ASX growth stocks: Analysts just hiked this stock's target price by 46%

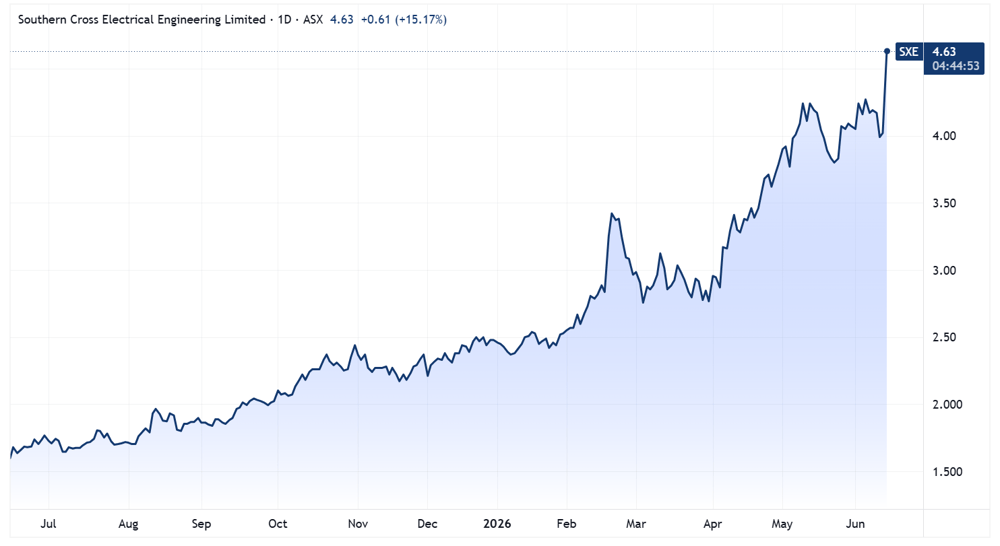

Southern Cross Electrical hit fresh all-time highs as blowout FY26-27 guidance offset the usual capital raise dilution and discount.

Source: iStock

Mentioned

KEY POINTS

- Southern Cross Electrical Engineering raised $150 million at just a 0.5% discount, with the placement pricing at the top of the bookbuild range on strong investor demand.

- Maiden FY27 EBITDA guidance of at least $100 million lands 26% above Bell Potter's February estimate. Contract wins from data centres, infrastructure and electrification are doing the heavy lifting.

- Bell Potter hiked its target price 46% to $5.40 this morning. The stock is currently up 16% to fresh all-time highs, lifting year-to-date gains to 85%.

Southern Cross Electrical Engineering (SXE) has raised $150 million to fund a supercharged growth outlook, headlined by a step-change FY27 EBITDA target of at least $100 million, which sits 26% above analyst expectations.

Capital raisings usually drag on the share price thanks to dilution and the discount on offer, but contracting momentum and a hefty earnings surprise have propelled the stock 16% higher this morning.

SCEE has been a stellar industrial growth story, with a revenue and net profit compound average growth rate of 11.5% and 19.5% respectively, since FY20. Before today's move, the stock had soared 148% in the last twelve months and 680% in the last five years.

Southern Cross Electrical Engineering 12-month price chart (Source: TradingView)

The capital raise comprises a $150 million institutional placement and a $15 million share purchase plan. The placement was priced at $4.00 per share, the top of the $3.85-4.00 bookbuild range, with the company citing "very strong support from both existing shareholders and new investors". This marks a tiny 0.5% discount to the previous close.

New works at a glance

SCEE said new works awards and growth initiatives support an upgraded FY26 guidance and a maiden FY27 guidance.

Secured over $150m of new works awards across multiple projects

Subsidiary Heyday awarded letter of authorisation to commence initial electrical and communications early works for Multiplex at NextDC S4 data centre

Subsidiary Trivantage supplying Low Voltage skids for a major data centre operator

Secured contract with Rio Tinto for Pilbara EIC (Electrical, Instrumentation and Communications) work

Expanded bank and bond funding capacity to $200m, with new $50m revolving credit facility and $50m acquisition facility

Appointment of experienced COO on East Coast, Peter Bierton, to support next phase of growth

Manufacturing footprint has more than doubled to 17,000m2

Earnings upgrade

This is the second FY26 EBITDA guidance upgrade since last August.

Aug-25: Initial guidance set at $65-68m

Mar-26: Guidance upgraded to at least $72m

Today: Guidance upgraded to at least $75m, representing a 4.1% upgrade against the prior guidance.

SCEE expects a step-change heading into FY27, with earnings powered by further momentum across data centres, infrastructure and renewables/electrification. The company guided to FY27 EBITDA of at least $100 million, 26.4% above Bell Potter's February 2026 estimate of $79.1 million.

Capital raisings usually weigh on the share price through discount and dilution, but here, the catalyst behind the raise far outweighs the negatives.

On the pre-raise market cap (~$1bn) and Bell Potter's estimates (Feb-26), the business traded at 12.6x EBITDA. On the post-raise market cap (~$1.23bn) and new guidance, it sits at 12.3x EBITDA, but with a far stronger growth outlook.

The bottom line

SCEE is one of many industrial names that keep on giving, supported by broad structural tailwinds across data centres, infrastructure, renewables, defence and more.

Capital raisings are dilutive, but this one was struck at a minimal discount on strong investor demand, and well offset by the FY26-27 earnings upgrade. In response to the new guidance, Bell Potter hiked its target price 46% from $3.70 to $5.40, citing "a more optimistic medium-term revenue growth outlook, underpinned by rising investment momentum in the Data Centre and BESS construction markets".

The stock is looking frothy, with year-to-date gains now at 85%, but fundamentally things keep moving in the right direction.