ASX 200 Live Today - Tuesday, 19th May

The S&P/ASX 200 is set to bounce after suffering a sharp selloff on Monday and a strong overnight session for defensive sectors.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Tuesday, May 19. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

ASX 200 bounces from no man's land

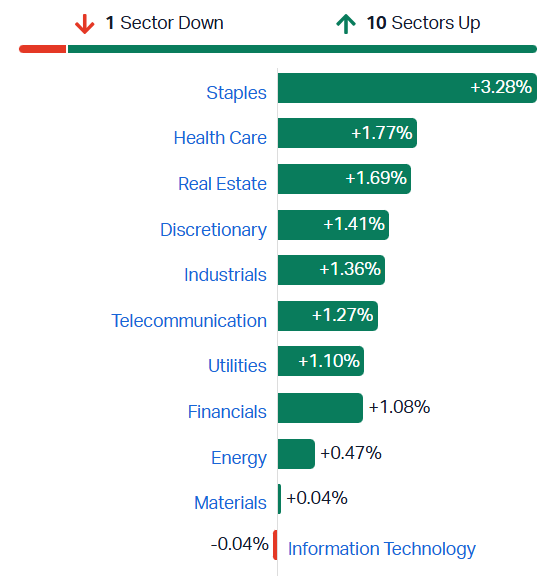

[2:10 pm] A decent bounce after a ~4.2% skid in the last seven sessions. The S&P/ASX 200 is up 1.03%, with 136 constituents higher (68%) and only Tech (-0.38%) and Materials (-0.91%) lower. This session features rather outsized bounces for sectors like:

Staples (+3.3%) after a 12% selloff between 22-Apr and 18-May

Telcos (+2.4%) has been trading mostly sideways this year, on track to close at the highest since December

Financials (+1.9%) now up ~3.6% in the last four sessions. This follows a sharp 8.3% dip between 6-13 May

Sectors like Real Estate, Discretionary, Healthcare and Industrials are also up 1-2%

A much-needed bounce from no man's land. The ASX 200 is trading firmly below its 200-day moving average, breadth is deteriorating, and bond yields have climbed to uncomfortable levels. The Aussie 10-year has pulled back slightly, down 2 bps to 5.04%, but yields in Japan, the UK, and the US continue to creep higher.

TechnologyOne 1H26 earnings call highlights

[2:00 pm] Here are some of the key takeaways from the TNE earnings call.

AI product adoption is tracking well above internal expectations, with customer feedback described as unprecedented and pointing to potential ARR upside

SaaS+ now underpins all offerings, simplifying implementations and lifting recurring revenue quality, with no separate segmentation disclosed given the integrated sales approach

FY26 guidance reaffirmed at 16-18% ARR growth and 18-20% PBT growth, targeting the top end of both ranges with PBT margin expansion to 32% and 100% cash conversion

Net revenue retention guided to 115-120% by FY26 year-end, supported by exponential AI uptake driving higher engagement and transaction volumes

UK and ANZ pipelines remain solid post-Showcase, though a stronger AUD vs. GBP and NZD is a known ARR headwind on statutory results

Company page: TechnologyOne (TNE)

Analysts' take on Brambles

[1:22 pm] Brambles downgraded its FY26 sales and underlying profit growth guidance on Monday, due to a ~$60 million earnings impact from US repair network disruptions, partially offset by a tightened FCF outlook and a new $400 million buyback.

Analysts were divided on whether the issues are temporary execution challenges or expose structural vulnerabilities in Brambles' reliance on third-party repair providers, with most lowering targets but maintaining constructive medium-term views. The stock fell 20.2% on the day.

UBS upgraded to Buy from Neutral, lowered target from $25.40 to $23.80. Viewed the ~20% share price reaction as overdone with valuation support re-emerging, and expects most of the $60M earnings impact to unwind over time through operational fixes and pricing pass-through.

JPMorgan retained Neutral, lowered target from $24.20 to $19.50. Viewed the disruption as operational rather than demand-driven with the $400m buyback and reaffirmed FY28 margin target supportive, though forecasts a material FY27 FCF decline from elevated pallet purchases and capex.

Morgans downgraded to Hold from Accumulate, lowered target from $25.50 to $18.70. Viewed management's remediation plan as credible but highlighted ongoing execution risk, while maintaining confidence in achieving the FY28 margin targets.

