ASX 200 Live Today - Tuesday, 3rd March

The S&P/ASX 200 is set to slip after four straight days of record highs. Here are today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Tuesday, March 3. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

Risk-off sentiment sweeps across global markets

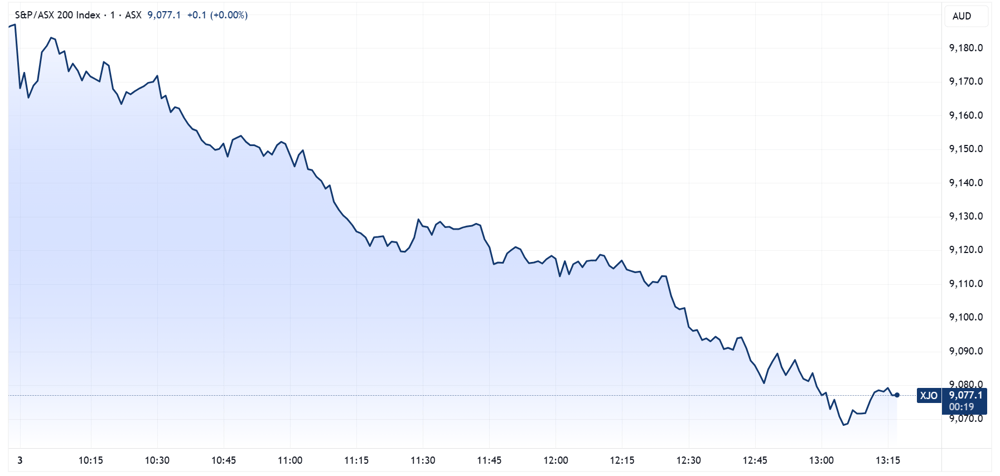

[2:30 pm] A heavy day for markets. The ASX 200 hit a session low of -1.45% and is currently sitting at -1.17%, though no single catalyst stands out as the clear driver. South Korea's KOSPI dropped 4.3% (notable given it was up as much as 50% YTD just days ago), while China's SSE Composite recovered from a -1.2% low to trade near flat. The broader volatility follows a sharp move in oil prices and bond yields, with global bonds suffering their worst session since May. Markets have a habit of looking through geopolitical flare-ups, but this one carries real implications for oil and inflation, so it's worth watching closely. On the sentiment and positioning side, a number of indicators (mostly US-based) are pulling back from frothy levels: AAII bears have outweighed bulls for a second consecutive week, the NAAIM exposure index is at its lowest since May 2025, software shorts are at historic levels, and the 10-day equity put/call ratio is the highest since April 2025. If the Middle East situation stays contained, and you factor in the reset in positioning and sentiment alongside a strong February reporting season, it's hard not to feel at least a little constructive from here.

ASX 200 dips, still making fresh lows

[1:20 pm] Selling pressure has continued to intensify, with the ASX 200 down 1.4% vs. a ~0.8% decline just two hours ago. Sectors including Real Estate, Discretionary and Materials are all down more than 2%. Stocks started to roll over aggressively around 12:05 pm. The catalyst remains unclear (still looking). Earlier this morning, Iran officially closed the Strait of Hormuz, with officials citing "We won't allow oil to leave the region."

ASX 200 intraday chart (Source: TradingView)

BHP largely insulated from Middle East conflict

[12:26 pm] BHP Chairman Ross McEwan says the company's Asia-focused supply chain limits its direct exposure to the US-Iran conflict, while flagging continued growth appetite.

Around 95% of BHP's output is directed to Asia, where trade routes remain open, limiting the direct impact of Middle East disruptions on the business

McEwan acknowledged some exposure to certain Middle Eastern passages but said the company's response would be reactive given limited ability to influence outcomes

Growth opportunities flagged in Argentina, Canada and Australia, with McEwan indicating BHP would pursue acquisitions if they stack up for shareholders

Source: Bloomberg

RBA flags March rate rise possible

[12:25 pm] Governor Michele Bullock has warned markets not to assume the RBA will wait for Q1 inflation data before acting, flagging March as a "live meeting."

