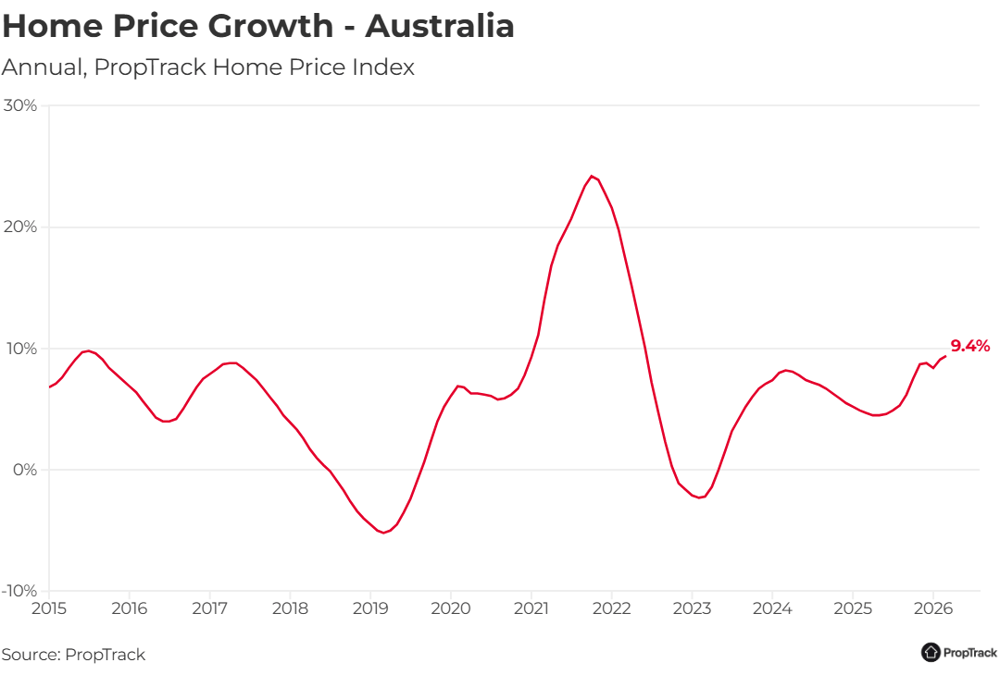

National dwelling prices grew close to 9% last year, and have risen over 55% since the first quarter of 2020. But the headline figures mask a significant divergence: in inflation-adjusted terms, Sydney and Melbourne prices remain below their 2021 peaks — while Brisbane, Adelaide, and Perth have carried the national average, driven by interstate migration and affordability.

Home Price Growth – Australia. Annual, PropTrack Home Price Index. Source: Prop Track

Critically, investors were a key engine of that strength. The investor share of new housing lending has climbed back toward the highs last seen before APRA intervened in 2017 to cap investor lending growth and tighten interest-only loan conditions. Investors may be back in force, but history suggests their growing participation carries real risk — and this time, rising borrowing costs and the prospect of less favourable tax treatment are moving against them simultaneously.

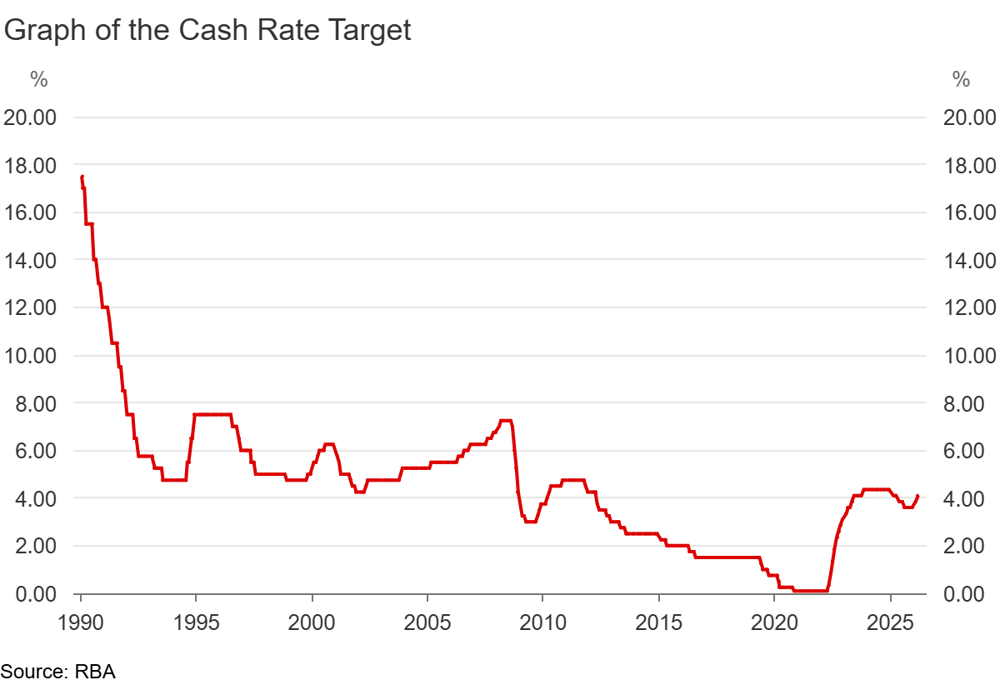

The RBA has hiked 25 basis points in both February and March, taking the cash rate to 4.1%, and markets are pricing a further 60 basis points of tightening by year’s end. Mortgage servicing costs are rising — and for investors navigating a wide gap between rental yields and borrowing costs, the arithmetic is deteriorating quickly.

