ASX 200 Live Today - Wednesday, 21st January

The S&P/ASX 200 is set to tumble as the Greenland dispute triggered a broad selloff. Here are today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Wednesday, January 21. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Be sure to refresh manually for the latest updates — and let us know how we can make it even better.

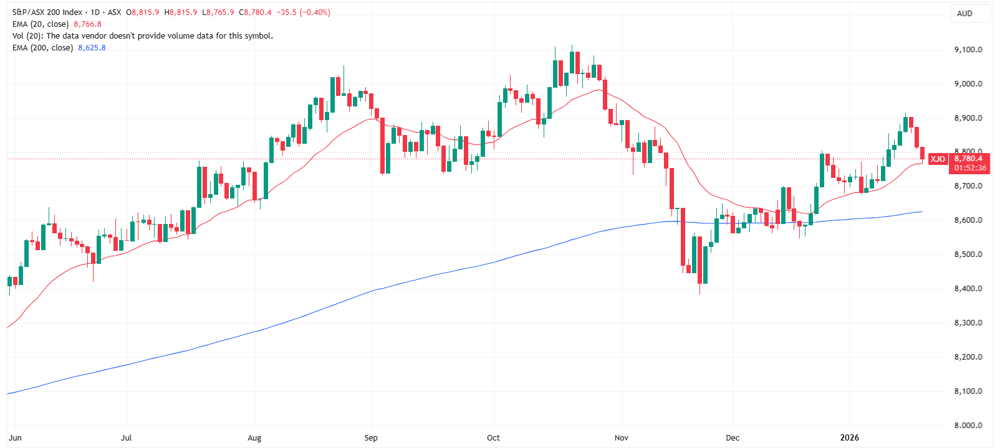

ASX 200 lower for a third straight session

[2:15 pm] ASX 200 down 0.45%, trading near session lows and slightly above the 20-day moving average. The index is down 1.46% in the last three sessions, which largely reflects a 3.2% decline in the heavyweight Financials (XFJ) sector, as well as some softness from Tech (-4.3%), Telcos (-2.4%) and Real Estate (-2.4%).

This weakness has been partly offset by Materials and Energy, which have gained 1.5% and 0.3% over the same time period.

Overall, things a getting a little dicey out there, against this escalating geopolitical backdrop and rising bond yields (Australia 10-year is snapping a four-day win streak today, where it ran 12 bps to 4.79%).

ASX 200 daily price chart (Source: TradingView)

Ballard Mining halted for $50m placement

[1:27 pm] Shares in Ballard Mining halted this morning, pending an announcement regarding a proposed capital raising. The slide decks for the raise just came out, noting:

Seeking to raise $50 million at 80 cents per share (14% discount to last close)

Funds to support 220,000m of drilling planned for 2026, grow camp scale and transition the project towards a final investment decision

Ballard is up 38% year-to-date and up 151% since debuting on the ASX back in July 2025.

Company page: Ballard Mining (BM1)

Lithium stocks broadly higher

[12:37 pm] Lithium stocks are trading broadly higher, with the bellwether Pilbara Minerals up 3.3%, pretty much back at recent highs.

Chinese lithium futures open at 12:00 pm AEST, and currently up 5.0% to 163,000 yuan a tonne. Prices experienced a sharp ~9% drawdown in the past week, but now back up to breakeven and within 6% of recent highs (174,060 yuan).