Bullock cautioned that inflation expectations could become unanchored given supply shock risks from the Middle East conflict and already elevated inflation

Headline inflation sits at 3.8% with unemployment at 4.1%, which the Governor described as "tight" conditions warranting close monitoring

The RBA board may act before the Q1 CPI print due 29 April, pushing back against market assumptions that May was the earliest possible move

A rate decision at the March meeting remains on the table if the board determines it needs to move more quickly to anchor expectations

Source: Reuters

Lindian acquires rare earths processing facility

[11:35 am] Lindian has secured a binding deal this morning to acquire a fully built rare earths processing facility in Kazakhstan at a fraction of replacement cost, enabling a step-change from concentrate-only production to higher-value mixed rare earths carbonate output.

The stock opened 3.7% higher, now up a massive 30.1% ($0.69) to fresh all-time highs. Lindian shares are up 65% year-to-date and up 626% in the last twelve months.

Lindian will hold 51% of a joint venture acquiring 100% of the SARECO MREC hydrometallurgical plant for a total purchase price of US$15m

The majority of payment deferred until after commercial MREC production commences

Replacement cost of a new comparable facility is estimated at over US$500m, implying the acquisition is being made at roughly 3 cents in the dollar

The facility will process ~12,500 tonnes per annum of monazite concentrate from Lindian's Kangankunde project in Stage 1, with world-class recovery rates of 92% TREO and ~97% NdPr; a 10kg sample from Kangankunde has already been successfully processed at the plant

Both Kangankunde and the SARECO facility are targeted to be fully operational within approximately nine months (Q4 2026)

Company page: Lindian Resources (LIN)

Tech stocks reverse into negative territory

[11:30 am] The S&P/ASX 200 Tech Index opened 2.3% higher but has been aggressively sold down, now trading 0.8% lower. This price action is relatively consistent across the board, with Wisetech opening 2.6% higher, now down 0.3%. Most names follow the same gap-up-and-fade-like price action.

