How does the ASX 200 perform in June?

The market obsesses over the bearish months of May and September, but June is quietly worse, and this year's backdrop looks rather fragile.

.jpg)

Source: Shutterstock

KEY POINTS

- Since 1980, the ASX 200 has averaged a 0.40% June decline, rising just 43% of the time. That's the second-worst month and the only one positive under 50% of the time.

- The ASX 200 trades at around 16.7x forward earnings versus its 14.9x long-term average, though consensus tips strong EPS growth of 11.9% in FY26 and 12.3% in FY27.

- Domestic conditions look fragile, with business conditions falling four straight months and consumers staying pessimistic, but commodities and a possible Iran resolution offer the main upside.

Everyone talks about 'selling in May' and September being the market's worst month, but June is quietly one of the worst too.

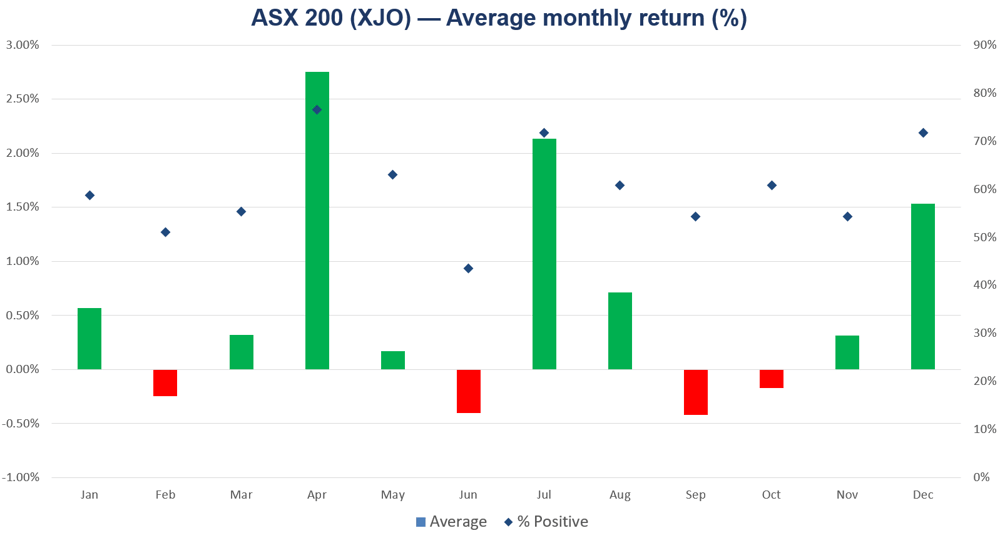

Since 1980, the S&P/ASX 200 has averaged a 0.40% decline in June and finished higher just 43% of the time. That makes it the second-worst month for performance, and the only one that's positive less than 50% of the time.

Source: Market Index

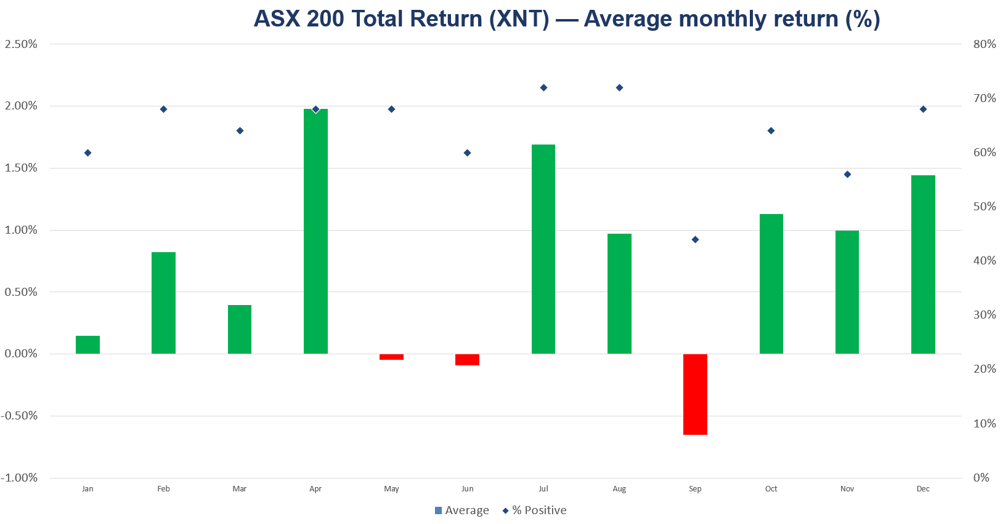

Our S&P/ASX 200 Total Returns data goes back to 2001, with an average decline of 0.09% and a positive hit rate of 60% for June. This still ranks as the second-worst month for performance and equal second-worst for positive returns.

