ASX 200 Live Today - Tuesday, 17th March

The S&P/ASX 200 has given back early gains, now trading around breakeven ahead of the RBA decision. Here are today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Tuesday, March 17. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

ASX 200 edges higher

[2:40 pm] The ASX 200 was up about 0.18% heading into the RBA decision, briefly spiked to ~0.40% on the announcement, then settled right back to ~0.18%. Across other asset classes the moves were also relatively muted. The Aussie 10-year dipped 4 bps, the dollar pulled back slightly, and REITs saw roughly a 0.4% swing. With Polymarket pricing the hike at ~80% beforehand, the market had largely pre-digested the outcome, and what should have been the main event of the day played out as a non-event (but still a painful one). That's a wrap for today.

RBA hikes by 25 bps to 4.10%

[2:30 pm] The RBA has hiked rates for a second straight meeting, up 25 bps to 4.10%.

This was a tight decision, with five members voting to hike and four voting to hold at 3.85%

Inflation picked up materially in the second half of 2025, with the Board judging that some of the increase reflects greater capacity pressures rather than purely temporary factors.

Short-term inflation expectations have already risen, and sustained higher fuel prices from the Middle East conflict pose further upside risk.

The labour market has tightened slightly, with unemployment a little lower than expected and underutilisation remaining at low rates.

Private demand growth strengthened substantially more than anticipated in late 2025, led by business investment, though consumption came in below expectations.

The Board flagged that the full effects of 2025 rate cuts are yet to flow through to demand, prices and wages, adding uncertainty about how restrictive current settings actually are.

The statement stressed the two-way risks from the Middle East conflict: A longer or more severe war could push energy prices higher and entrench inflation expectations, while prolonged uncertainty may weigh on growth in Australia's major trading partners and domestically.

Will the RBA hike, hold or cut?

[1:55 pm] Just over half an hour until the rate decision. What are we thinking?

ASX 200 back at breakeven

[1:42 pm] ASX 200 has faded the entirety of today's 0.57% gain, now trading back at breakeven.

Materials bounced 1.43%, now up just 0.33%

Financials up 0.82% to a two-week high, now up 0.27%

Tech up 1.51% in early trade, now down 0.90%

Discretionary up 0.39%, now down 1.0% and at the lowest since Jun-24

Perhaps some unease heading into the RBA decision at 2:30 pm (we'll keep the blog running till then).

Just how bad was Northern Star's selloff?

[1:35 pm] Northern Star experienced an 18.7% selloff last Friday, after the company cut its FY26 guidance (from 1.6-1.7Moz to "above" 1.5Moz) due to KCGM mill reliability issues and weaker mining productivity at Jundee. This marks the second production downgrade in less than three months.

The only comparable selloff in Northern Star's recent history was a 17.1% dip on 16 March 2020. Before that, declines of this magnitude were only seen when the stock traded below 10 cents.

Here's a list of NST's worst one-day declines:

Date | Close | % Chg |

|---|---|---|

10/10/2008 | $0.03 | -38.46% |

15/10/2008 | $0.03 | -33.33% |

23/06/2010 | $0.05 | -30.67% |

25/08/2009 | $0.03 | -30.00% |

3/03/2009 | $0.01 | -28.57% |

2/02/2009 | $0.01 | -25.00% |

24/09/2009 | $0.03 | -25.00% |

10/12/2009 | $0.03 | -25.00% |

19/02/2009 | $0.01 | -23.08% |

22/03/2005 | $0.08 | -21.43% |

27/06/2008 | $0.05 | -20.78% |

27/05/2004 | $0.08 | -20.00% |

13/03/2026 | $21.75 | -18.75% |

Top ASX 200 gainers

[1:30 pm] The All Ords Gold Index was up around 0.7% this morning, now up around 1.6%. A few gold names are catching a bid, notably West African Resources (opened 1.4% higher, now up 6.2%). The company reported its full-year result this morning, with net profit after tax up 130% to $576 million, valuing the company at a mere 5.7x.

