ASX Dividend Stocks: A recovery play that's yielded 7-9% in the last four years

Cash Converters has paid a steady 2 cents per share dividend since FY21, delivering 7-9% yields before a recent 70% share price surge.

Source: Shutterstock

Mentioned

KEY POINTS

- Cash Converters has paid a consistent 2 cents per share dividend every year since FY21, previously yielding 7-9% before recent share price gains brought the trailing yield to 6.0%.

- The company is targeting 20+ store acquisitions annually, with stores historically acquired at EBITDA multiples below 5x and delivering IRRs above 15%.

- Revenue has grown from $201.3 million in FY21 to $385.3 million in FY25, while operating profit increased from $15.0 million to $25.1 million over the same period.

I'm on a mission to uncover some of the market's most interesting dividend-paying stocks, providing readers with the key data and forecasts to make more informed decisions. Today, we're reviewing Cash Converters.

You probably haven't seen a Cash Converters (ASX: CCV) ad or physical store in a while, but the company is quietly staging a comeback. The past couple of years have marked a major turnaround amid a focus on high-margin luxury goods and diversification into credit solutions.

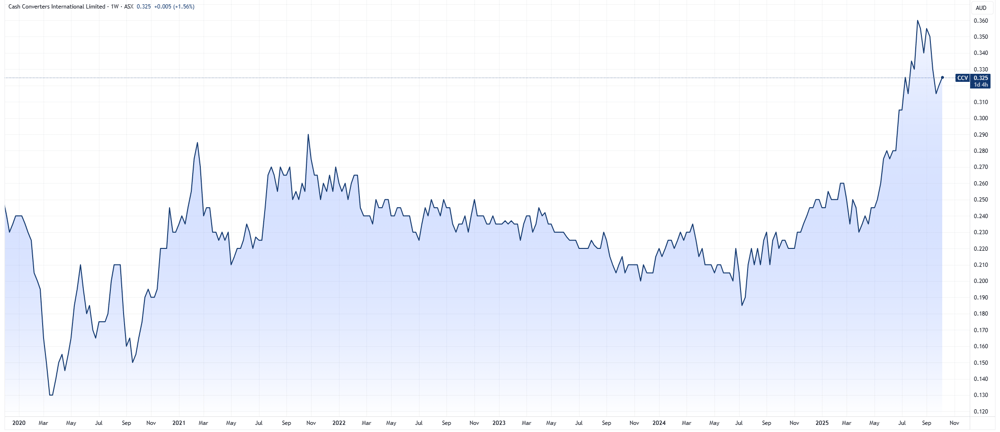

This turnaround has driven a 70% share price increase since August 2024. Prior to that, the stock traded sideways from the pandemic through mid-2024.

Cash Converters price chart (Source: TradingView)

What's notable is that throughout this entire period, CCV has paid a steady 2 cents per share dividend every year since FY21. With the share price largely flat until recently, that delivered yields of 7-9%.

Consistent dividends

Based on dividend history alone, you'd expect this to be a REIT or utilities company.

FY25 | FY24 | FY23 | FY22 | FY21 | |

|---|---|---|---|---|---|

DPS (cents) | 2.00 | 2.00 | 2.00 | 2.00 | 2.00 |

Dividend yield (%) | 7.1% | 9.0% | 8.8% | 8.7% | 9.0% |

Payout ratio (%) | 61% | 62% | 57% | 60% | 78% |

Source: Market Index

These stable dividends have been supported by solid revenue and earnings growth.

The most notable figure below is likely the $97.2 million statutory loss in FY23. This reflects a one-off impairment of goodwill and assets tied to its SACC (Small Amount Credit Contract) business following regulatory changes. New rules capped the portion of borrower income that can go toward loan repayments, limiting how much CCV can lend and earn from each small loan.

FY25 | FY24 | FY23 | FY22 | FY21 | |

|---|---|---|---|---|---|

Revenue ($m) | 385.3 | 382.6 | 302.7 | 245.9 | 201.3 |

% Chg (pcp) | 0.70% | 26.3% | 23.0% | 22.1% | ~ |

Operating NPAT ($m) | 25.1 | 20.9 | 20.1 | 19.0 | 15.0 |

% Chg | 20.0% | 3.9% | 5.7% | 26.6% | ~ |

Statutory NPAT ($m) | 24.4 | 17.3 | -97.2 | 11.2 | 20.7 |

Cash ($m) | 73.2 | 56.3 | 71.6 | 58.1 | 72.1 |

Source: Company reports

Looking ahead

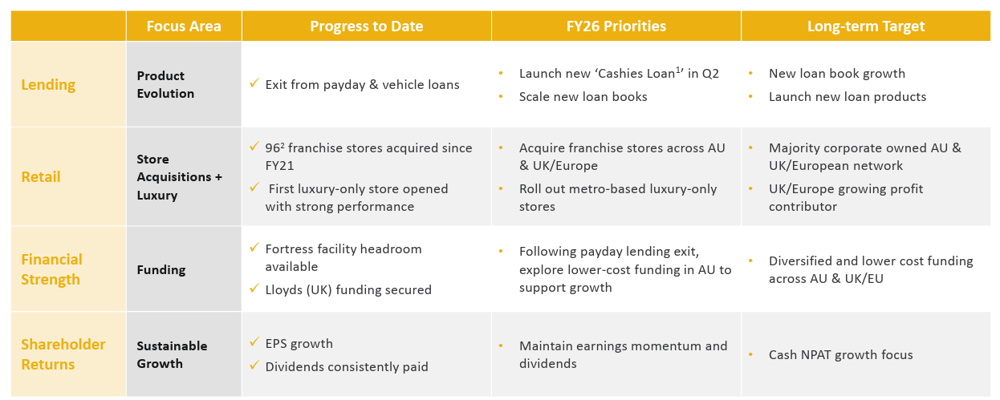

Management is working to simplify and launch new lending products while expanding the retail network through store acquisitions across Australia, the UK, and Europe.

Source: Cash Converters FY25 results presentation

For context, retail stores generated 41.9% of FY25 revenue ($161.4m), personal finance contributed 23.5% ($90.5m), with the remainder from vehicle financing and UK/NZ operations.

Given the company's $200m market cap, there's no broker coverage. Management has provided these targets:

Targeting 20+ franchise store acquisitions per annum to drive earnings upside

The average Australia and UK-based store generated revenue of $2.0 million and $1.6 million respectively in FY25, with both generating approximately $200,000 net profit per store

Australian stores have to date been funded via existing cash, while recent UK rollout was supported by a £12 million facility

The bottom line

Cash Converters isn't a high-profile brand, but the company has delivered consistent earnings growth and dividends over the past few years.

The acquisition-focused growth strategy appears to be working. According to the FY25 presentation, stores have typically been acquired for $1m in Australia and £600k in the UK, representing EBITDA multiples below 5x with IRRs above 15%. Given these returns, management plans to ramp up acquisition activity.

Following recent share price gains, the stock now trades at a 6.0% trailing dividend yield.