Gold and silver suffer historic crash, wiping $7 trillion. Here's what you need to know

Overbought metals, margin hikes and hawkish Fed pick combine to trigger worst precious metals crash in four decades.

Source: Shutterstock

Mentioned

KEY POINTS

- Gold fell 12% to below US$5,000 and silver crashed 36% after surging 29% and 68% year to date respectively, with severely overbought conditions setting the stage for violent reversal

- CME Group implemented five margin hikes within nine days, progressively squeezing leveraged longs before Friday's second increase in 72 hours (33% for gold, 36% for silver) triggered mass forced liquidation

- Kevin Warsh's Fed Chair nomination was another key catalyst, with his hawkish stance on quantitative easing and preference for balance sheet discipline over open-ended liquidity accelerating the dollar rally and precious metals selloff

Gold and silver posted their worst single-day performances in decades last Friday, with more than US$7 trillion wiped from precious metals markets as a perfect storm of factors triggered mass liquidation of over-leveraged positions.

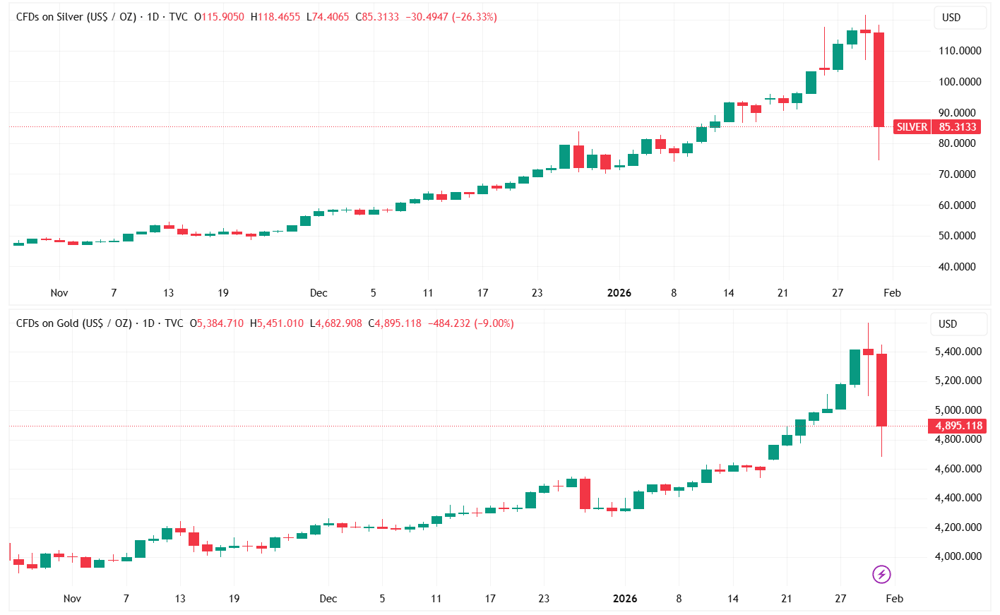

Gold plunged 9% from US$5,390 an ounce to US$4,895, marking its steepest decline since the early 1980s. Silver saw an even more dramatic collapse, dropping as much as 35% in what represents the largest intraday decline on record for the white metal. Silver closed the session 26% lower to US$85 an ounce, despite opening the session at US$115.

The crash came after gold had surged 29% year to date and silver had rocketed 68%, leaving both metals severely overbought with elevated speculative positioning and frothy sentiment.

Silver (TOP) and gold (bottom) daily price chart (Source: TradingView)

When CME Group announced its second margin increase in three days, followed by news that President Trump would nominate the hawkish Kevin Warsh as Federal Reserve Chair, the combination triggered a chain reaction of forced selling.

The selloff wiped ~US$5 trillion from gold markets and ~US$2 trillion from silver, with platinum and palladium also suffering losses of 27% and 21% respectively as speculative outflows swept through the metals complex.

Five margin hikes in nine days

The foundation for Friday's collapse was laid over the previous three weeks through a series of aggressive margin requirement increases by CME Group that progressively tightened the noose on leveraged traders.

On 13 January, CME shifted from fixed-dollar margins to percentage-based margins. This meant collateral requirements scaled with contract value, effectively capping leverage as prices climbed higher. Traders then faced five margin hikes within nine days, each forcing leveraged long positions to either post more capital or liquidate.

On Friday, CME announced its second increase in just 72 hours, with new requirements taking effect from Monday, 2 February:

Gold futures margins to 8% from 6%

Silver futures margins to 15% from 11%

The escalating requirements created what traders describe as a "coiled spring" of selling pressure. With metals prices having surged dramatically and leverage increasingly constrained, the market became primed for a violent reversal at the first sign of trouble.