Ticker | Company | % Chg | Price |

|---|---|---|---|

LKE | Lake Resources | 15.00% | $0.12 |

INR | Ioneer | 9.76% | $0.23 |

AGY | Argosy Minerals | 9.37% | $0.11 |

CXO | Core Lithium | 7.41% | $0.29 |

WR1 | Winsome Resources | 5.66% | $0.56 |

VUL | Vulcan Energy Resources | 5.29% | $4.38 |

5EA | 5E Advanced Materials | 5.26% | $0.60 |

LTR | Liontown | 3.59% | $2.17 |

GL1 | Global Lithium Resources | 3.57% | $0.58 |

PLS | PLS Group | 3.16% | $4.89 |

DLI | Delta Lithium | 1.79% | $0.29 |

PMT | Pmet Resources | 1.53% | $0.67 |

IGO | IGO | 0.83% | $9.07 |

MIN | Mineral Resources | 0.38% | $60.40 |

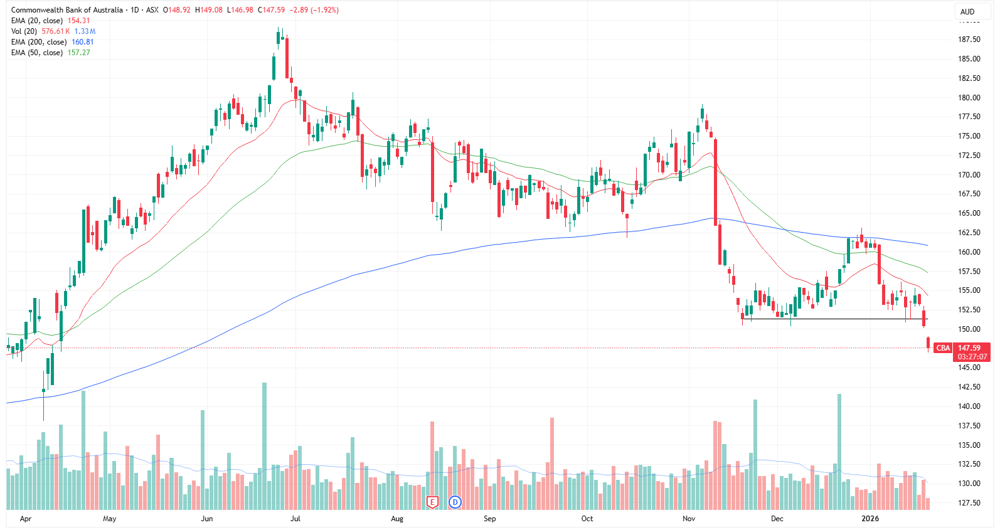

CBA undercuts recent low

[12:35 pm] CBA is looking even more wobbly, down 1.8% ($147.68) at noon and marking a clear break down from recent lows. The stock is now trading at the lowest since 9 April 2025, and just 4% away from Liberation Day lows.

CBA daily price chart (Source: TradingView)

Intraday runners: Paladin Energy, Evolution

[12:09 pm] Running the intraday scan again (this shows the % change vs. the open price). Paladin Energy and Evolution Mining have both experienced a massive morning drive thanks to better-than-expected December quarter production reports, also seeing a broad bid for various resources (GOLD, base metals)