Top All Ords gainers and losers

[1:18 pm] Here are the top S&P/All Ordinaries movers for the session.

Ticker | Company | % Chg | Price |

|---|---|---|---|

TUA | Tuas | 22.03% | $2.77 |

CAY | Canyon Resources | 7.41% | $0.15 |

OBM | Ora Banda Mining | 6.94% | $1.42 |

GTK | Gentrack Group | 6.93% | $3.55 |

STN | Saturn Metals | 6.25% | $0.51 |

TYR | Tyro Payments | 5.87% | $0.76 |

BLX | Beacon Lighting Group | 5.83% | $1.64 |

GNP | Genusplus Group | 5.64% | $9.74 |

SPL | Starpharma | 5.45% | $0.58 |

SMR | Stanmore Resources | 5.30% | $2.49 |

Ticker | Company | % Chg | Price |

|---|---|---|---|

AFP | Aft Pharmaceuticals | -13.33% | $2.73 |

BTL | Beetaloo Energy Australia | -7.02% | $0.27 |

WHI | Whitefield Income | -6.99% | $1.27 |

WA1 | WA1 Resources | -6.76% | $13.66 |

BCN | Beacon Minerals | -6.74% | $2.63 |

29M | 29Metals | -6.67% | $0.25 |

PDI | Predictive Discovery | -6.63% | $0.85 |

SRL | Sunrise Energy Metals | -6.39% | $12.23 |

GLN | Galan Lithium | -6.29% | $0.42 |

FRS | Forrestania Resources | -6.25% | $0.60 |

China aluminium smelters maxing out as inventories pile up

[1:16 pm] China's aluminium smelters are running at record rates, capturing peak margins amid the Iran-driven supply shock, but domestic inventory builds are starting to flash warning signs.

Daily output hit an all-time high of 129,000 tons in April, with Jan-April production up 3.5% to 15.33Mt

Producers pushing plants ~3% above nameplate via tech upgrades, bumping against the 45Mt annual capacity ceiling imposed in 2017

Citigroup expects further price upside as the market deals with its biggest supply shock in 50 years

Domestic inventories have more than doubled YTD to 1.37Mt, a 6-year high, as exports fail to fully offset weak domestic demand

Chinese aluminium demand growth tracking just ~1% this year, briefly turning negative in Jan-Feb, raising concerns about overproduction

Profitability may have already peaked despite record April margins

Source: Bloomberg

Korea's Kospi rally showing signs of froth despite chip-led record run

[1:14 pm] The Kospi is up 75% YTD but the rally is narrowing sharply, with Samsung and SK Hynix accounting for two-thirds of gains and a ~5% Tuesday tumble highlights an increasingly fragile market.

Just 33% of Kospi constituents trade above their 50-day average, down from 70% three weeks ago; only 2% hitting fresh 52-week highs despite the index at successive records

Non-tech firms have driven just 4% of the 12-month earnings gain since September, according to BNP Paribas

Tech valuations remain reasonable but other hot sectors are stretched, with materials (including EV names) at ~60x forward earnings

Retail margin debt hit a record 36.5 trillion won (US$24.4bn), raising forced unwind risk

Source: Bloomberg

Analysts' take on Elders

[12:07 pm] Elders reported a disappointing 1H26 on Monday, with elevated corporate services costs from systems modernisation weighing on profitability despite strong operational performance in crop protection and rural services.

Analysts responded somewhat positively despite the miss, generally lowering price targets but maintaining or upgrading ratings, arguing the market overreacted by treating transformation costs as permanent rather than temporary, with material cost relief expected in H2 and into FY27. Shares fell 22.9% on the day.

Morgans retained Buy, lowered target from $8.65 to $7.90. Delta Agribusiness contribution was below expectations but the synergy programme remains on track, with undemanding trading multiples and an attractive fully franked dividend yield supporting the valuation case.

Bell Potter retained Buy, lowered target from $9.00 to $6.45. Revenue outperformance in crop protection and rural services was realised from price tailwinds, but flagged earnings downside risk if the elevated cost base persists given dual running of legacy and new platforms.

Macquarie retained Outperform, lowered target from $8.50 to $7.50. The agency business was the standout performer with gross margin improvement from higher livestock prices, with systems modernisation spend set to reduce progressively and a clear pathway back to the management leverage target range.

Chinese lithium futures lower

[12:05 pm] Chinese lithium futures notably lower in early trade, down 4.3% to 183,140 yuan a tonne.

