Cochlear crashes to decade low on guidance cut, worst selloff on record

Cochlear shares plunged 32% to a decade low after the company cut its FY26 profit guidance by ~30%, marking its worst selloff on record.

Source: Shutterstock

Mentioned

KEY POINTS

- Cochlear cut FY26 underlying net profit guidance to $290-330 million, a roughly 30% downgrade at the midpoint from the $435-460 million range issued just two months ago

- The new guidance implies a second-half profit of just $95-135 million, a 41% decline on the first half, with management blaming softer US volumes, European hospital constraints and a stronger Australian dollar

- Short interest has climbed from 0.40% to 5.82% over the past year, delivering short sellers an estimated $256 million payday on today's move

Cochlear (ASX: COH) shares opened 32% lower at a decade low of $113 after the hearing implant maker cut FY26 underlying net profit guidance by roughly 30% at the midpoint. Heading towards market close, the stock is now down 40% to $101.

This marks Cochlear's worst one-day selloff on record, and by a wide margin.

Date | Close | % Chg |

|---|---|---|

22/04/2026 | $101.40 | -39.7% |

16/12/2003 | $21.65 | -23.8% |

12/09/2011 | $57.50 | -20.3% |

16/03/2020 | $174.51 | -19.2% |

13/02/2026 | $199.22 | -18.9% |

3/06/2013 | $52.88 | -18.1% |

28/10/1997 | $3.80 | -15.9% |

12/03/2004 | $18.90 | -15.9% |

14/09/2011 | $51.30 | -14.6% |

14/02/2025 | $262.73 | -13.7% |

Data as at 3:00 pm AEST, Wednesday 22 April

Guidance decimated

The new $290-330 million range is a ~30% downgrade at the midpoint from the $435-460 million guidance issued just two months ago, when management flagged it would land at the lower end.

UBS had pencilled in FY26 underlying net profit of $408 million, leaving the midpoint of the new range 24% below its estimate. The downgrade also implies a 15-26% decline on FY25's $391 million result, which for a stock trading around 32x is not acceptable.

Cochlear's FY25 first-half to second-half earnings split was 52/48. The new guidance implies a split closer to 62/28, pointing to a severe deterioration in the second half.

Cochlear delivered $194.8 million in underlying net profit for the first half of FY26, so the new guidance implies just $95-135 million in the second half. That represents a 41% decline on the first half and a 38.2% drop on the prior period.

Why the cut

Management pointed to a stack of moving parts hitting the second half at once:

Sales growth in 2H now expected at 2-6% in constant currency, with developed market implant revenue flat in the third quarter

Up to $10 million in receivables provisioning related to the Middle East conflict

A roughly one percentage point gross margin hit from lower overhead recoveries (around $20 million net profit impact)

Cost base reshaping expenses of $18-25 million booked above the line

A circa $25 million after-tax drag from the stronger Australian dollar, with guidance now built on 71 US cents and 61 euro cents, versus 66 and 56 previously

Trading conditions deteriorated through the quarter, including:

US was in line with expectations until mid-February before volumes dropped in March

Hospital capacity constraints and growing surgical waiting lists in the UK and Germany held back Western European procedures, with industrial action in Italy and Spain compounding the issue

US consumer sentiment has hit historic lows, which is bleeding into discretionary healthcare decisions in the adults and seniors segment that has been Cochlear's main growth engine

Chief executive Dig Howitt said the data reinforces the case for Cochlear's "medicalise hearing loss" push, arguing that adult and senior hearing loss is still treated as a discretionary intervention rather than a clinical priority. He also flagged early traction from the Nucleus Nexa System and improving market share now that contracting is complete.

An (unfortunate) positive lead in

UBS flagged recent share price weakness in a 24 March note as "an opportunity, with the business positioned to deliver a solid earnings recovery over the next 12 months, underpinned by the Nexa launch." The broker had a Buy rating and a $302.00 price target.

That leaves Cochlear's downgrade looking like a left-field event and a complete U-turn against analyst expectations.

Despite the bullish analyst community, short interest in Cochlear has gone near vertical over the past twelve months, climbing from 0.40% a year ago to 5.82%.

Cochlear short interest (Source: Shortman)

Before today's selloff, Cochlear carried a market cap of approximately $11 billion. That implies a collective short position of around $640 million, or a $256 million payday for short sellers.

Where to from here?

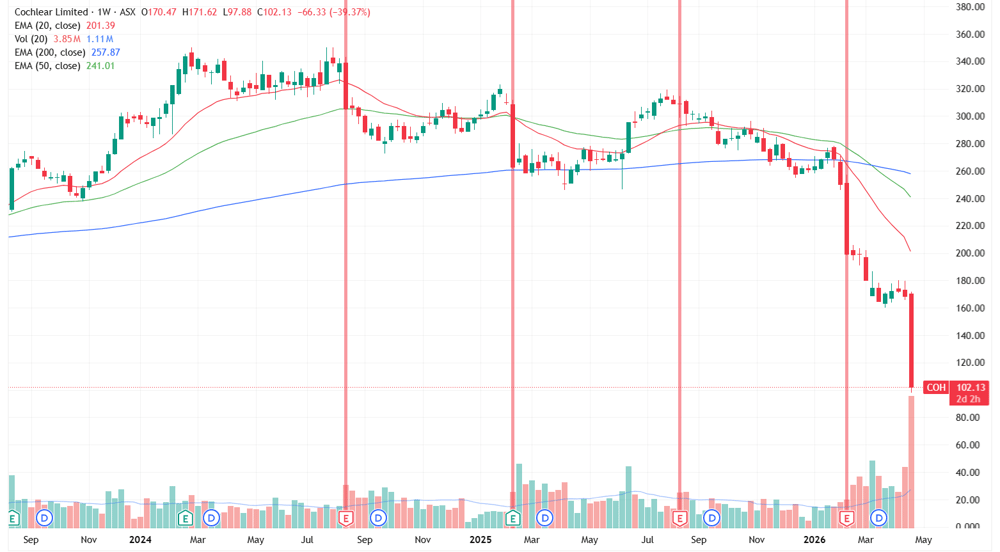

Cochlear shares have traded lower on every one of its past four earnings results, going back to the FY24 result on 12 August 2024.

Cochlear weekly price chart, earnings week marked in red (Source: TradingView)

While a case can be made around its historic growth rates and the fact the stock now trades at a "cheap" multiple relative to historical levels, Cochlear's recent track record suggests the path of least resistance is to stay well away. The chart also shows the stock tends to drift lower in the weeks and months following each earnings-related shock.