Ticker | Company | % Chg vs. Open | Price |

|---|---|---|---|

PDN | Paladin Energy | 9.94% | $13.16 |

EVN | Evolution Mining | 7.35% | $14.60 |

ZIM | Zimplats | 4.85% | $24.44 |

EMR | Emerald Resources | 3.81% | $7.50 |

ORG | Origin Energy | 3.19% | $11.66 |

4DX | 4DMedical | 2.88% | $4.28 |

LYC | Lynas Rare Earths | 2.68% | $16.10 |

BPT | Beach Energy | 2.25% | $1.14 |

SMR | Stanmore Resources | 2.03% | $3.01 |

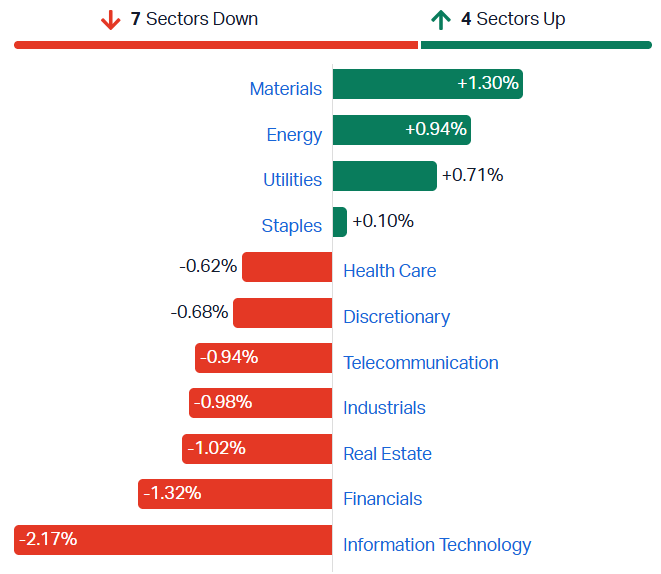

ASX 200 Materials rebounds

[11:28 am] The ASX 200 Materials Index is up 1.49%, recovering all of yesterday's losses and on track to close at fresh all-time highs. The move also comes as the US dollar eased overnight, which can support commodity prices and flow through to the Materials sector.

Ticker | Company | % Chg | Price |

|---|---|---|---|

EVN | Evolution Mining | 7.03% | $14.46 |

LYC | Lynas Rare Earths | 5.84% | $16.14 |

ZIM | Zimplats | 5.68% | $24.20 |

BGL | Bellevue Gold | 4.49% | $1.86 |

PLS | Pls Group | 3.27% | $4.90 |

ASX 200 sector performance (Source: TradingView)

By Warren Masilamony

ASX 200 lower, miners buoy the market

[11:13 am] A fairly tame open as the ASX 200 slips 0.37%. The market's down for a third straight session, but it could be far worse if not for the resource sector, with Materials (+1.30%) back up towards record highs. Still seeing risk-off sentiment come in the form of continued selling in the Tech sector (-2.1%), which is now on track to undercut April-25 lows as well as weakness in Financials (-1.3%) and yield-sensitive sectors like Real Estate (-1.0%).

ASX 200 sector performance (Source: TradingView)

Growth stocks continue to struggle

[10:34 am] A broad basket of growth/tech stocks are leading the downside today, with badly beaten names like Xero, Pro Medicus and ARB Corp continuing to trend lower.

Ticker | Company | % Chg | Price |

|---|---|---|---|

SLX | Silex Systems | -4.90% | $6.79 |

GDG | Generation Development Group | -4.87% | $5.86 |

DRO | Droneshield | -4.22% | $4.54 |

XRO | Xero | -3.84% | $100.27 |

LNW | Light & Wonder | -3.02% | $169.11 |

ARB | ARB Corp | -2.96% | $27.58 |

PME | Pro Medicus | -2.92% | $181.10 |

LOV | Lovisa | -2.91% | $30.15 |

TLX | Telix Pharmaceuticals | -2.87% | $11.16 |

MP1 | Megaport | -2.68% | $12.00 |

Top ASX 200 gainers: Uranium and gold

[10:32 am] Paladin Energy tops the leaderboard after reporting better-than-expected December quarter production numbers and an upgraded (towards upper end of guidance) FY26 production guidance. Gold miners are also trading broadly higher, some off the back of solid quarterly updates, but mostly thanks to the soaring gold price.

Ticker | Company | % Chg | Price |

|---|---|---|---|

PDN | Paladin Energy | 9.88% | $12.79 |

WGX | Westgold Resources | 9.10% | $7.50 |

EVN | Evolution Mining | 4.59% | $14.13 |

AAI | Alcoa Corporation | 4.40% | $92.48 |

LYC | Lynas Rare Earths | 4.20% | $15.89 |

ZIM | Zimplats | 4.19% | $23.86 |

EMR | Emerald Resources | 4.13% | $7.32 |

SNZ | Summerset Group | 3.96% | $10.50 |

BGL | Bellevue Gold | 3.09% | $1.84 |

RMS | Ramelius Resources | 2.93% | $4.75 |

Coast Entertainment 1H26 update

[9:56 am] Coast Entertainment highlighted record ticket sales and revenue for the first half of FY26, supported by new attractions and strong visitation numbers.