Source: Market Index

The most recent Junes have performed slightly above the historical average, with a higher positive rate too.

Year | Jun (XJO) | Jun (XNT) |

|---|---|---|

2015 | -5.51% | -5.36% |

2016 | -2.70% | -2.52% |

2017 | -0.05% | 0.11% |

2018 | 3.04% | 3.20% |

2019 | 3.47% | 3.64% |

2020 | 2.47% | 2.57% |

2021 | 2.11% | 2.22% |

2022 | -8.92% | -8.81% |

2023 | 1.58% | 1.71% |

2024 | 0.85% | 0.97% |

2025 | 1.28% | 1.38% |

Source: Market Index

Where to from here?

The ASX 200 rose 0.76% last month, though it swung ~2% in either direction as it digested continued geopolitical and commodity price volatility, and the Federal Budget.

The market trades at a 12-month forward PE of approximately 16.7x compared to its long-term average of 14.9x, according to Morgan Stanley, though current consensus expectations are for robust growth in FY26 and FY27, with EPS growth of 11.9% and 12.3% respectively, largely driven by the materials and energy sectors.

The domestic outlook looks fragile, as the economy absorbs the fallout of the Federal Budget, ongoing RBA rate hikes and other headwinds. This has been apparent in economic data points, including:

The Westpac–Melbourne Institute Consumer Sentiment Index rose 3.5% to 83 in May as fuel excise relief (~30¢/litre off pump prices) partly offset the RBA's third consecutive 25bp hike, though consumers remain deeply pessimistic. Mortgage rate expectations climbed to a fresh three-year high with 85% of consumers anticipating further hikes, while the 'time to buy a dwelling' index plunged 16.1% to an 18-month low.

The NAB business confidence survey showed purchase-cost growth soaring threefold to 4.5% (in quarterly terms) in April, well ahead of final product price growth at 1.8%, with the margin squeeze most acute in manufacturing and construction. Business conditions fell for a fourth straight month to +3, the second-lowest reading since 2020 and a full unwinding of 2025's gains. Retail price growth jumped to a multi-year high of 3.2%, suggesting energy-driven cost pressures are now feeding into broader consumer inflation even as demand indicators soften.

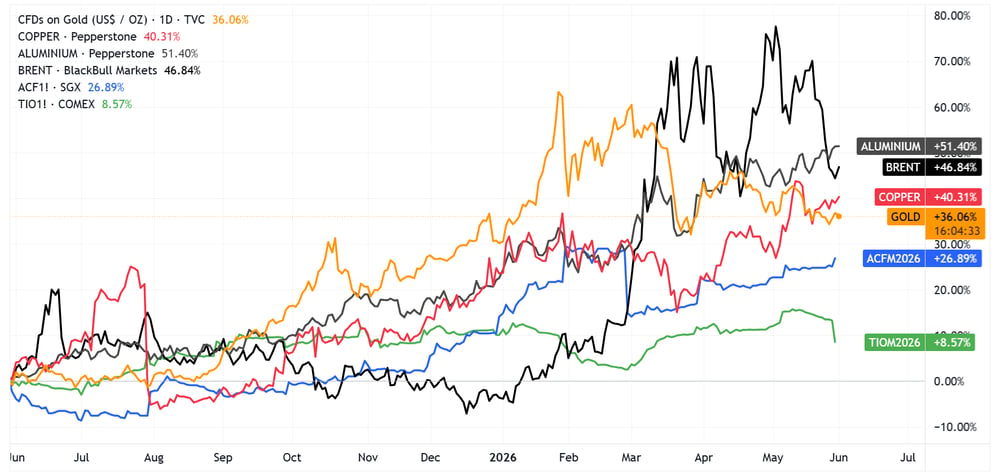

On the flip side, commodities have been a major bright spot, many of them already performing well before the Iran conflict.

Aluminium (grey), Brent (black), Copper (red), Gold (orange), coal futures (blue) and iron ore future (green) | Source: TradingView

In recent weeks, the market has become increasingly positive on Iran developments, and even sees any flare-ups as part of the noise ahead of a ceasefire extension and/or Strait reopening. Morgan Stanley notes the sectors that have had the strongest negative correlation with the oil price have been Discretionary, Industrials, REITs, and Healthcare.

"We would be cautious about assuming discretionary outperformance given the domestic headwinds the sector faces, but the other sectors could benefit if a resolution resulted in lower oil prices and yields," noted the analysts.

The bottom line: None of this means June is destined to disappoint, but with a fragile global backdrop and mounting domestic headwinds stacked on top of an already-soft month, the bright spots in commodities and a possible Iran resolution have a fair bit of work to do.