While most lithium stocks experienced a flattish open, bellwether names like PLS Group and Liontown are now down 3-4%.

Ticker | Company | % Chg | Price |

|---|---|---|---|

PAT | Patriot Resources | -4.55% | $0.11 |

LTR | Liontown | -4.53% | $2.22 |

AGY | Argosy Minerals | -4.41% | $0.07 |

VUL | Vulcan Energy Resources | -4.37% | $3.40 |

PLS | PLS Group | -3.08% | $5.82 |

IGO | IGO | -2.99% | $8.11 |

INR | Ioneer | -2.00% | $0.15 |

CXO | Core Lithium | -0.94% | $0.32 |

PMT | Pmet Resources | 0.00% | $0.66 |

DLI | Delta Lithium | 0.00% | $0.21 |

MIN | Mineral Resources | 0.31% | $64.30 |

EUR | European Lithium. | 0.48% | $0.42 |

WR1 | Winsome Resources | 0.94% | $0.54 |

GL1 | Global Lithium Resources | 4.17% | $0.50 |

Analysts' take on Ora Banda

[11:32 am] OBM formally sanctioned a new 3.0Mtpa Davyhurst processing plant alongside Waihi underground approval on Monday, unveiling its 'Drive to 300' aspiration targeting ~300kozpa by FY29.

Analysts were broadly positive, viewing the decision to retain the existing mill (lifting combined capacity to ~4.2Mtpa) as the key upside surprise, though FY27/FY28 were flagged as transition years with negative FCF through the peak capex period. Shares rallied 3.6% on the day.

UBS upgraded to Buy from Neutral, raised target from $1.40 to $1.60. Update came with greater scale than anticipated, with the retained mill the key upside surprise and the company expected to remain FCF positive through the build despite heavier capex.

Euroz Hartleys retained Buy, raised target from $1.92 to $2.05. Board approval effectively green-lights the FY29 earnings step-change, with conservative reserve pricing, Waihi underground additions and a self-funded growth profile viewed as compelling differentiators.

Australian consumer sentiment ticks up but housing views deteriorate sharply

[10:46 am] Westpac-MI consumer sentiment improved modestly in May but remains deeply pessimistic, with housing-related indicators weakening notably ahead of the June RBA meeting.

Headline sentiment index up 3.5% to 83 in May (from 80.1), with fuel excise tax halving driving ~30c/litre pump price relief, partly offset by the RBA's third consecutive 25 bp hike

Federal budget reception poor: 34% expect to be worse off vs 15% better off (21% gap, well wider than last year's 10% gap and 2024's 3% gap when stage 3 tax cuts featured)

Inter-generational themes stark with Boomers/Gen X gap at 30-36% worse off vs Millennials at 9% and Gen Z slightly net positive

Mortgage rate expectations index up 2.3% to 181.2 (fresh 3-year high), with 85% of consumers (closer to 90% for mortgage holders) still expecting further hikes despite three already this year

Housing sentiment under pressure as 'time to buy a dwelling' index down 16.1% to 72 (18-month low, ~50pts below long-run average)

House price expectations off 1.8% to 150.6, now 13.4% below February high but still 20pts above long-run average

Unemployment expectations index down 5.2% to 140, clawing back half of last month's rise but still above long-run average of 129

Source: Westpac

China BEV sales rebound in April, lithium market stays tight

[10:24 am] Morgan Stanley's China autos team flags improving BEV demand and a still-tight lithium market, with spodumene prices well above incentive levels.

China BEV sales up 9% MoM and 10% YoY in April, with YTD tracking +2.6% YoY

Demand supported by new launches, promotions and seasonal recovery, with MS expecting further improvement into H2, though broad model choice and subdued consumer confidence may reinforce a "wait-and-see" mindset

China BEV exports up 85% YoY and 20% MoM, helping offset softer domestic demand

Lithium market remains tight despite some Zimbabwe lithium concentrate export resumption (subject to quotas and local processing requirements)

Spot spodumene ~US$2,860/t, well above MS long-term real US$1,510/t, which could encourage restarts

ASX 200 opens higher, defensives bounce

[10:20 am] A fairly strong open, with the ASX 200 up 1.0% and pretty much all sectors positive outside of Tech and Miners. Though the index is still down 0.4% for the week, after Monday's 1.45% selloff. A clear bid for defensive pockets of the market, with Staples, Healthcare and Real Estate trading notably higher. The market has had the tendency to fade strong opens, so let's see how the dust settles.