Ticker | Company | % Chg | Price |

|---|---|---|---|

WAF | West African Resources | 6.12% | $2.95 |

SNZ | Summerset Group | 4.38% | $8.34 |

OBM | Ora Banda Mining | 4.15% | $1.43 |

WGX | Westgold Resources | 3.28% | $6.15 |

BPT | Beach Energy | 3.15% | $1.21 |

BGL | Bellevue Gold | 3.09% | $1.57 |

EVN | Evolution Mining | 3.05% | $13.50 |

AAI | Alcoa Corporation | 2.90% | $93.35 |

AUB | Aub Group | 2.65% | $24.04 |

GGP | Greatland Resources | 2.52% | $11.80 |

Top ASX 200 losers

[1:29 pm] Coal stocks, rare earths and growth-related names like Zip and Pro Medicus remain the market's laggards.

Ticker | Company | % Chg | Price |

|---|---|---|---|

ZIP | Zip Co | -5.96% | $1.50 |

NHC | New Hope Corporation | -5.38% | $5.02 |

LYC | Lynas Rare Earths | -4.41% | $20.07 |

EOS | Electro Optic Systems | -4.10% | $10.28 |

YAL | Yancoal Australia | -3.64% | $7.67 |

DYL | Deep Yellow | -3.55% | $1.71 |

PME | Pro Medicus | -3.46% | $127.10 |

GQG | GQG Partners | -3.43% | $1.63 |

ILU | Iluka Resources | -3.18% | $6.24 |

NXG | Nexgen Energy | -3.15% | $16.60 |

Morgan Stanley flags diesel supply as key risk for Australian economy

[1:27 pm] Morgan Stanley examines Australia's fuel vulnerability amid the Middle East conflict, concluding petrol supply should be manageable but diesel disruption would carry material economy-wide consequences.

Australian petrol averaged $2.10/L on Friday (2025 avg $1.80/L)

Diesel averaged $2.50/L (2025 avg $1.86/L), with spot input prices pointing higher still

Australia's net import fuel cover sits at ~49 days as of January 2026, with the government authorising a 762ML release of strategic petrol and diesel reserves and temporarily relaxing fuel standards to allow high-sulphur fuels from Lytton refinery (~100ML) for domestic use

Diesel is the critical watch given fewer substitutes and broad industrial reliance. MS estimates Australia could manage ~26% lower diesel imports before industrial shutdowns would be required

Oil supplies may take months to return to pre-conflict levels even if the conflict ends, with many global markets prioritising refined products for domestic use

A temporary fuel excise cut is a plausible policy response (as per the March 2022 precedent), while MS flags demand-side rationing scenarios as a possibility if supply tightens further

Morgan Stanley sees gold upside but flags rising two-way risks

[1:25 pm] Morgan Stanley remains constructive on gold but acknowledges the Middle East conflict introduces more uncertain macro dynamics that could challenge the bullish case.

Gold is down 5% since the start of the conflict (Feb 27), with strong prior YTD gains, a firmer USD and liquidity-driven selling outweighing geopolitical safe haven flows

MS retains a 2H bull case of US$5,700/oz, driven by central bank buying, Fed rate cuts supporting ETF inflows and growing investor interest in real assets

Key risk is that persistent inflation forces the Fed to hold or hike rather than cut, which history (2H22) shows can trigger ETF liquidation and pressure gold despite elevated geopolitical risk

MS economists still expect two Fed cuts this year (June and September), but acknowledge the outlook is more finely balanced than before the conflict

Poland's central bank flagging more "active management" of its gold reserves raises questions about the durability of central bank purchasing, a key pillar of the gold bull case

New Hope 1H26 earnings call highlights

[12:57 pm] Some interesting takeaways from New Hope's earnings call, especially around fuel costs.

