How does the ASX 200 perform in May?

May is usually a quiet month for the ASX 200, but a wave of corporate downgrades and a hawkish RBA could change that script in 2026.

Source: Shutterstock

KEY POINTS

- The ASX 200 has averaged a 0.17% gain in May since 1980 and finished positive 63% of the time, but this year arrives against a tougher macro backdrop with soaring oil prices, a barrage of negative corporate updates and a hawkish RBA

- Recent corporate updates from Cochlear, Woolworths, Westpac, Orora, a2 Milk and others point to mounting pressures across industrials, consumers and healthcare, with cost inflation and Middle East exposure recurring themes

- Macquarie still forecasts 10.5% earnings growth for the ASX in FY26, led by resources on stronger base metal and energy prices, though the heavy reliance on banks and miners masks clear headwinds beneath the index

The S&P/ASX 200 enters the month of May on a rather turbulent note – snapping an eight-day losing streak last week and suffering from a barrage of negative corporate updates, spanning high-profile names like Woolworths, Cochlear, Westpac, Orora and more.

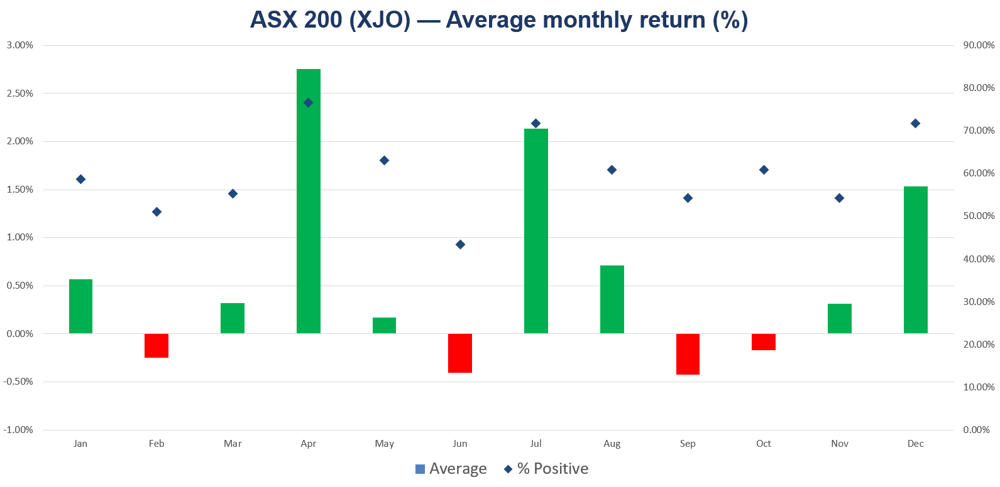

Historically, May ranks among the quieter months. Since 1980, the ASX 200 has averaged a 0.17% gain in May and finished positive 63% of the time.

Source: Market Index

The past ten Mays have outpaced that historical average, returning 0.51% on average and finishing positive 70% of the time.