S&P/ASX 200 sectors (Source: Market Index)

Japan Q1 GDP beats expectations on consumption and trade strength

[10:14 am] Japan's economy grew faster than forecast in Q1, supporting the BoJ's policy normalisation case, though the outlook remains clouded by the Iran war.

Q1 Real GDP up 2.1% annualised vs 1.7% ests, accelerating from a downwardly revised 0.8% in Q4

Private consumption (>50% of GDP) up 0.3% QoQ vs 0.1% ests, supported by utility subsidies and wage growth finally outpacing inflation

Net exports also contributed more than expected, with March data showing faster export growth as China demand rebounded

Business investment growth slowed to 0.3% QoQ, though Finance Ministry corporate survey showed a fifth consecutive quarterly rise in ordinary profits, with AI boom and digitalisation demand supporting capex

Solid print gives the BoJ scope to argue the economy can withstand higher rates as it addresses upward inflation risks

Source: Bloomberg

Top ASX 200 gainers

[10:10 am] Tuas bounces after experiencing a ~50% selloff on Monday, Ora Banda trending higher as yesterday's ore reserves update validates the company's growth pathway and Stanmore likely benefiting off the Anglo American coal asset divestment.

Ticker | Company | % Chg | Price |

|---|---|---|---|

TUA | Tuas | 18.72% | $2.70 |

OBM | Ora Banda Mining | 9.43% | $1.45 |

SMR | Stanmore Resources | 7.20% | $2.53 |

4DX | 4DMedical | 5.50% | $4.22 |

PME | Pro Medicus | 5.24% | $132.10 |

ALK | Alkane Resources | 4.76% | $1.54 |

JHX | James Hardie | 4.65% | $27.23 |

WOW | Woolworths Group | 4.41% | $34.44 |

ALQ | ALS | 4.03% | $22.71 |

AUB | Aub Group | 3.86% | $25.02 |

Top ASX 200 losers

[10:10 am] Lynas pulling back after a 5.4% rally on Monday, TechnologyOne whipsaws on a mixed 1H26 result and lithium stocks broadly lower in early trade.

Ticker | Company | % Chg | Price |

|---|---|---|---|

LYC | Lynas Rare Earths | -3.86% | $18.20 |

TNE | Technology One | -2.76% | $27.85 |

DRO | Droneshield | -2.40% | $3.06 |

LTR | Liontown | -2.16% | $2.27 |

GQG | GQG Partners | -1.58% | $1.56 |

L1G | L1 Group | -1.36% | $1.09 |

PLS | PLS Group | -1.33% | $5.92 |

VUL | Vulcan Energy Resources | -1.27% | $3.51 |

CEN | Contact Energy | -0.74% | $8.05 |

IGO | IGO | -0.72% | $8.30 |

A volatile open for TechnologyOne

[10:06 am] TechnologyOne opened the session up 1.9%, now down 4.2%. The company reported its 1H26 result this morning, with most metrics tracking in-line with prior guidance (but maybe not enough to fend off ongoing software sector concerns).

ARR up 17% to $598.0m, within FY26 guidance range of 16-18%

Revenue up 11% to $322.7m vs $330.9m ests (2% miss)

NPAT up 6% to $66.8m vs $67.1m ests (in line)

PBT up 9% to $89.1m, in line with profit phasing flagged at AGM due to planned Showcase event investment

On constant currency and normalised basis, ARR up 19% and PBT up 21% with margin up 2pts to 30%

Interim DPS up 21% to 8 cps

FY26 guidance reaffirmed: PBT growth of 18-20% year-on-year (targeting top end), ARR growth of 16-18% (targeting top end), PBT margin expansion of 2pts to 32%, fully inclusive of AI, Showcase and SaaS+ investments