Ticket sales up 46.6% vs 1H25 (38.0% like-for-like), surpassing previous peak levels

Total visitation up 44.4% vs 1H25 (32.4% like-for-like), with record daily attendance at Dreamworld

Operating revenue $62.2m, up 30.2% vs 1H25 (21.8% like-for-like)

Broader commentary:

Growth driven by new King Claw ride, Rivertown opening and targeted promotional campaigns

Food, Beverage and Retail revenues exceeded prior peak levels, reflecting higher in-park spending

EBITDA (ex-specific items) expected to rise materially, leveraging largely fixed cost base

Early January trading shows continued positive trends, though at more moderate levels post-peak season

Company page: Coast Entertainment (CEH)

Rio Tinto Q4 commodity commentary

[9:49 am] Some fairly interesting commodity commentary accompanied Rio Tinto's December quarter report. The key takeaways include:

Global & China macro: Global growth slowed in Q4, inflationary pressures eased, and China’s economy remained export- and production-driven, with weak consumption and property markets. Policy focus is on advanced manufacturing, technology, green transition, and modest near-term stimulus.

US macro: Resilient despite Q4 government shutdown, easing borrowing costs, narrower credit spreads and stronger equity markets supported business and household confidence.

Iron ore: China’s steel consumption stable QoQ, seaborne shipments up 4% QoQ and 2% YoY, driven by non-major producers, China portside inventories rose 21Mt to 166Mt.

Copper: LME prices surged to $5.67/lb driven by US rate cuts, AI-related demand, and supply disruptions. CME prices averaged ~$0.10/lb higher due to import tariff risks, copper concentrate market extremely tight with spot treatment and refining charges hitting all-time lows.

Aluminium & alumina: LME prices reached highest since Q2 2022; premiums in US and Europe rose on tighter supply expectations and CBAM-related front-loading, Australian FOB alumina prices fell due to higher Indonesian/Chinese supply.

Lithium: Lithium carbonate prices up 55% in Q4 amid strong battery and EV demand, rapid EV sales growth drives upward revisions to lithium demand expectations.

Other commodities: Borates stable, titanium dioxide demand soft with elevated inventories and reduced feedstock purchases.

Company page: Rio Tinto (RIO)

Rio Tinto Q4 production report

[9:44 am] Rio Tinto delivered an operationally strong report, with both December quarter and full-year numbers hitting company guidance and ahead of consensus expectations.

Q4 2025:

Pilbara iron ore shipments 91.3Mt vs. 88.1Mt ests (4% beat)

Pilbara iron ore production 89.7Mt vs. 87.7Mt ests (2% beat)

Bauxite 15.4Mt vs. 14.6Mt ests (5% beat)

Alumina 2.0Mt vs. 1.933Mt ests (4% beat)

Aluminium 0.85Mt vs. 0.841Mt ests (1% beat)

Copper 240kt vs. 217kt ests (11% beat)

2025:

Pilbara iron ore shipments 326.2Mt vs. lower end of 323-338Mt guidance (within guidance)

Pilbara iron ore production 327.3Mt vs. 323-338Mt guidance (within guidance)

Bauxite 62.4Mt vs. >61Mt guidance (beat)

Alumina 7.6Mt vs. 7.4-7.8Mt guidance (within guidance)

Aluminium 3.38Mt vs. 3.25-3.45Mt guidance (within guidance)

Copper 883kt vs. 860-875kt guidance (+6% beat)

Commentary (by commodity):

Copper equivalent (CuEq) production rose 8% YoY in 2025, with shipments up 5%, supported by Oyu Tolgoi ramp-up, record bauxite output, and strong lithium performance.

Iron ore: Pilbara achieved record Q4 production (+4% YoY) and shipments (+7% YoY); Simandou started operations and shipped its first cargo in Q4.

Aluminium: Demonstrated production strength and operational agility across the value chain in 2025.

Lithium: Delivered record quarterly production from operating assets in Argentina.