Ticker | Company | % Chg | Price |

|---|---|---|---|

WBT | Weebit Nano | -8.32% | $4.30 |

360 | Life360 | -5.95% | $23.25 |

CAT | Catapult Sports | -5.67% | $3.33 |

DDR | Dicker Data | -5.47% | $9.34 |

AD8 | Audinate Group | -3.40% | $2.84 |

ELS | Elsight. | -1.75% | $5.05 |

CDA | Codan | -1.75% | $36.48 |

SDR | Siteminder | -1.36% | $3.28 |

PPS | Praemium | -1.33% | $0.74 |

IRE | Iress | -1.23% | $7.21 |

MP1 | Megaport | -1.08% | $8.22 |

XRO | Xero | -1.08% | $79.11 |

BVS | Bravura Solutions | -0.98% | $2.02 |

MAQ | Macquarie Technology Group | -0.81% | $61.48 |

HSN | Hansen Technologies | -0.77% | $5.13 |

WTC | Wisetech Global | -0.24% | $45.18 |

NXL | Nuix | -0.16% | $1.83 |

TNE | Technology One | 0.16% | $25.00 |

OCL | Objective Corporation | 0.31% | $12.82 |

DTL | Data#3 | 0.52% | $6.81 |

NXT | NextDC | 1.72% | $13.58 |

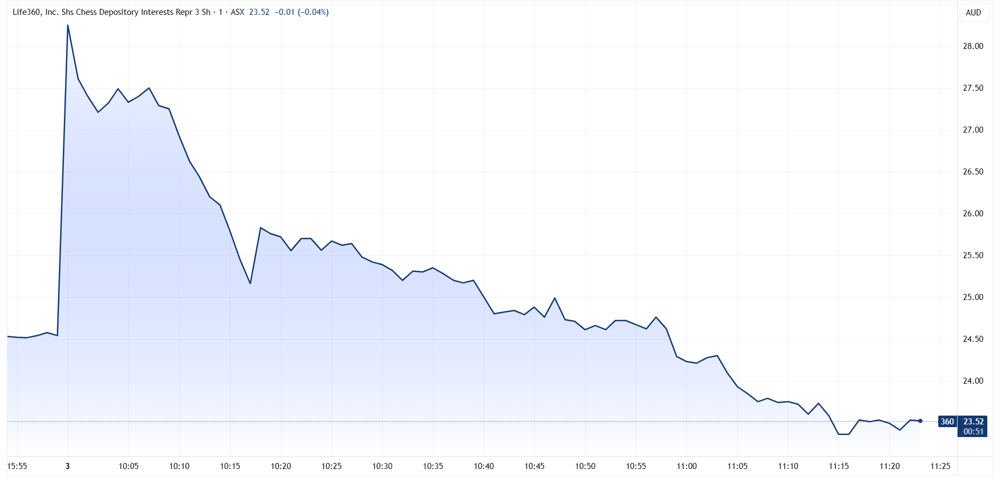

Life360 gaps 13%, now red

[11:25 am] Massive reversal for Life360, with the stock opening 13.1% higher, but aggressively sold down, now down 6.0% (if you bought the top, you'd be down ~18%).

The company's 4Q25 result was broadly ahead of market expectations, though the FY26 guidance was relatively in-line, with management flagging a heavily weighted second half.

Revenue up 26% to $146.0m vs. $141.1m ests (3% beat)

Adjusted EBITDA up 53% to $32.4m vs. $26.8m ests (21% beat)

Global MAUs up 20% to 95.8m, in line with January guidance and above 95.1m ests (0.7% beat)

FY26 revenue guidance of $640-$680m (midpoint $660m) vs. $653.7m ests, with adjusted EBITDA guided to $128-$138m (midpoint $133m) vs. $132.8m ests

Management flagged earnings will be heavily second-half weighted

Life360 intraday chart (Source: TradingView)

Gold stocks broadly lower

[11:20 am] Gold stocks are trading 1-4% lower despite gold prices running for five straight sessions, up 4.1%. Prices were rather volatile overnight, closing 0.8% higher, down from session highs of 2.6%. This intraday weakness might explain why gold miners are off to a weak start.