How the property cookie crumbles…

Two of Australia's leading investment banks have independently arrived at the same conclusion over the last couple of weeks: the Australian housing market is heading for a meaningful correction. Their research points to a sharp shift in the early indicators of a downturn — and the timing couldn't be worse for overleveraged investors.

The warning signs are already flashing:

Sequential monthly price growth in Sydney and Melbourne has turned negative

Surveyed price expectations fell sharply in March

Auction clearance rates have dropped to levels historically consistent with national price declines in the months ahead

Nationally, 50% of home builders expect volume declines over the next three months

Mortgage servicing costs for the average new buyer — measured as a share of household disposable income — are on track to breach record highs

Morgan Stanley's research concludes that forward indicators suggest prices are “likely to fall over the coming months” — with headwinds from higher rates and a slowing economy still building.

But the more consequential development may be what's coming on 12 May. The Federal Budget is widely expected to include changes to the Capital Gains Tax (CGT) discount — potentially reducing it from 50% to 33% for housing investors — and possibly reduce the benefits of negative gearing. The key swing factor is whether any changes are grandfathered. The Government's emphasis on "intergenerational equity" as the policy rationale suggests the risk of non-grandfathering is underappreciated by the market.

The ground-level evidence is already consistent with this read. Macquarie's proprietary HomeBuilder Survey of 30 detached builders conducted in April found investor demand in Victoria had dropped sharply — with CGT uncertainty cited explicitly as a key driver. National house prices fell 10% into the 2019 election on the prospect of a similar policy package. Investor activity has since returned to comparable levels — leaving the market equally exposed.

Will the RBA ride to the rescue this time?

In previous downturns, the RBA's willingness to cut rates aggressively provided the circuit breaker that stabilised the housing market. This time, the calculus is different — and the RBA may not be in any hurry to help. Here, Macquarie's view is pointed: the market is “under-estimating the impact of higher-for-longer rates on residential volumes, pricing and margins.”

Morgan Stanley goes even further, noting that the RBA will likely welcome housing weakness as confirmation that its tightening policy is working. The Bank has pointed to rising house prices and credit growth as reasons why financial conditions eased more than expected in 2025 — and it will be watching both variables soften before considering any change of course.

The financial stability argument — the one that has historically motivated the RBA to act — is also less compelling this cycle. Even an 18% fall in national house prices, Morgan Stanley estimates, would leave only around 1.8% of aggregate loans in negative equity. That's broadly in line with pre-COVID levels — well within the range the RBA considers manageable.

RBA cash rate changes since 1990. Source: RBA

So what would prompt the RBA to move in favour of homeowners? A sharper-than-expected deterioration in the broader economy is the most likely trigger — and Morgan Stanley has already cut its GDP growth forecast to 1.2% for 2026, well below the consensus of 1.6%. Arguably though, that's a slowing economy, not a collapsing one.

The message for homeowners and property investors is uncomfortable but clear: don't count on the RBA riding to the rescue. The Bank has reasons to let this housing correction run.

Conclusion: Watch this space (very closely!) 🧐

The Australian housing market is not in freefall. But it is under pressure from multiple directions simultaneously — higher rates, stretched affordability, softening investor demand, and a Budget that may reset the tax economics of property investment before the market has fully absorbed the rate shock.

Investors will want to pay very close attention to:

Sales volumes and building approvals — the earliest indicators of stress in the cycle.

Credit applications and approvals — will lag by months, but softer data here will show animal spirits in the sector are waning.

Stocks exposed to residential development — particularly those with significant pipelines in New South Wales and Victoria — may see earnings headwinds before the broader market fully prices the slowdown in.

The RBA's comfort with some degree of housing weakness, and the relative resilience of household balance sheets, suggests this is likely a correction rather than the start of a crisis. But corrections are real, and for those who can least afford a contraction in the value of their homes — they can be deeply painful. The most leveraged investors and homeowners may find themselves in negative equity, paying off loans larger than the value of their investments.

Housing weakness has historically weighed on consumer confidence and spending, with knock-on effects for growth and employment. All investors, whether those exposed to stocks or bricks and mortar, must pay very close attention to price trends and sales volumes into the 12 May Budget and beyond.

This article draws on institutional research from Morgan Stanley and Macquarie, both published in April 2026.