Diesel accounts for ~13% of costs with no near-term supply risks identified, while rising coal prices are more than offsetting diesel cost pressures

Bengalla expected to maintain a ROM coal run rate of 13.4Mt per annum in H2 FY26, with full-year physicals and cash cost targets on track

~$130m in growth capital to be deployed at New Acland over the next 12 months, with mining at Manning Vale West Pit to commence in Q4 CY26

Sales dominated by long-term contracts with consistent Asian destinations, limiting spot exposure and providing revenue visibility

Capital allocation focused on New Acland ramp-up and Bengalla fleet replacement, with the share buyback remaining opportunistic and the significant franking account balance supporting future fully franked dividends

UBS initiates on five ASX gold names

[12:05 pm] UBS has launched coverage on five ASX-listed gold stocks, taking its team gold coverage to 14 names, with a constructive view on production growth and a supportive gold price backdrop.

All five initiations carry a Buy rating with significant implied upside vs. 16 March closing prices: Pantoro (120%), Minerals 260 (88%), Catalyst Metals (83%), Westgold (72%) and Ora Banda (16%)

Production volume CAGR to FY30 across the five names ranges from 8% to 22%, driven by better utilisation, higher throughputs and higher grades

UBS's gold price forecasts remain supportive at US$5,200/oz for CY26 and US$3,250/oz long-term real, underpinned by Middle East conflict, trade tensions, weak global growth and dedollarisation

Order of preference is PNR > WGX > MI6 > CYL > OBM, largely driven by valuation support. PNR is the top pick among emerging producers, while WGX screens well in mid-caps on a cheaper EV/EBITDA multiple and higher near-term FCF yield versus Gold Road (GMD)

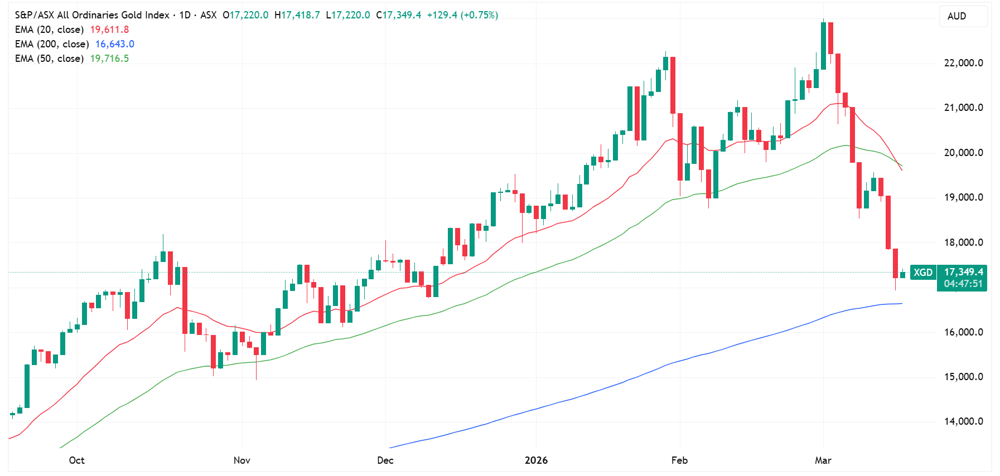

A tiny bounce for gold miners

[11:12 pm] The All Ords Gold Index is up 0.7% in early trade, a rather tiny bounce after falling 11.4% in the previous three sessions (and down almost 25% since 2-Mar).

Gold prices slipped 0.2% overnight to US$5,007/oz.

All Ords Gold Index daily chart (Source: TradingView)

UBS assesses CMRG iron ore restrictions on BHP

[11:10 am] UBS examines the evolving CMRG negotiations and their impact on BHP's realisations, while noting spot prices are lifting fair values across diversified miners and bulk producers.

CMRG expanded restrictions on BHP cargoes on 5 March, instructing traders to limit purchases of Newman and MAC products on top of earlier bans on Jimblebar fines and Jinbao.