Ticker | Company | % Chg | Price |

|---|---|---|---|

EMR | Emerald Resources | -4.72% | $6.76 |

RMS | Ramelius Resources | -4.49% | $4.58 |

EVN | Evolution Mining | -4.13% | $16.94 |

NEM | Newmont Corp | -3.49% | $180.69 |

NST | Northern Star Resources | -3.37% | $30.66 |

ALK | Alkane Resources | -3.36% | $1.73 |

PRU | Perseus Mining | -3.11% | $6.09 |

CYL | Catalyst Metals | -2.75% | $8.49 |

PNR | Pantoro Gold | -2.21% | $5.76 |

RRL | Regis Resources | -1.84% | $9.58 |

VAU | Vault Minerals | -1.43% | $5.88 |

GMD | Genesis Minerals | -1.36% | $7.95 |

OBM | Ora Banda Mining | -1.29% | $1.37 |

CMM | Capricorn Metals | -1.29% | $15.33 |

WGX | Westgold Resources | -0.43% | $8.02 |

BGL | Bellevue Gold | -0.43% | $1.83 |

RSG | Resolute Mining | 2.26% | $1.68 |

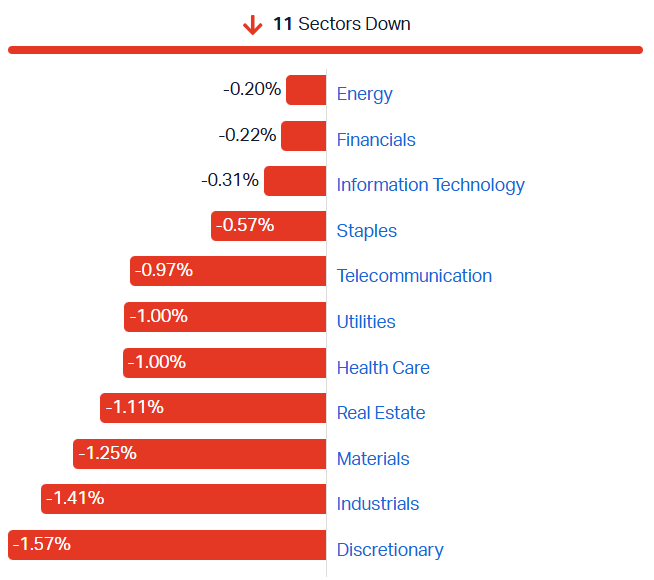

All sectors red, ASX 200 trending lower

[11:15 am] ASX 200 down 0.78%, current sitting at session lows. A relatively downbeat session, with all sectors trading lower and 158 constituents (79%) in the red. Despite a strong reversal on Monday (closed +0.03% higher, from session low of -0.86%), the market is cooling off after four-straight days of all-time highs.

ASX 200 sectors (Source: Market Index)

ASX 200 top gainer and losers

[11:00 am] Defence and energy stocks continued to trend higher, while gold, travel and growth stocks struggled for upside.

Ticker | Company | % Chg | Price |

|---|---|---|---|

IPX | Iperionx | 4.53% | $7.15 |

LNW | Light & Wonder | 4.05% | $129.91 |

NHC | New Hope Corporation | 4.00% | $4.94 |

WHC | Whitehaven Coal | 3.09% | $8.19 |

NXG | Nexgen Energy.s | 2.61% | $18.48 |

FBU | Fletcher Building | 2.58% | $2.99 |

VEA | Viva Energy Group | 2.46% | $1.88 |

YAL | Yancoal Australia | 2.34% | $6.34 |

XYZ | Block | 1.75% | $90.72 |

TLX | Telix Pharmaceuticals | 1.64% | $9.92 |

Ticker | Company | % Chg | Price |

|---|---|---|---|

CSC | Capstone Copper Corp | -5.46% | $13.68 |

PME | Pro Medicus | -5.33% | $118.93 |

ASB | Austal | -5.04% | $5.09 |

DOW | Downer | -4.52% | $8.24 |

RMS | Ramelius Resources | -4.49% | $4.58 |

EMR | Emerald Resources | -4.37% | $6.78 |

VGN | Virgin Australia | -4.27% | $3.14 |

EVN | Evolution Mining | -4.24% | $16.92 |

GGP | Greatland Resources | -4.08% | $13.86 |

DRO | Droneshield | -3.89% | $3.71 |

By Warren Masilamony

Magellan rallies on Barrenjoey merger

[10:26 am] MFG opened 17% higher is now up 27% at $10.75 in morning trade, its highest since September. Morgan Stanley upgraded MFG to Equal-weight, raised target from $8.35 to $9.20 after the company launched a $130m placement at $8.45 to help fund a larger stake in Barrenjoey ahead of the proposed merger.

Re-rating setup: Morgan Stanley frames the BJ merger as a “Macquarie like growth story” and explicitly flags a re-rating because the combined group offers better growth at a lower multiple versus peers.

Pro-forma multiple looks cheap versus comps: On BJ at 100%, the broker says the pro forma MFG valuation equates to about 10.4x LTM NPATA and 11.5x NPAT. It calls below comps and highlights BJ as nearly half of group earnings (47-48% of NPAT/NPATA).

Deal multiple supports valuation gap: Morgan Stanley implies MFG is paying ~15x LTM CY25 P E for BJ (ex synergies) versus ~20.5x for US mid cap advisory banks (CY25) and ~17x for US Aus large caps (CY25), arguing this underwrites “sound re rating prospects”.

By Warren Masilamony | Company page: Magellan Financial Group Ltd (MFG)

Coal stocks trading higher

[10:10 am] Newcastle coal futures jumped 7.7% to US$125.85 a tonne, helping lift coal producers 1-6% in early trade.