Market breadth continues to deteriorate

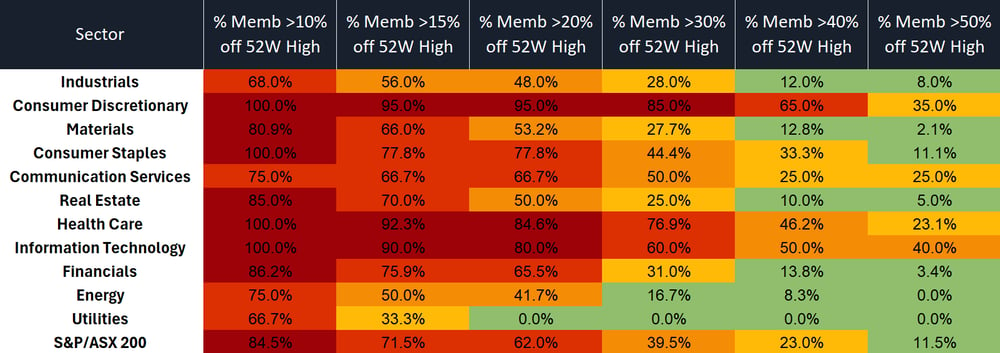

[9:43 am] I ran some numbers before market close on Monday, observing which ASX 200 stocks and sectors were trading furthest from their 52-week highs.

It's pretty rough out there, with 62% of S&P/ASX 200 constituents trading more than 20% below their 52-week highs. The pain is more pronounced in consumer facing and yield sensitive sectors like Discretionary, Healthcare, Staples and Tech.

Source: Market Index

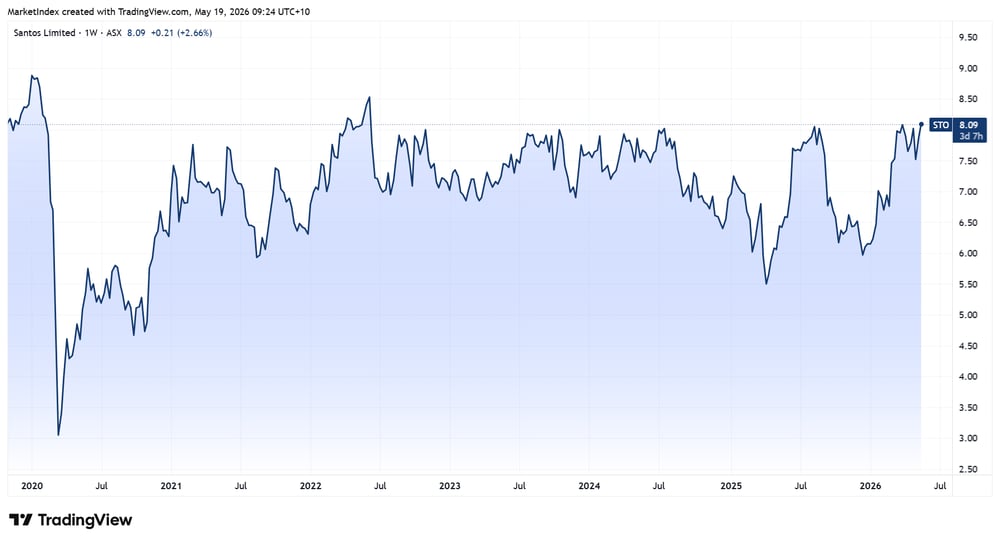

Santos: Another crack at $8

[9:38 am] Santos has made roughly a dozen attempts at breaking through the $8 level over the past four years. After an ~8% pullback in recent weeks, the stock has returned to this key inflection point.

Santos price chart (Source: TradingView)

Catalyst Metals flags low-cost path to expand Plutonic mill throughput

[9:21 am] Catalyst has completed a study on refurbishing its mothballed PP2 circuit at Plutonic, offering low capital-intensity throughput expansion optionality on top of its existing 200,000/oz per annum plan.

Study contemplates lifting Plutonium's processing capacity from 2.0Mtpa to between 2.5Mtpa and 3.0Mtpa, at a capital cost of $50-75m

Two options assessed: standalone refurbished PP2 (0.5-0.7Mtpa throughput) or utilising upgraded PP1 crushing circuit to feed both PP1 and PP2 mills (0.6-0.9Mtpa)

Low capex reflects leveraging existing infrastructure as PP2 (originally commissioned 1996, on care and maintenance since 2008) found to have most major mechanical assets in reasonable condition

Three of four new mines required for the ~200koz pa plan have been delivered in the past 12 months

No decision made on expansion, dependent on ongoing exploration success across the Plutonic Belt

Company page: Catalyst Metals (CYL)

Technology One delivers record H1, reaffirms upgraded FY26 guidance

[9:14 am] Technology One posted its 17th consecutive record first half profit and annual recurring revenue, with SaaS+ and AI momentum driving the result.