Copper: Annual production grew 11% YoY, exceeding the top end of guidance, driven by Oyu Tolgoi’s ramp-up and completion of the underground development project.

Company page: Rio Tinto (RIO)

Paladin Energy 2Q26 report

[9:34 am] Some very strong December quarter numbers from Paladin Energy.

Uranium production of 1.23Mlb vs. 1.03Mlb ests (19% beat)

Uranium sold of 1.43Mlb vs. 1.225Mlb ests (17% beat)

Average realised price of US$71.8/lb vs. $70.1/lb ests (2% beat)

Guidance update: "Given the robust production in the first half of FY2026 coupled with the continued ramp up of LHM to full mining and processing operations by the end of FY2026, the Company expects full year production to trend towards the upper end of the guidance range of 4.0 to 4.4Mlb"

Management commentary: “As global interest in nuclear energy continues to strengthen, I am delighted by our progress in ramping-up operations at Langer Heinrich Mine. The new level of production achieved during the quarter provides insight into the robust performance that can be achieved from this strategic uranium asset."

Company page: Paladin Energy (PDN)

Evolution Mining 2Q26 report

[9:29 am] Evolution reported a relatively sound December quarter result, with production relatively in-line with market expectations.

Group gold production of 191koz vs. 186koz ests (3% beat)

Copper production of 18kt vs. 19kt ests (5% miss)

AISC of $1,275/oz vs. $1,726/oz ests (not sure if comparable)

On track to deliver FY26 production at "lower than original cost guidance"

The earnings growth, both in absolute terms and relative to the prior period, shows just how leveraged gold miners are to the rising gold price.

Operating mine cash flow (2Q26) up 57% quarter-on-quarter to $1.1bn

Net mine cash flow of $727m, Group cash flow of $412m

Gearing is now just 6% vs. 11% in September and 33% at 31-Dec-23

Company page: Evolution Mining (EVN)

Vault Mineral 2Q26 report

[9:15 am] Vault's December quarter numbers appear broadly weaker-than-expected, though the company reaffirmed its full-year guidance, alongside upbeat management commentary.

Gold production of 76.5koz vs. 87.8koz ests (13% miss)

Gold sales of 77.8koz vs. 87.5koz ests (11% miss)

AISC of $3,160/oz vs. $2,820/oz ests (12% cost miss)

Achieved gold price of $4,582/oz vs. $4,564/oz ests (0.4% beat)

Gold hedge book reduced by 87,864 ounces, resulting in Vault now being materially unhedged

Guidance reaffirmed: "Vault is well positioned to deliver on its FY26 production guidance of 332,000 – 360,000 ounces, with first half capital investments strengthening the operating platform and supporting a clear pathway to sustained, high‑margin production."

Company page: Vault Minerals (VAU)

Gold and silver soar to fresh all-time highs

[9:10 am] Another record setting session for classic safe havens, with gold up 3.6% to US$4,763/oz and silver up 5.0% to US$94.5/oz. I'd chuck a price chart here but there's really no point – they're both fairly vertical.

What's more remarkable is that gold and silver equities continued to soar despite the risk-off tone dominating the overnight session. These miners sometimes sell off alongside the broader market even when the underlying commodity price rises, but not this time.

The VanEck Gold Miner ETF and Global X Silver Miner ETF rallied 5.7% and 5.1% respectively, both closing at fresh all-time highs.

Greenland rift dominates Davos agenda

[9:05 am] Geopolitical tensions between the US and Europe over Greenland set the tone at Davos, amplifying market unease and raising questions over alliances, trade and financial stability.

European leaders openly pushed back against Trump’s Greenland ambitions, with Macron calling tariff threats unacceptable and warning Europe must build greater sovereignty to avoid strategic subordination

Denmark’s AkademikerPension plans to exit US Treasuries, citing concerns over US creditworthiness and political risk, a small but symbolically important shift in perceptions of safe havens

UK Chancellor Rachel Reeves struck a calming tone on both geopolitics and fiscal policy, stressing budget discipline and warning against locking in future tax decisions amid global uncertainty

Broader Davos discussions underscored rising global fragmentation, spanning AI export controls to China, Ukraine war risks and European fiscal instability, reinforcing a backdrop of elevated political risk for markets

Source: Bloomberg

China rolls out targeted fiscal support

[9:02 am] Beijing unveiled a fresh package of credit and fiscal incentives on Tuesday, aimed at reviving private investment and consumption amid weak domestic demand.