However, on 14 March CMRG temporarily eased the Jimblebar fines ban for steel mills (not traders) to address supply shortages amid surging iron ore prices.

Prolonged CMRG negotiations could see BHP's WAIO volumes discounted while alternate supply attracts premiums, with extended discounts estimated to reduce BHP's FY26 EBITDA by roughly US$0.3bn (approximately 1%).

Vulcan Energy secures 6-year lithium production licence

[11:08 am] Vulcan Energy Resources has been granted a lithium production licence for its Lionheart project in Germany, marking a key regulatory milestone ahead of targeted commercial production. This announcement was released shortly after market open, with Vulcan shares currently up ~3%.

The LiThermEx licence covers Vulcan's Insheim geothermal production permit area within Lionheart, which is already producing renewable heat and power

Vulcan will look to extend the permit to a minimum of 30 years following the initial 6-year term

Commercial production at Lionheart is targeted to commence in 2028

Company page: Vulcan Energy Resources (VUL)

Challenger cuts Pepper Money takeover bid

[10:24 am] Challenger has lowered its non-binding indicative offer for Pepper Money by 13.5%, describing the revised price as its best and final offer.

The revised proposal of $2.25 per share is down from the original $2.60 offer.

Challenger cited deterioration in both market conditions and the operating environment as the reason it is not prepared to proceed at the earlier price.

The $2.25 price is inclusive of the 2025 final dividend of 7.8 cents per share (fully franked) and any special dividend, meaning the ex-dividend value to shareholders would be lower.

Challenger has stated the revised proposal is its best and final offer in the absence of a superior proposal from a competing bidder.

Company page: Pepper Money (PPM)

Analysts take on Perpetual

[10:22 am] Perpetual shares nudged 1.8% higher on Monday after the company agreed to sell its wealth management business to Bain Capital for $500 million, with an earn out payment of up to $50 million. Here's what analysts are thinking:

JPMorgan retained Neutral, target unchanged at $19.50. Terms broadly matched internal valuation views with additional payments providing some upside, though the separation process carries client retention execution risk.

Morgan Stanley retained Equal-Weight, target unchanged at $20.30. The outcome was seen as practical and sensible, with debt reduction leaving the balance sheet comfortable and brand retention improving strategic appeal.

Top ASX 200 gainers

[10:17 am] Iperionx is bouncing after falling 42% in the last three sessions, a few resource names (gold, aluminium) also bouncing.

Ticker | Company | % Chg | Price |

|---|---|---|---|

IPX | Iperionx | 5.62% | $4.32 |

EOS | Electro Optic Systems | 4.38% | $11.19 |

CGF | Challenger | 4.07% | $7.68 |

AUB | AUB Group | 3.80% | $24.31 |

WAF | West African Resources | 3.24% | $2.87 |

4DX | 4DMedical | 3.13% | $3.95 |

AAI | Alcoa Corporation | 3.04% | $93.48 |

RWC | Reliance Worldwide | 2.88% | $3.21 |

ZIM | Zimplats | 2.85% | $17.70 |

OBM | Ora Banda Mining | 2.55% | $1.41 |

Top ASX 200 losers

[10:17 am] New Hope is tumbling off the back of its 1H26 result, though most coal names are down 2-3%. Other sectors including uranium, energy and select tech names are also trading lower.