ARR up 17% to $598.0m, within FY26 guidance range of 16-18%

Revenue up 11% to $322.7m vs $330.9m ests (2% miss)

NPAT up 6% to $66.8m vs $67.1m ests (in line)

PBT up 9% to $89.1m, in line with profit phasing flagged at AGM due to planned Showcase event investment

On constant currency and normalised basis, ARR up 19% and PBT up 21% with margin up 2pts to 30%

Interim DPS up 21% to 8 cps

Rule of 40 result of 55%, placing TNE in the top quartile of global SaaS peers

FY26 guidance reaffirmed: PBT growth of 18-20% year-on-year (targeting top end), ARR growth of 16-18% (targeting top end), PBT margin expansion of 2pts to 32%, fully inclusive of AI, Showcase and SaaS+ investments

Company page: Technology One (TNE)

Bellevue Gold mines first ore from Deacon North on schedule

[9:09 am] Bellevue Gold has delivered first development ore from its high-grade Deacon North area on schedule, with grade control drilling results tracking expectations.

First development ore mined in May 2026, in line with company budgets and guidance

All major mining areas (Deacon Main, Viago, Deacon North) now in production, with combined output expected to support stable production for FY27 and beyond

Average development grade across first 13 production faces tracking better than initially anticipated, with main orebody structure aligned with geological expectations

FY27 guidance to be provided early in FY27, sixth underground diamond rig due on site in June quarter for FY27 exploration drilling

Company page: Bellevue Gold (BGL)

Victorian auditor-general to probe Lottery Corp's 40-year licence extension

[9:05 am] Victoria's auditor-general will investigate whether the Allan government's $1.15 billion, 40-year extension of The Lottery Corporation's exclusive licence delivered value for taxpayers, according to the AFR.

Deal extends TLC's exclusive Victorian public lottery licence by 40 years to June 30, 2068, four times the typical 10-year term, replacing the existing licence due to expire June 30, 2028

$1.15bn premium payment split into two instalments: $250m on July 3, 2026 and $895m on October 1, 2026

No public tender held and no other operators invited to bid, awarded via exclusive bilateral negotiations following a market sounding process started in June 2024

Victoria expects $642m in public lottery tax revenue next financial year, growing to $756m over the forward estimates, underscoring reliance on gaming taxes

Source: AFR

Mineral Resources restarts Bald Hill lithium mine on price recovery

[9:03 am] MinRes is restarting its 100%-owned Bald Hill lithium operation in WA, citing a sustained lithium price recovery, after placing it on care and maintenance in November 2024.

Production capacity of ~165,000 dmtpa of 5.1% spodumene concentrate, drawing on a 58.1Mt at 0.94% Li2O Mineral Resource

Ramp-up begins late May, crushing and mining in June, first spodumene production from July

First shipment from Port of Esperance expected Q1 FY27, ramp to full capacity in Q2 FY27

Restart costs of ~$20m (including working capital) to be incurred in Q4 FY26

Restart to create ~370 jobs, with ~110 redeployed from other MinRes operations

Company page: Mineral Resources (MIN)

Anglo American to sell Australian steelmaking coal mines to Dhilmar for up to $3.8bn

[8:52 am] Anglo American has agreed to divest its Australian steelmaking coal portfolio to Dhilmar Limited, with proceeds earmarked for debt reduction.

Total cash consideration of up to $3.875bn, comprising $2.3bn upfront at completion and a price-linked earnout of up to $1.575bn

Proceeds to be used to reduce net debt

Anglo continues to pursue arbitration with Peabody over its November 2024 agreement to acquire the same portfolio, maintaining the Moranbah North incident did not constitute a Material Adverse Change

Motorcycle Holdings COO buys 850k shares

[8:49 am] Motorcycle COO Michael Poynton acquired ~850k shares, lifting his beneficial ownership by 48.6% to 2.6 million shares.

MTO shares have tumbled 25% year-to-date and down 8% in the last twelve months.

Company page: Motorcycle Holdings (MTO)

Market tidbits: Breadth, concentration and a momentum unwind

[8:45 am] Here's a grab bag of interesting stuff that's crossed my desk this morning.

Breadth unusually narrow: Goldman notes that as the S&P 500 hit 14 new record highs over the past month, while the share of constituents above their 200-day moving average has fallen, with the median stock now 13% below its 52-week high. Sharp breadth drops have historically preceded larger drawdowns, though GS says today is nowhere near as extreme as 1999-2000 and comparable to May 2023, which saw volatility but not a bull market end.