A 500bn yuan, two-year loan guarantee facility will support private firms borrowing for expansion, equipment purchases and technology upgrades, directly targeting financing constraints

Small and medium-sized enterprises will receive interest subsidies of up to 1.5 percentage points for two years on loans of up to 50m yuan, lowering effective borrowing costs

Officials signalled a more active fiscal stance in 2026, with higher public spending and government bond issuance kept at “necessary” levels to support consumption and household welfare

The measures mark a shift from the previously cautious stimulus approach, following data showing export strength masking weak consumption and a sharp investment slowdown

Source: Bloomberg

Crypto sells off as macro risk spikes

[8:53 am] Bitcoin and broader crypto markets fell in line with a global risk-off move as geopolitical tensions and bond market stress drove investors to cut exposure.

Bitcoin dropped below $90,000 for the first time since early January, down 3.4% on the day, tracking selloffs in equities, long-dated Treasuries and Japanese bonds.

Bitcoin price chart (Source: TradingView)

Losses were sharper in smaller tokens, with Ether down over 7% and Solana off 5.3%, highlighting reduced liquidity and higher beta during periods of market stress

Crypto-linked equities underperformed, with Coinbase down more than 5% and Strategy shares sliding almost 10%, despite continued accumulation of Bitcoin by the company

The sell-off reflects broader macro forces rather than crypto-specific weakness, with tariff threats and Greenland-related tensions fuelling demand for traditional safe havens like gold

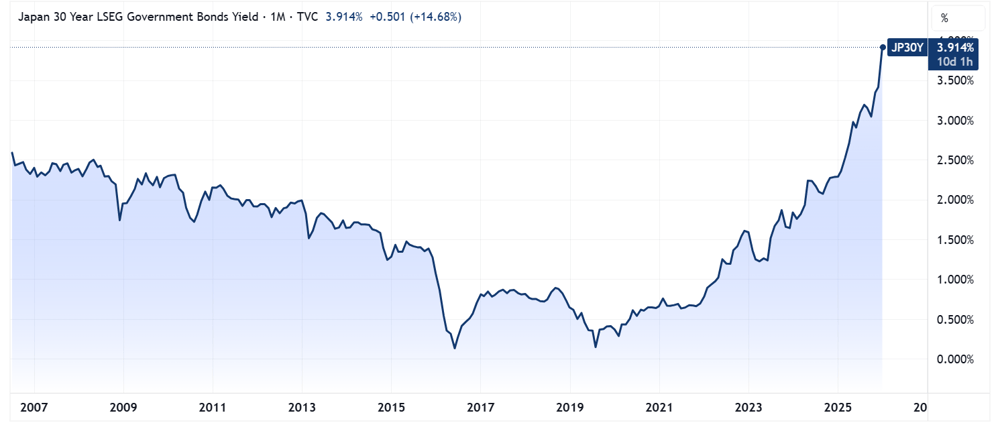

Japan bond rout sparks fiscal credibility fears

[8:51 am] A sudden collapse in Japan’s long-dated bond market exposed deep investor anxiety over fiscal sustainability, triggering violent yield moves and stress across credit markets.

Yields on 30 and 40 year JGBs surged more than 25 bps in a single session, the largest move since last year’s tariff shock, as a weak 20-year auction tipped simmering fiscal concerns into outright panic.