Ticker | Company | % Chg | Price |

|---|---|---|---|

YAL | Yancoal Australia. | 5.17% | $6.51 |

WHC | Whitehaven Coal | 4.66% | $8.31 |

NHC | New Hope Corporation | 4.42% | $4.96 |

SMR | Stanmore Resources | 1.41% | $2.88 |

By Warren Masilamony

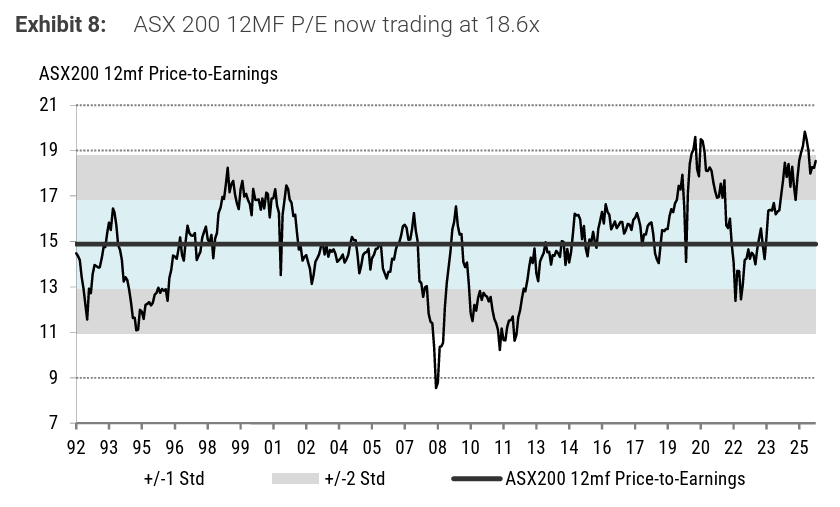

ASX 200 valuations near historic highs

[9:52 am] The ASX 200's twelve month forward price-to-earnings ratio now sits at 18.6x, not far from recent peaks of almost 21x.

Source: Morgan Stanley

I think comparisons vs. historical valuations are becoming increasingly irrelevant. If we look at BHP (largest weighting on the ASX) – the company has grown copper as a percentage of EBITDA from ~30% to over 50% in the last three years. BHP's 1H26 results presentation noted how the multiples of copper pure plays have increased from ~6.5x to 9.5x, while BHP was trading around 6x. The point is, as BHP becomes an increasingly copper-weighted play, it's not really logical to continue to reference historic valuations.

AREIT asset values stabilise but rate uncertainty delays re-rating

[9:36 am] Australian REITs are entering a new rate hike cycle with asset valuations in far better shape than 2022-23, but price-to-NTA multiples have pulled back and the path higher is likely bumpy. Morgan Stanley sees fund managers as the preferred way to play the theme.

For the first time in four years, the Feb-26 reporting season saw average upward revaluations across every asset class, demonstrating broad-based pricing stability after 50-140bps of cap rate expansion since June 2022

The sector has de-rated from 1.1x P/NTA in October 2025 to 0.9x currently, driven by the RBA's February rate hike and market expectations for at least one further 25bp hike by mid-2026

Downside risk to asset values is seen as minimal given the valuation correction already absorbed. Unlike the 2022-23 cycle, a resumption of the journey to above 1.0x P/NTA expected once the market gains confidence the hiking cycle is complete

Morgan Stanley's preferred exposure is via fund managers Charter Hall (Overweight, price target of $27.75) and Centuria Capital (Overweight, price target of $2.40), as any pick-up in transaction activity driven by rising property values should support earnings from FY27 onwards

Magellan-Barrenjoey merger sets up Macquarie-like re-rating opportunity

[9:25 am] Morgan Stanley sees the proposed merger of Magellan and Barrenjoey as a structural re-rating catalyst, with the combined group offering faster growth at a cheaper multiple than peers.