Index concentration at all-time highs: Top 10 S&P 500 names now make up 41% of the index. CitiSec says passive flows are no longer neutral, with ~35c of every dollar into SPX going to the Mag 7, ~41c to the top 10, and nearly half into AI-linked exposure, effectively making passive buying a pro-growth, pro-momentum allocation.

Overbought reversal flashing caution: BTIG's Krinsky flags S&P 500 hit a daily RSI of 78 Thursday before dropping 1.2% Friday. Since 2003, there have only been six prior instances of a >1% drop after >RSI 75. Average returns were negative across all 5-40 day windows, with five of six seeing peak-to-trough drawdowns of at least 7%.

Momentum factor getting smoked: Goldman Sachs says momentum just had its worst two-day selloff since 2022, with back-to-back >5% unwinds as past losers outperform winners. The AI trade is taking collateral damage. GS sees the AI narrative as intact but flags stretched positioning (81st percentile 1yr, 96th percentile 5yr) and prefers buying the losers, since the short leg historically outperforms during 5%+ momentum drawdowns.

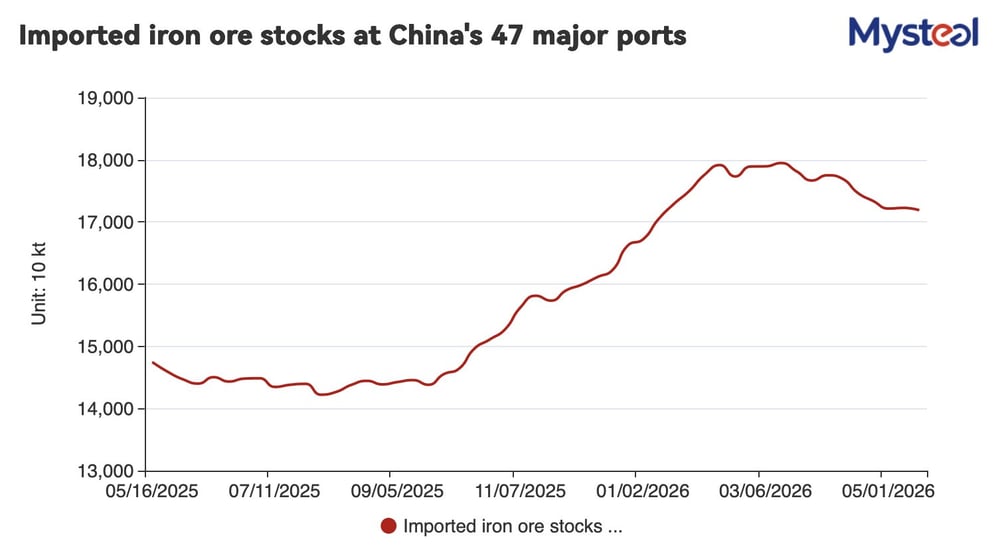

China port iron ore stocks edge lower as mill demand firms

[8:41 am] China's portside iron ore inventories slipped marginally last week, though levels remain well above year-ago, with rising mill offtake and growing port congestion the key signals.

Inventories at 47 tracked ports down 0.2% week-on-week to 171.89Mt as of May 14, but still 16.6% above year-ago levels

New iron ore arrivals down 6.6% week-on-week to 24.1Mt over May 4-10

Port congestion building, with 109 vessels queuing for unloading

Daily outflows up 4.6% to 3.37Mt/day

Source: Mysteel

Goldman sees central bank gold buying to accelerate in 2026

[8:37 am] Goldman expects official sector demand to drive a gold recovery by year-end, despite near-term pressure from sticky inflation and the bond selloff.

Central bank purchases forecast to average 60 tons/month over 2026, vs a revised 50-ton 12-month average to March (prior figure was 29 tons)

Goldman maintains US$5,400/oz year-end target, in line with recent UBS and ANZ calls

WGC estimated Q1 official sector buying at 244 tons, up from 208 tons in Q4

PBoC added 260koz in April, the most in over a year and an 18th consecutive month of buying

Near-term caution: Gold remains a natural source of liquidity if equities sell off on higher rates and weaker growth

Source: Bloomberg

Morgan Stanley flags equity correction risk from bond selloff

[8:36 am] Mike Wilson's team warns rising long-end yields could end the AI-led rally, though stays structurally bullish on a broadening earnings recovery.

