Gold's pullback looks temporary. Why Newmont and four other stocks are top picks

Macquarie lifted earnings forecasts and upgraded Evolution and Greatland, but cut targets across its gold coverage. Here is why.

Source: Shutterstock

Mentioned

KEY POINTS

- Macquarie upgraded Evolution Mining and Greatland Resources to Outperform and lifted near-term earnings forecasts across most of its gold coverage

- Target prices fell broadly because the bank switched to lower EV/EBITDA valuation multiples, which outweighed the earnings increases

- Newmont is the large-cap pick while Genesis and Capricorn are preferred in the mid-caps, with the whole thesis resting on a gold price recovery in CY27 and CY28

Macquarie has told clients to keep buying gold miners even as it cut its price targets across the sector, betting that a temporary dip in the gold price gives way to higher earnings in the years after.

The investment bank lifted near-term profit forecasts for most of its gold coverage and upgraded two stocks, Evolution Mining and Greatland Resources (from Neutral to Outperform). At the same time, it trimmed target prices for nearly every name it covers. The two moves look contradictory until you see what is driving them.

Earnings up, targets now

Gold has dipped back to breakeven for the year, with the Iran conflict stoking inflation concerns and weighing on the broader commodities complex. Against that backdrop, Macquarie changed how it forecasts gold prices and how it judges gold miner valuations.

Gold price chart (Source: TradingView)

On the gold price forecast: For the next two years, Macquarie has dropped its own gold price estimates in favour of the market-set forward curve, before reverting to a long-run US$3,100 an ounce from CY29. The curve has gold slightly lower this year, higher in 2027 at US$4,433, then easing to US$3,951 in 2028, shifting Macquarie's price deck -4% for CY26, +6% for CY27 and +4% for CY28.

On the valuation method: Macquarie also switched the short-term half of its valuation to an EV/EBITDA multiple from the operating cash flow multiple it used before. The new multiples are lower, at 8x for the large diversified miners against 9-11x previously, and that compression more than offset the earnings upgrades for most names, so target prices fell even as profit forecasts rose.

In laymans terms: Macquarie now expects these miners to earn more, but it also decided to pay a smaller multiple for those earnings, basically valuing each dollar of profit less generously than before. Because the lower multiple outweighed the higher profits, its price targets fell even as its earnings forecasts rose.

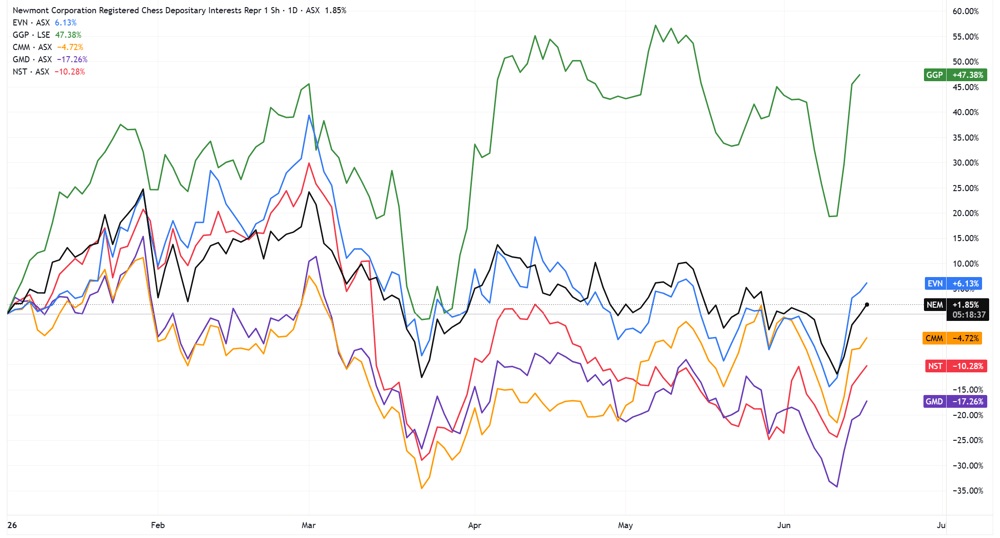

This drove broad target price cuts across the gold complex. Newmont fell 8% to $176.00, while Evolution Mining and Greatland both dropped 7%, to $13.00 and $14.00 respectively. Capricorn Metals held at $16.00 and Genesis Minerals at $9.00, with the multiple change offsetting the earnings lift rather than dragging those two lower. Northern Star stayed at $25.00.

Greatland (green), Evolution (blue), Newmont (black), Capricorn (orange), Northern Star (red) and Genesis (purple) year-to-date charts | Source: TradingView

The two upgrades

Evolution moved up to Outperform after a 3Q result that missed expectations and pulled the shares back. Macquarie sees production at Ernest Henry stabilising and output at Cowal normalising after weather disruptions in the December and March quarters. The company shifted to net cash in the March quarter, which the analysts argue should protect margins against peers if the gold price stays soft.

Greatland was upgraded after the recent pullback and the miner tracking ahead of its FY26 guidance of 230,000 to 310,000 ounces. A final investment decision on the Havieron project is due this quarter, and a possible spin-off of the O'Callaghans tungsten project sits as another catalyst. Despite operating high-quality, tier one assets, Telfer is the only producing asset until Havieron comes online, and single-asset miners carry more earnings risk.

Where Macquarie sees most upside

Newmont is the pick among the large caps. The analysts point to free cash flows of 10% per annum over the next three years, a US$6 billion buyback approved on top of US$1.9 billion already spent in the first quarter, and net cash of US$3.2 billion.

In the mid-caps, Genesis and Capricorn are the preferred names. Genesis trades at 5x EV/EBITDA on a one-year-forward basis, below its growth and large-cap peers. Its long-term production outlook, due in the first quarter of FY27, is the event to watch. Capricorn pairs steady output from Karlawinda with the Mt Gibson development, where federal permitting approval is expected around the fourth quarter of FY26.

But every part of this bullish thesis rests on the gold price. Current forecasts and assumptions bet on solid prices for 2026-27, and any further US-Iran escalation, stickier-than-expected inflation and a more hawkish Fed could upend gold's outlook.