Ticker | Company | % Chg | Price |

|---|---|---|---|

NHC | New Hope Corporation | -7.17% | $4.92 |

SNZ | Summerset Group | -6.00% | $7.99 |

YAL | Yancoal Australia | -3.27% | $7.70 |

NXG | Nexgen Energy | -3.15% | $16.60 |

MCY | Mercury NZ | -2.77% | $5.27 |

VEA | Viva Energy Group | -2.40% | $2.03 |

WHC | Whitehaven Coal | -2.37% | $8.64 |

XYZ | Block | -1.86% | $84.55 |

PME | Pro Medicus | -1.84% | $129.23 |

REH | Reece | -1.79% | $14.24 |

ASX 200 higher after three-day losing streak

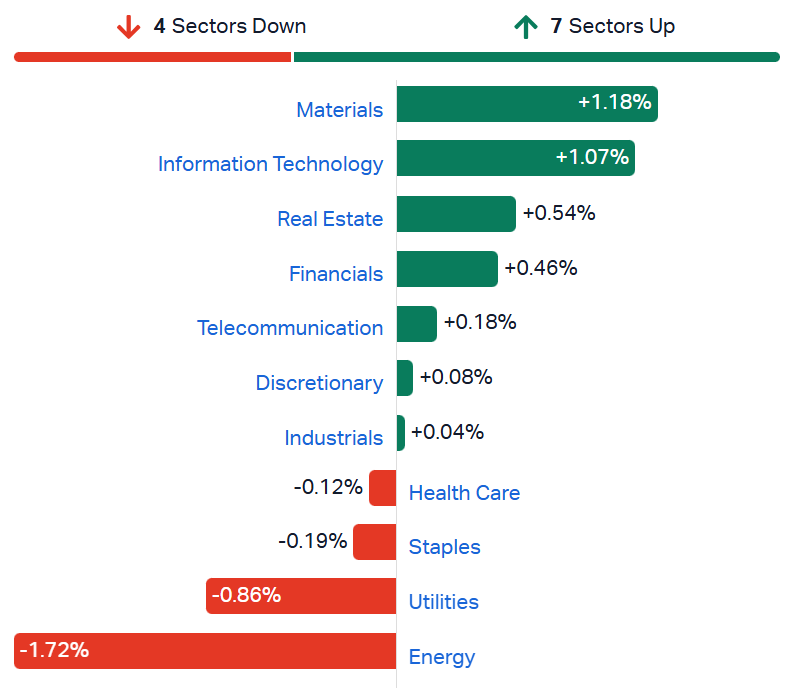

[10:10 am] The ASX 200 is up 0.50% in early trade, potentially snapping a three-day losing streak. Yesterday's losers are today's winners, with Materials (+1.1%) and Tech (+1.0%) leading the bounce after dropping 2.2% and 1.5% respectively on Monday, while defensives and Energy lag.

The ASX 200 has fallen for three consecutive sessions and trading below the key 200-day moving average. We're seeing a slight oversold bounce as the market welcomes an overnight session where bond yields and oil prices eased (WTI down 5.1% to US$94.2). That said, Middle East risks haven't gone away. Attacks on regional energy infrastructure continue, and there's still no clarity around Strait of Hormuz coalition efforts or shipping flows. Elevated hedging activity and depressed sentiment may offer some near-term support, but analysts note the absence of meaningful capitulation.

ASX 200 sectors (Source: Market Index)

New Hope posts 84% profit decline

[9:42 am] New Hope delivered solid operational output in 1H26, but sharply lower realised pricing weighed heavily on earnings and cash flow. Coal prices (gC NEWC 6000) average US$108 a tonne in the first half, down 20.5% compared to a year ago.

Consensus coverage for this half-year result is relatively thin, so estimates may vary considerably from actuals.

Revenue up 1.5% to $814.4m vs. $802.7m ests (1.5% beat)

Underlying EBITDA down 58.5% to $214.8m vs. $216.2m ests (0.6% miss)

Net profit after tax down 84% to $54.3m vs. $77.9m ests (30.3% miss)

Operating cash flow down 41.6% to $185.0m

Available cash of $616.8m

Interim dividend down 47% to 10.0 cps

Operational highlights:

Group saleable coal production was broadly flat at 5.5Mt, while FOR cash costs rose 9.2% to $60.6/t driven by increased prime overburden movement at Bengalla.

Bengalla is expected to return to its 13.4Mtpa ROM production rate (100% basis) in H2 FY26 following pit sequence re-alignment after weather disruptions.