First meaningful equity correction since March lows seen as likely if bond volatility persists and long-end rates keep climbing

US 30-year yield near 3-year highs, Japan yields at multi-decade highs, with S&P 500 equity risk premium shrinking toward zero

Morgan Stanley maintains 12-month S&P 500 target of 8,300 on the strongest earnings growth in 20+ years outside major-shock recoveries

Earnings strength extends well beyond AI beneficiaries, but investor positioning hasn't caught up to the broadening trade

Key catalysts to unlock the rotation: Oil prices and rates coming off recent highs, which in turn need a lasting Iran resolution

Source: Bloomberg

China April data misses across the board as Iran war bites

[8:35 am] China's recovery stumbled in April with consumption, output and investment all undershooting expectations as Middle East fallout weighs on the world's second-largest economy.

Retail sales up 0.2% vs 2% ests (weakest since Dec 2022, slowing from 1.7% in March)

Industrial output up 4.1% vs 5.9% ests (decelerating from 5.7% in March)

Urban fixed asset investment down 1.6% YTD vs +1.6% ests, with property investment plunging 13.7% (deepening from -11.2% in Q1)

Exports the bright spot at +14.1% vs 7.9% ests as foreign buyers stockpiled ahead of war-driven input cost rises

Factory-gate prices snapped a years-long deflationary streak to hit a 3-year high, with PPI outpacing CPI for the first time since July 2022

Iran oil export bottleneck deepens under US blockade

[8:34 am] Satellite imagery shows tanker congestion around Iran's main oil hub at multi-month highs as the US Navy blockade chokes exports.

23 tankers spotted around Kharg Island on May 16, vs just 4 on April 13 before the blockade began, with crude-loading berths sitting empty

US Central Command has turned around 81 commercial vessels and disabled 4 ships since the blockade began

Storage at Kharg is filling up, forcing Iran to slow crude production as laden tankers can't rotate out

Source: Bloomberg

Trump pauses Iran strike as Gulf allies push for diplomacy

[8:33 am] Trump called off a planned Tuesday strike on Iran after Saudi Arabia, Qatar and UAE requested a short delay to pursue a deal, though both sides remain far apart.

Trump said Gulf allies asked for 2-3 days as they believe a deal is close, with no deadline set for renewed military action

White House rejected Iran's Sunday proposal (delivered via Pakistani mediators) as lacking detail on uranium stockpile surrender and enrichment suspension; Iran says US demands remain excessive and wants frozen assets returned plus war compensation

Treasury extended Russian oil sanctions waiver another 30 days to ease global supply pressure

Trump also flagged potentially lifting sanctions on Chinese firms buying Iranian crude (China was ~90% of Iran's pre-war exports)

Source: Bloomberg

US equities lower as Iran tensions and AI unwind weigh

[8:27 am] Major US benchmarks finished mostly lower overnight but off worst levels.

Equal-weight S&P 500 (+0.62%) outperformed cap-weighted index by 69 bps, with majority of sectors higher

Outperformers included software, energy, banks, insurers, homebuilders and industrials, while laggards spanned tech hardware, autos, biotech, metals and quantum computing

US-Iran headlines drove volatility, with Trump cancelling a planned military strike on Iran following requests from Qatar, UAE, Saudi Arabia

Yields little changed after breaking out last Friday, US 10-year yield briefly hit 4.60% but finished the session slightly lower at 4.58%

Bearish narrative drivers include soaring global bond yields (Japan, UK in focus), energy inventory concerns, extended positioning, likely CTA selling and a hawkish Fed (market pricing ~15 bp of hikes through year-end)

Good morning!

[8:20 am] ASX 200 futures are up 92 pts (+1.07%).

The overnight session in a nutshell:

US benchmarks finished mixed: S&P 500 flat (-0.07%), Nasdaq -0.51% on a memory chip and semi-led tech pullback, Dow +0.32% as defensives outperformed

Bonds yields in focus, with the US 10-year yield briefly pushing above 4.60% to a one-year high and Morgan Stanley's Mike Wilson warning the AI-led rally is at risk from the global bond rout

Trump called off a planned US strike on Iran scheduled for Tuesday after appeals from the Saudi, Qatari and UAE leaders, citing "serious negotiations" toward a no-nuclear-weapons deal