MFG is raising $150m to acquire an additional 10% of Barrenjoey ahead of a full merger, taking its stake to 36%

Pro-forma for 100% ownership, Barrenjoey represents 44% of group PBT and 47-48% of NPAT

The deal values Barrenjoey at $1.62bn on a 100% equity basis at 15x CY25 P/E ex-synergies, a discount to US midcap advisory peers at ~20.5x CY25 P/E

Pro-forma, MFG trades at 10.4x LTM NPATA and 11.5x NPAT, below comparable peers

Barrenjoey's CTI ratio (including bonuses) has compressed from 84% in FY25 to 72% in 1H26, with the compensation ratio holding steady at 52-53% and seen scaling toward MQG's low-40s% over time

Morgan Stanley estimates taking Barrenjoey to 100% ownership increases MFG's FY28 group NPAT growth by approximately 5%, with the merged group offering a growth profile at a lower multiple than peers

Company page: Magellan Financial Group (MFG)

Life360 beats on 4Q25 revenue and EBITDA, guides FY26 above consensus

[9:20 am] Life360 delivered a strong Q4, beating on key metrics and issued a relatively in-line FY26 guidance, underpinned by record subscriber additions and accelerating monetisation. Nasdaq-listed Life360 shares are currently up 13.3% to US$60.98.

Revenue up 26% to $146.0m vs. $141.1m ests (3% beat)

Adjusted EBITDA up 53% to $32.4m vs. $26.8m ests (21% beat)

Global MAUs up 20% to 95.8m, in line with January guidance and above 95.1m ests (0.7% beat)

Operating cash flow up 199% to $36.8m

FY26 revenue guidance of $640-$680m (midpoint $660m) vs. $653.7m ests, with adjusted EBITDA guided to $128-$138m (midpoint $133m) vs. $132.8m ests

Management flagged earnings will be heavily second-half weighted

FY26 outlook calls for revenue growth acceleration driven by both the core subscription business and the scaling of its advertising platform, with a longer-term target of above 35% adjusted EBITDA margin

Company page: Life360 (360)

Acadia's trofinetide receives negative EU opinion for Rett syndrome treatment

[9:16 am] Europe's medicines regulator has rejected Acadia's marketing application for trofinetide, its Rett syndrome treatment, despite the drug already being approved in three other markets.

The CHMP issued a negative opinion citing the treatment effect observed at 12 weeks as limited in magnitude, incomplete capture of core Rett syndrome symptoms, and longer-term outcome data compromised by patient discontinuations

Acadia intends to request a re-examination of the opinion, arguing the LAVENDER trial successfully met its co-primary and key secondary endpoints

Trofinetide remains the first and only approved treatment for Rett syndrome in the US, Canada and Israel, leaving EU patients without access pending any re-examination outcome

Rett syndrome affects approximately 1 in 10,000 to 15,000 female births globally and typically requires intensive round-the-clock care into adulthood, underlining the unmet need the drug targets

Nasdaq-listed Acadia dipped 7.1% overnight, which is not a good look for Neuren Pharmaceuticals.

For context, Neuren is essentially a royalty and milestone recipient, having developed trofinetide and licensed its commercalisation rights to Acadia .

Rio Tinto advances North American gallium supply chain with Canadian-backed pilot plant

[9:05 am] Rio Tinto is moving to extract primary gallium from its existing alumina refining operations in Quebec, backed by government funding, as part of a push to establish a critical minerals supply chain outside of China.

A pilot plant will be constructed at Complexe Jonquière in Saguenay, targeting operational status in 2027, following the first successful gallium extraction with partner Indium Corporation in May 2025

A demonstration plant with capacity of up to 4 tonnes of gallium per year is planned for the same site, with a path to commercial scale production of up to 40 tonnes annually or roughly 5% of current global output

The project has received a conditionally approved non-repayable contribution of up to C$18.95m from the Government of Canada, alongside C$7m previously committed by the Government of Quebec

All current global gallium production of more than 700 tonnes per year is sourced from outside North America, making this a strategically significant project for Western supply chain resilience given gallium's use in defence radar, semiconductors, EVs and consumer electronics

Company page: Rio Tinto (RIO)