New Acland continues ramping toward approximately 5Mtpa, with access to the Manning Vale West pit scheduled for late calendar year 2026.

New Hope increased its stake in Malabar Resources by 3% to 25.97%, adding exposure to high-quality metallurgical coal consistent with its strategy to invest in low-cost, long-life coal assets.

Company page: New Hope Corporation (NHC)

West African Resources is printing cash

[9:26 am] The unhedged gold miner reported strong full-year results underpinned by high-margin production from Sanbrado and the successful ramp-up of Kiaka.

Revenue up 111% to $1.54bn

Net profit after tax up 130% to $567m

Operating cash flow up 213% to $790m

Cash and gold bullion of $584m plus 27,095 oz of unsold bullion at year end

Gold production up 45% to 300,383 oz at an AISC of US$1,488/oz (up 20%)

Kiaka was constructed and ramped up on budget during the year, with the first five months of production now contributing. A full year of output from both Sanbrado and Kiaka in 2026 is expected to further improve revenue and operating cash flow.

West African Resources has slumped in recent weeks alongside the broader gold sector, down 28.9% since 29 January. At a market cap of $3.2 billion, the stock trades on a price-to-earnings ratio of just 5.7x. Macquarie analysts expect the company to be absolutely printing cash over the next two years, with free cash flow yields of 33% and 32% respectively. The key risk, however, lies in its ongoing discussions with the Burkina Faso Government following an EOI (received in late August 2025) for increased ownership in Kiaka.

Company page: West African Resources (WAF)

Meeka Metals to boost Murchison processing capacity

[9:18 am] The company is installing ore sorting technology at its Murchison Gold Project to unlock additional mill capacity and accelerate gold production at a fraction of the cost of a conventional plant expansion.

The upgrade adds roughly 200ktpa of processing capacity, lifting throughput from the current 600ktpa nameplate to approximately 800ktpa, with commissioning targeted for the September 2026 quarter.

Test work confirmed ore sorting separates roughly 85% of contained gold into approximately 50% of the rock mass, effectively doubling Andy Well's already high underground head grade entering the plant.

Capital cost of just $6m, funded from existing cash, compares favourably to a conventional crushing and grinding circuit expansion that would cost significantly more to achieve equivalent 800 to 1,000ktpa capacity.

Meeka is one of the market's newest gold producers, with its latest quarterly report (Dec-25) delivering 9,174 ounces at $2,365/oz AISC.

Company page: Meeka Metals (MEK)

Rio Tinto completes historic land exchange

[9:13 am] The Rio Tinto (55%) and BHP (45%) joint venture has cleared a major regulatory hurdle in Arizona, with approximately $500 million in preliminary spending now planned over two years.

The US Forest Service and Resolution Copper have completed a land exchange following a 13 March ruling by the Ninth Circuit Court of Appeals in favour of the project and the federal government, ending a long-running legal challenge. The exchange was originally enabled by bipartisan legislation passed in 2014.

Resolution Copper transferred more than 5,400 acres of environmentally and culturally sensitive land into National Forests and Conservation Areas, and received over 2,400 acres adjacent to the historic Magma copper mine in Superior, Arizona.

The joint venture announced roughly $500m in preliminary spending over two years for enabling works including surface drilling for additional resource data, upgrades to existing infrastructure, initial underground development and approximately 100 new jobs.

The milestone is significant for both Rio Tinto's copper growth pipeline and BHP's exposure to long-life copper resources, coming at a time of strong structural demand for the metal driven by electrification and infrastructure buildout.

Company page: Rio Tinto (RIO)

Wall Street strategists hold targets but flag oil as the key risk to equities

[9:10 am] Major investment banks banks are maintaining base cases for now, but the Iran war and sustained crude prices above US$100 are increasingly testing conviction.