Japan 30-year bond yield chart (Source: TradingView)

Prime Minister Takaichi’s plan to cut taxes and boost spending reignited fears of unfunded deficits, with investors likening the sell-off to a “Liz Truss moment” for Japan

Forced unwinds hit hedge funds and life insurers, while dislocations were severe enough to derail multi-million dollar corporate bond deals and push high-grade credit yields to record highs

Global investors used the turmoil to rotate, with some selling US Treasuries to buy JGBs, underscoring how extreme the pricing became during the rout

Persistent fiscal doubts and rising rates threaten to keep pressure on Japanese government bonds, particularly for insurers who may struggle to re-enter even at higher yields

Source: Bloomberg

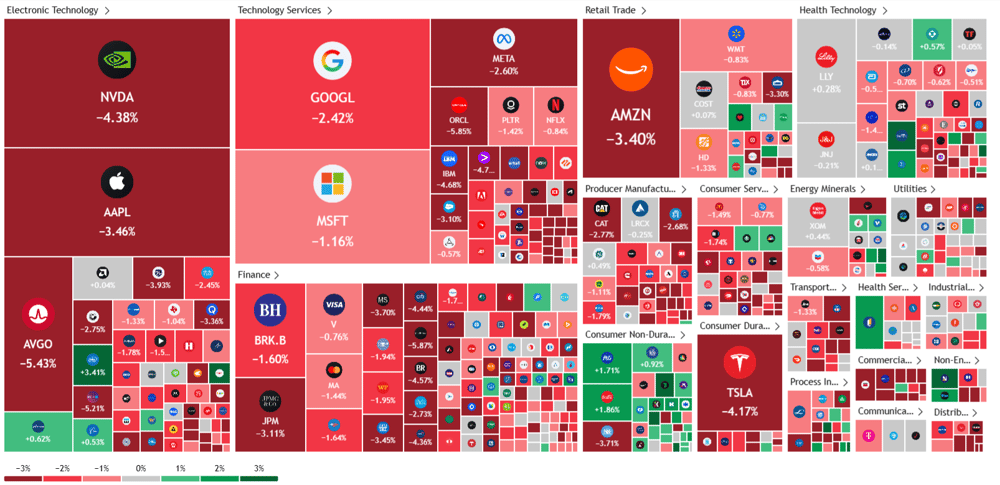

S&P 500 sectors broadly lower

[8:46 am] A rather heavy overnight session, where ten out of eleven S&P 500 sectors finished lower. Notable decliners include Tech (-2.94%), Discretionary (-2.82%), Financials (-2.23%) and Communication Services (-2.06%). Only Staples (+0.12%) managed to buck the trend, while Energy (-0.17%) and Healthcare (-0.21%) also outperformed on a relative basis.

S&P 500 heatmap (Source: TradingView)

Trump tariff threats trigger global risk-Off

[8:43 am] Markets sold off sharply as Trump’s renewed tariff threats and Greenland tensions reignited geopolitical risk and challenged US asset exceptionalism.

S&P 500 fell 2%, wiping out its 2026 gains, while equity volatility jumped to the highest level since November, marking the worst cross-asset session since April’s tariff shock

Long-end US yields rose despite equity losses, with the 10-year at 4.29%, as foreign demand concerns grew amid Japanese bond turmoil and reports of European investors diversifying away from Treasuries

The US dollar suffered its worst two-day run in a month, while gold surged to record highs above $4,700 an ounce, reinforcing demand for hedges as policy uncertainty escalated

Bitcoin sank below $90,000 and US megacap tech dropped 2.9%, extending the rotation toward small caps, defensives, gold and non-US equities

Investors remain split between viewing tariff threats as negotiation tactics and fearing a deeper regime shift, with positioning stretched as optimism sits near five-year highs and downside protection at cycle lows

Good morning!

[8:38 am] ASX 200 futures are down 49pts (-0.56%) as of 8:30 am AEDT. The overnight session in a nutshell:

Major US benchmarks finished sharply lower, recording the worst session since last October

Trump threatened tariffs on various European countries ahead of the Davos meeting

Gold surged more than 3% to a record US$4,758/oz, silver also up almost 5% to US$94/oz

To catch up on all overnight developments, check out today's Morning Wrap.