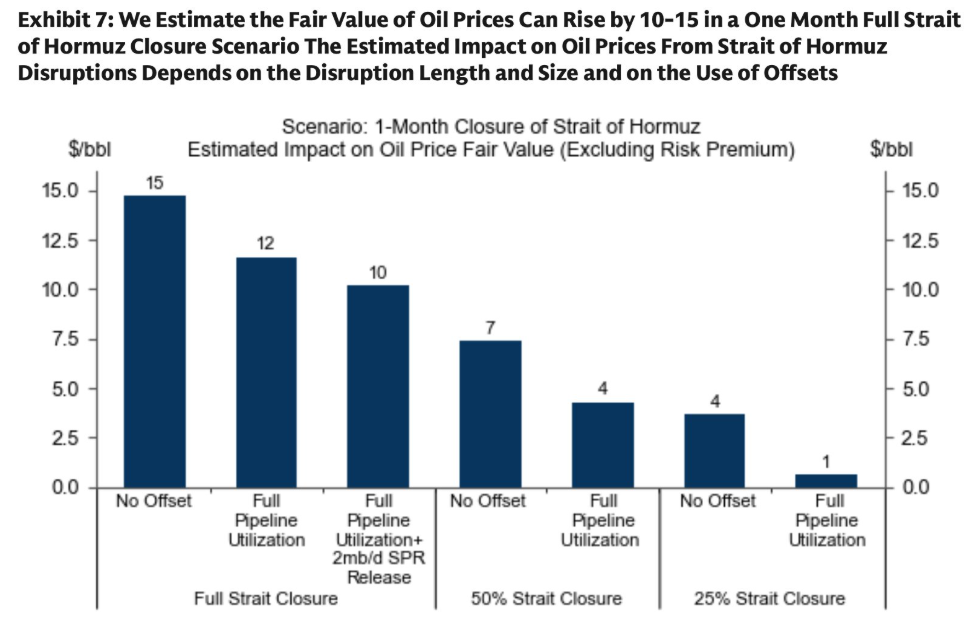

Goldman Sachs' oil price scenarios

[9:03 am] A Goldman Sachs chart maps out oil price scenarios under varying degrees of a Strait of Hormuz closure.

Source: Goldman Sachs

Trump outlines four objectives for Iran campaign

[9:00 am] Trump has defined the goals of the US military campaign against Iran for the first time, signalling a sustained operation with no firm end date as the conflict widens across the region.

Trump outlined four objectives: eliminating Iran's missile capabilities, destroying its navy, cutting off its path to a nuclear weapon, and ending its funding and direction of terrorist groups

Trump said the campaign could run "whatever it takes," extending beyond the initial four-to-five week projection, while Defence Secretary Hegseth pushed back on any fixed timeline

Four US service members have been killed so far. Trump has acknowledged more casualties are likely but has not ruled out sending ground troops, saying "I don't have the yips with respect to boots on the ground"

Iran has continued retaliatory strikes, launching waves of missiles at targets across multiple countries hosting US military facilities, blasts were reported Monday in Israel, Saudi Arabia, Qatar and the UAE

Source: Bloomberg

US-Israel strikes on Iran spark major energy market disruption

[8:57 am] Military strikes on Iran have triggered cascading damage across Middle East energy infrastructure, with the Strait of Hormuz effectively shut and a significant share of global LNG supply offline.

Brent and WTI crude jumped sharply on the Sunday open, while European gas prices surged more than 50% after Iranian drones targeted Qatar's Ras Laffan LNG facility, taking offline roughly a fifth of global LNG supply

Aramco's 550,000 bpd Ras Tanura refinery (one of the world's largest) halted operations after drone debris caused a fire, though Bloomberg says exports appear to be running normally

Strait of Hormuz vessel traffic has fallen to near zero, with at least 13 empty LNG tankers diverting away, Goldman Sachs estimates a month-long halt could push spot Asian LNG prices up 130% to $25/mmbtu

Additional infrastructure hit includes VTTI's Fujairah oil storage terminal (UAE), Kuwait's West Doha power and desalination plant, Jebel Ali container port, and an Amazon data centre in the UAE