Goldman Sachs kept its S&P 500 year-end target at 7,600, citing ongoing AI spending as an offset to softer growth and potentially fewer Fed rate cuts. However, warned that an oil supply shock matching recent historical precedents could push the index to 5,400, roughly 23% below the latest peak.

BofA's trading desk said the path of least resistance is lower, noting the Consensus Longs basket (a historically leading indicator) has already broken below its 200-day moving average. Flagged anecdotal consensus that the breaking point for equities would be crude holding above $105 for a month or more, and noted markets are still pricing in the possibility of negotiation or de-escalation.

Morgan Stanley expects ongoing volatility and potential further lows driven by geopolitical uncertainty, but sees durable technical support in the 6,400 to 6,500 range if the S&P 500 breaks its 200-day moving average at 6,600. Remains constructive medium-term on the back of earnings momentum and fiscal support from OBBBA.

Citi left its base case unchanged but flagged the Iran disruption, private credit uncertainty and AI-related tail risks as impossible to ignore. Still argued the US should be a relative safe haven, with megacap growth and the AI trade offering good earnings visibility and limited macro sensitivity for now.

S&P 500 earnings growth expected to continue

[9:05 am] Despite the ongoing energy turmoil from Iran, Wall Street is looking for a sixth consecutive quarter of double-digit earnings growth for the S&P 500.

Consensus is expecting 11.6% earnings growth in the first quarter, following 14.1% growth in Q4, according to FactSet.

Eight of eleven sectors are forecast to post year-on-year earnings gains, led by Tech (+41.7%), Materials (+24.6%) and Financials (+11.6%).

Earnings momentum remains the key pillar of the bull case amid elevated geopolitical uncertainty, with JPMorgan pointing to accelerating leading indicators and ISM manufacturing at near three-year highs.

Goldman Sachs flagging AI capex as an offset to softer economic activity, and Morgan Stanley arguing accelerating earnings growth distinguishes this cycle from prior late-cycle periods derailed by oil shocks.

Retail investors pile into oil ETFs at record pace, drawing "meme stock" comparisons

[9:01 am] The Iran war-driven volatility in crude markets is attracting a surge of speculative retail trading, with analysts warning the momentum could reverse sharply.

Net retail buying of oil ETFs hit a record $211m on 12 March, surpassing the previous peak set during the May 2020 market turmoil, according to Vanda Research.

Analysts are drawing parallels with past meme trading frenzies in GameStop and silver.

Reddit forums show traders boasting of quick profits and debating whether the rally still has room to run.

The Crude Oil Volatility Index has surged to its highest level since 2020, with prices up roughly 40% in two weeks. Analysts note the scope for sudden escalation or de-escalation means oil will continue to trade with "erratic and enlarged price swings" throughout the conflict.

The underlying supply disruption is real, with the IEA estimating roughly 10 million barrels per day of production has been shut in.

Source: CNBC

Bond managers bet on central bank divergence

[8:59 am] Fund managers are positioning for a widening split in global monetary policy, arguing the war in Iran will not trigger synchronised rate hikes across major economies.

Before the war, economists were forecasting the widest divergence in major central bank policy direction since at least 2009, and investors say the conflict has reinforced rather than closed that gap

Several managers are buying short-dated bonds in the UK, Europe and Australia, arguing markets have priced in too many hikes given the weaker growth backdrop compared to 2022

Others favour long-dated Australian, Japanese and New Zealand bonds where central banks had already turned hawkish, viewing these as more straightforward trades

Markets have now flipped from pricing rate cuts to hikes in the UK and Europe, while expectations for US cuts this year have faded

German 10-year yields hit their highest since October 2023 after ECB's Peter Kazimir flagged the war could force earlier rate increases, highlighting how sensitive markets are to policymaker rhetoric

Source: Bloomberg

US allies resist Trump's call to send warships to the Strait of Hormuz

[8:58 am] Years of strained relations over tariffs, NATO spending and the Ukraine war are leaving Trump with few willing partners to help reopen the world's most critical oil chokepoint.