Year | May |

|---|---|

2016 | 2.41% |

2017 | -3.37% |

2018 | 0.49% |

2019 | 1.13% |

2020 | 4.22% |

2021 | 1.93% |

2022 | -3.01% |

2023 | -2.98% |

2024 | 0.49% |

2025 | 3.80% |

Source: Market Index

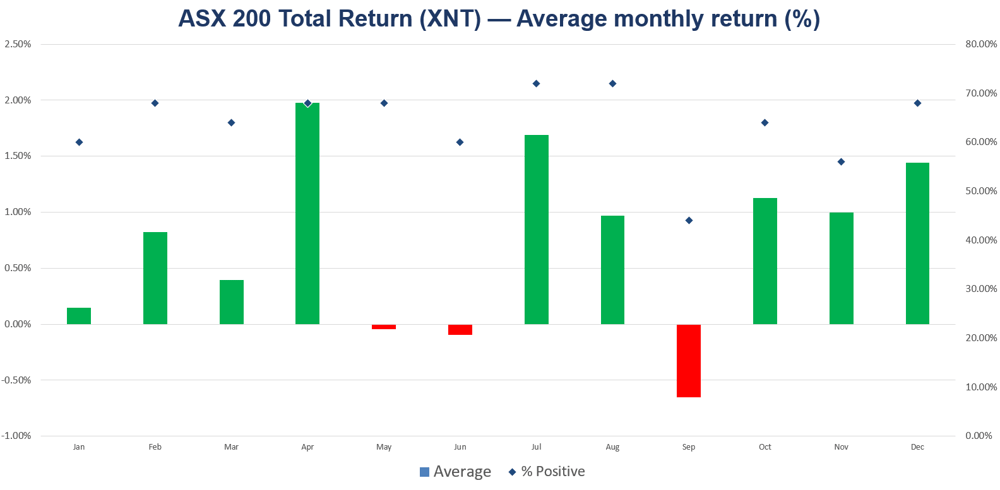

Our S&P/ASX 200 total returns data dates back to May 2001, showing an average return of -0.04% and a positive hit rate of 68%. The softer average reflects both the smaller sample and a difficult stretch between 2006 and 2013.

Source: Market Index

The total returns data highlights the old adage "sell in May and go away" as May-October period delivers the weakest six-month returns on average, of just 0.37%, well-below the 5.78% gain for the November-April stretch.

Overall, May tends to be one of the calmer periods for markets, but this year it arrives against a tougher backdrop:

The RBA is poised to hike for a third straight meeting, fully reversing last year's cuts.

Australia's annual inflation climbed to 4.6% in March, the highest reading since September 2023 and well above the RBA's 2-3% target.

The April S&P Global PMI flagged a sharp pickup in cost inflation that will keep filtering through to consumers. Australian input costs rose for a third straight month to their highest level since August 2022, driven by fuel and shipping. Charge inflation hit a 3.5-year high as firms passed those costs on.

As for markets, the ASX has been battered by downbeat corporate updates in recent weeks. Most reactions have stayed confined to the affected stock, though several (Cochlear, the Big Four banks, Woolworths and more) have triggered broader selling across their sectors.

Corporate updates at a glance

Airlines & Travel: Mixed but broadly cautious. Air NZ suspended its full-year guidance. Qantas and Virgin flagged near-term earnings headwinds from sharply higher jet fuel prices, partly offset by stronger pricing and tighter capacity. Cinema, hotel and restaurant operator EVT warned of emerging demand weakness in its FY26 update.

Financials: Geopolitical and macro risks ran through every update. Westpac flagged softer-than-expected revenues, citing margin pressure in its treasury markets division and a higher impairment charge. NAB lifted impairment charges for sectors most exposed to geopolitical risk. Judo Capital reaffirmed guidance at the low end with a top-up provision for economic conditions, and Iress guided FY26 revenues to the bottom of its range, citing the same risks.

Industrials & Materials: Reactions were broadly negative, with Middle East exposure front of mind. Orora issued materially lower EBIT guidance, Worley said some customers were delaying the commencement and award of new projects, Cleanaway cut guidance, and Fletcher Building said the Middle East impact can't yet be quantified.

Consumer Staples & Agriculture: Cost pressures and softening demand were the recurring themes. a2 Milk lowered FY26 NPAT guidance to "similar to down" on higher air freight costs. Woolworths flagged that FY26 Australian Food EBIT growth would no longer reach the upper end of the mid-to-high single digit range, citing direct fuel cost exposures in Q4 and investment to support customers. Endeavour reported FY26 half-to-date sales growth slowing to 0.7% in Retail and 3.7% in Hotels, down from 1.3% and 4.5% at the February half year, with Hotels momentum easing across food, bar, gaming and accommodation despite a record ANZAC Day. Ridley Corp and Nufarm both reported limited disruption.

Healthcare: Cochlear cut its FY26 underlying profit guidance by ~30%, triggered a 40% one-day selloff, EBOS also lowered guidance late last month.

The bottom line

Analysts still expect the ASX to deliver solid earnings growth in FY26, with Macquarie forecasting 10.5%, largely driven by the resource sector on the back of higher copper prices, stable iron ore, soaring gold (relative to last year), and a broad lift in prices across energy complex.

While index-level growth will lean heavily on banks and miners, the pressures emerging across industrials, consumers and healthcare point to clear headwinds beneath the hood.

While May is historically a quiet month for equities, whether the geopolitical, macro and corporate backdrop allows it to stay that way is another question.