OPEC+ announced a larger-than-expected output boost of 206,000 bpd on Sunday to help offset potential lost Iranian supply, though the move has done little to fully calm markets

Safe haven assets rallied with strength in gold, yen and Swiss franc, travel and leisure stocks sold off sharply, while Treasury yields edged higher as Fed rate cut expectations were trimmed on oil-linked inflation fears

Trump indicated the assault could be sustained for four to five weeks, while signalling openness to lifting sanctions if new Iranian leadership proves pragmatic

US manufacturing holds up but inflation alarm bells are ringing

[8:54 am] US manufacturing expanded for a second straight month in February, but a sharp surge in input prices is raising fresh inflation concerns, compounded by the outbreak of conflict in the Middle East.

ISM manufacturing index came in at 52.4 vs. 51.8 ests, down slightly from January's 52.6 reading

Prices paid index surged 11.5 points to 70.5, the highest level since June 2022, driven by metals costs and tariff-related price pressures across steel, aluminium, and raw materials

New orders eased 1.3 points to 55.8 and production fell 2.4 points to 53.5, though both remain in expansion territory; order backlogs jumped 5 points to 56.6, the highest since May 2022

Employment index edged up 0.7 points to 48.8 (still in contraction), though nearly one in five respondents reported higher headcount, the largest share since 2022

US and Israeli airstrikes on Iran over the weekend have since halted oil tanker traffic through the Strait of Hormuz and pushed crude prices sharply higher, meaning the prices index is likely to remain elevated or move higher in coming months

Markets shrug off Iran conflict

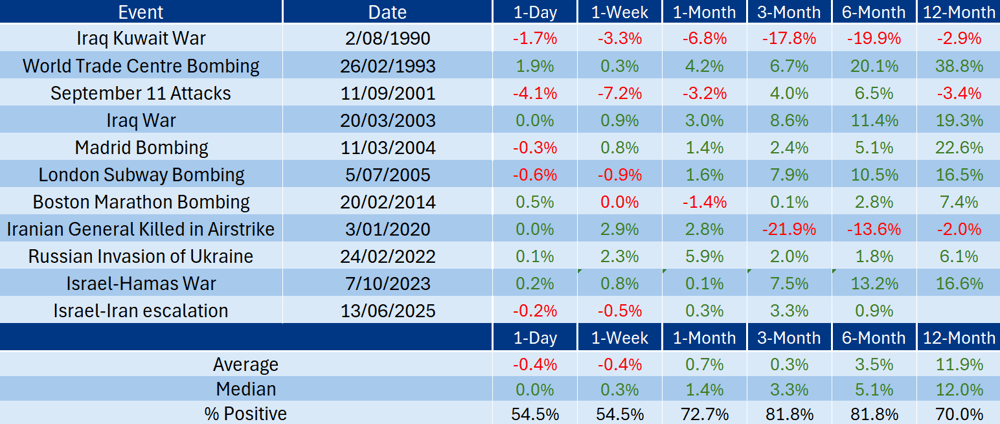

[8:50 am] Equity markets pretty much all reversed from session lows to close around breakeven. The S&P 500 dipped 1.19% in early trade, closed 0.04% higher, while the ASX 200 fell 0.86% on Monday but finished the session up 0.03%. This is despite Trump saying attacks will continue until US objectives are met.

While uncertainty about the path ahead remains high, markets have the tendency to look past geopolitical events. The below table shows how the S&P/ASX 200 (price not total returns) performs after major geopolitical events.

S&P/ASX 200 performance after major geopolitical events (Source: Kerry Sun)

Good morning!

[8:30 am] ASX 200 futures are down 27 pts (-0.29%) as of 8:30 am AEDT.

The overnight session in a nutshell:

Major US benchmarks mixed but bounced off worst levels

S&P 500 dipped as much as 1.19% in early trade, finished the session marginally positive

Volatile overnight session for commodities, most of which traded sharply higher on Monday morning but set to close the session off best levels

Markets shrugging off US/Israeli attacks on Iran, though ongoing strikes, jump in oil price and inflation concerns may continue to weigh on equities