Europe, Japan, South Korea and China have all stopped short of committing naval assets, with Germany's Defence Minister questioning what "a handful of European frigates" could achieve that the US Navy cannot. The EU requires unanimous approval to redirect its Red Sea naval mission toward Hormuz, and Berlin is blocking the move.

Japan has made no commitment to dispatch escort ships ahead of PM Takaichi's White House visit this week. South Korea is similarly reviewing the request without committing.

China is unlikely to support US military operations. State media dismissed Trump's request as an attempt to spread the risk of "a war that Washington started and can't finish."

Source: Bloomberg

Fujairah port partially resumes

[8:55 am] The UAE's key oil export hub outside the Strait of Hormuz has been hit by a second drone attack in days, raising the stakes for global supply.

A drone strike on Monday caused a fire in Fujairah's petrochemicals area. While some port operations have resumed, Adnoc's crude oil loadings remain suspended, with authorities not disclosing full operational details.

Iran's military warned over the weekend that Fujairah, Jebel Ali and Port Khalifa are now "legitimate targets" due to the presence of US military forces, signalling the risk of further disruption to the UAE's only oil export route that bypasses the Strait of Hormuz.

Fujairah is the primary export terminal for the UAE's Murban crude, connected by pipeline to Abu Dhabi's main oil fields, with over 70 million barrels of storage capacity and a major ship refuelling role.

Source: Bloomberg

IEA signals more strategic oil reserves available if needed

[8:54 am] The IEA has flagged it retains significant firepower to release further oil from strategic stockpiles following last week's record drawdown, as the Strait of Hormuz closure continues to disrupt global supply.

The IEA's largest-ever coordinated reserves release drew down roughly 20% of strategic stocks, with approximately 1.4 billion barrels still available for further action "as and if needed"

The IEA warned the release is a temporary buffer, not a lasting solution, and that even if the Strait reopened immediately, a full recovery in global energy trade would take time

Oil-importing emerging economies in South and Southeast Asia are the worst affected, while key Middle East producers like Iraq are losing critical export revenues

Russia's oil export windfall hits post-invasion high

[8:51 am] Russia is capitalising on soaring global oil prices and US sanctions relief to dramatically boost crude export volumes and revenues.

Weekly seaborne crude shipments surged to 3.97 million barrels per day in the week to 15 March, up roughly 1.1 million barrels per day and the highest in about three months, driven by resumed flows from the Black Sea terminal at Novorossiysk and higher Arctic and Pacific loadings.

The gross value of exports jumped to approximately $2.07bn for the week to 15 March, up $890m from the prior week, marking the biggest weekly income increase since Russia's invasion of Ukraine.

Delivered prices to India hit a record US$70.23 per barrel, boosted by the Strait of Hormuz disruption lifting global benchmarks.

A US tariff waiver extension allowing buyers to purchase Russian crude loaded before 12 March without sanctions risk is accelerating the clearance of a roughly 140 million barrel backlog of Russian crude sitting on tankers at sea, with vessels increasingly diverting toward India.

Source: Bloomberg

US indices bounce

[8:50 am] Major US benchmarks finished broadly higher, though struggled to hold onto intraday highs. The S&P 500 snapped a four-day losing streak to close 1.01% higher, off session highs of 1.47%.

S&P 500 daily chart (Source: TradingView)

Good morning!

[8:30 am] ASX 200 futures are up 66 pts (+0.76%) as of 8:30 am AEDT.

Local sharemarket set to bounce after a three-day losing streak, though the RBA meeting (widely expected to hike) could rattle markets

Major US benchmarks higher but struggled to hold onto session highs, all sectors finished higher, with Tech and Discretionary leading gains

WTI crude fell 5.1% to US$94 as Trump said the White House will soon announce which countries have agreed to participate in a coalition to protect tankers through the Strait of Hormuz