Warsh's nomination

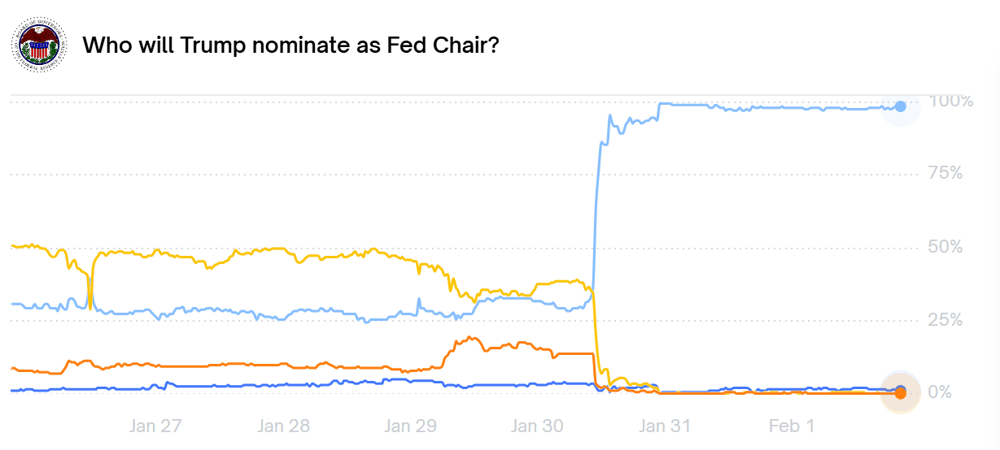

The catalyst that ignited the selling came when Trump confirmed he intends to nominate Kevin Warsh as the next Fed Chair. Markets view Warsh as a more hawkish choice compared to other candidates, raising expectations for tighter monetary policy that would support the US dollar and pressure commodity prices.

Warsh's probability of becoming Fed Chair was sitting around 31.5% on Friday morning but spiked to 95.5% by 1:30 pm AEST, broadly coinciding with when commodities started to roll over.

By 11:00 pm AEST, the likelihood had crossed 99%.

Next Fed Chair candidates (Source: Polymarket)

Why Warsh matters for markets

Warsh's policy record sets him apart from the accommodative stance markets have grown accustomed to, though his actual impact on monetary policy remains uncertain.

The 54-year-old served on the Federal Reserve Board from 2006 to 2011, developing a reputation as a competent crisis fighter during the 2008 financial crisis. Since leaving the Fed, he has become one of the most vocal critics of post-crisis monetary policy.

The key concern for markets is not simply whether rates will fall, but whether cuts will come with the balance sheet expansion that has characterised previous easing cycles. Warsh is a supply-side optimist who believes deregulation and tax cuts can spur productivity, potentially justifying lower rates. However, he has consistently argued for a smaller Fed balance sheet.

This creates uncertainty for investors who have relied on loose monetary policy to support asset prices. Markets are now pricing in the possibility of interest rate cuts without the accompanying liquidity injections that fuelled previous rallies in risk assets.

Technical factors

While the margin hikes set the stage and Warsh's nomination provided the trigger, precious metals had been primed for extreme moves after their parabolic rally.

Technical indicators had been flashing warning signals for weeks, with gold's relative strength index hitting 90, the highest reading in decades. RSI readings above 70 typically indicate an asset is overbought and due for a pullback.

The speed of the decline was accelerated by a gamma squeeze, where options dealers were forced to sell futures contracts to hedge their positions as prices fell through key strike levels. Large options positions were clustered at US$5,300, US$5,200 and US$5,100 for Comex gold futures. As prices tumbled and margin calls hit, over-leveraged longs were forced to liquidate, creating a self-reinforcing downward spiral of selling pressure.

Chinese liquidity

While Western markets focused on the Fed Chair appointment, pricing dislocations that emerged in Asian trading also played a significant role in silver's collapse.

The UBS SDIC Silver Futures Fund, a main source of silver exposure for Chinese investors, was trading at premiums of 36-64% over Shanghai Futures Exchange contracts. On 30 January, the Shenzhen Stock Exchange implemented an emergency full-day trading halt for the SDIC Silver ETF.

This suspension created a liquidity trap for Chinese institutional and retail traders. Unable to liquidate their domestic holdings, these participants were forced to dump positions in the SPDR Silver Trust ETF and Comex futures to raise cash or hedge their exposure, adding significant selling pressure to global markets.

Rally remains intact

Despite Friday's historic decline, precious metals remain substantially higher for the month and year. Gold still posted a 13% gain for January, while silver rose 19% for the month, marking nine consecutive months of gains.

The resilience of the broader rally reflects sustained investor demand driven by concerns about currency debasement, Fed independence, trade tensions and geopolitical uncertainty.

The bottom line

Friday's selloff serves as a stark reminder of the risks inherent in parabolic moves. Volatility is likely to remain elevated, with precious metals still substantially above their levels from 12 months ago and technical indicators suggesting stretched valuations. Looking ahead, it wouldn't be surprising to see sharp moves in both directions.