ASX 200 Live Today - Tuesday, 10th March

The S&P/ASX 200 is set for a massive bounce amid a sharp reversal in oil prices and potential de-escalation in the Middle East.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Tuesday, March 10. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

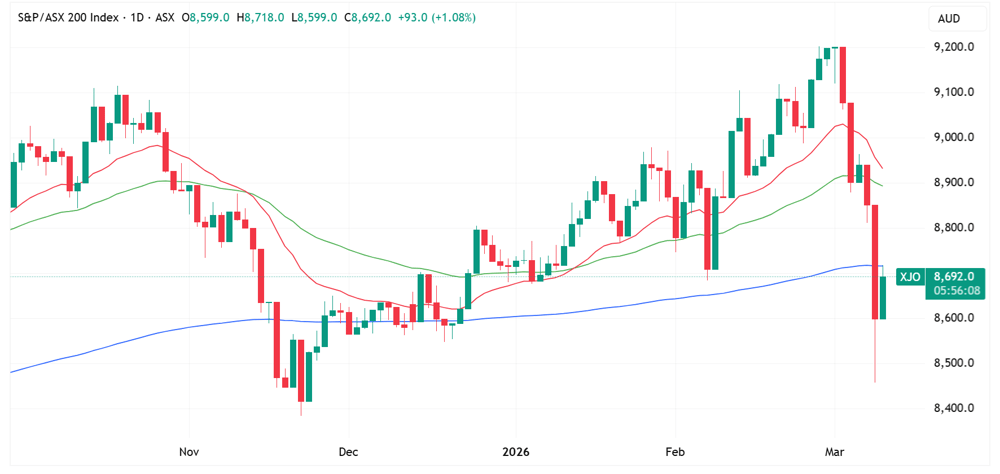

ASX 200 higher, off best levels

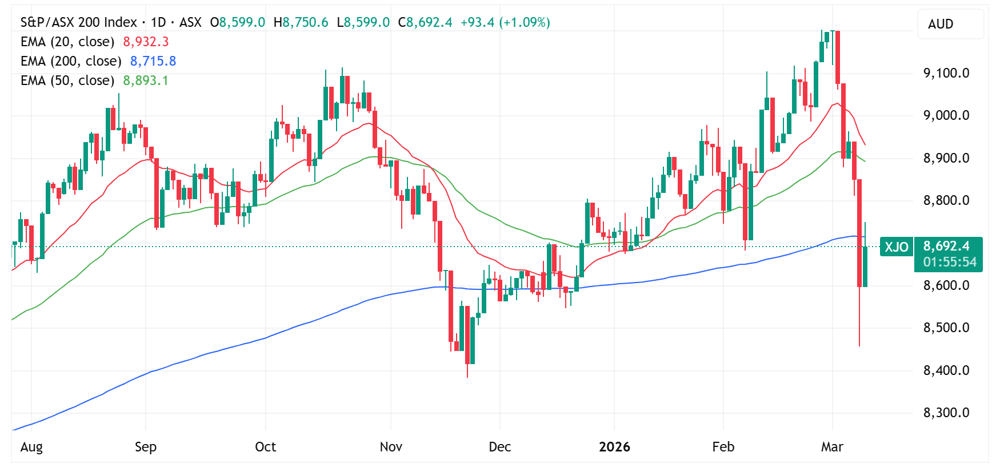

[2:10 pm] ASX 200 trading 1.15% higher, off session highs of 1.76%. This follows a sharp unwind from record highs over the past five days, where the index tumbled 6.5%.

Markets remain extremely volatile and unpredictable, much like Trump's answer to a journalist who asked: "You said the war is 'very complete.' But your defence secretary says 'this is just the beginning.' So which is it?"

He answered: "You could say both."

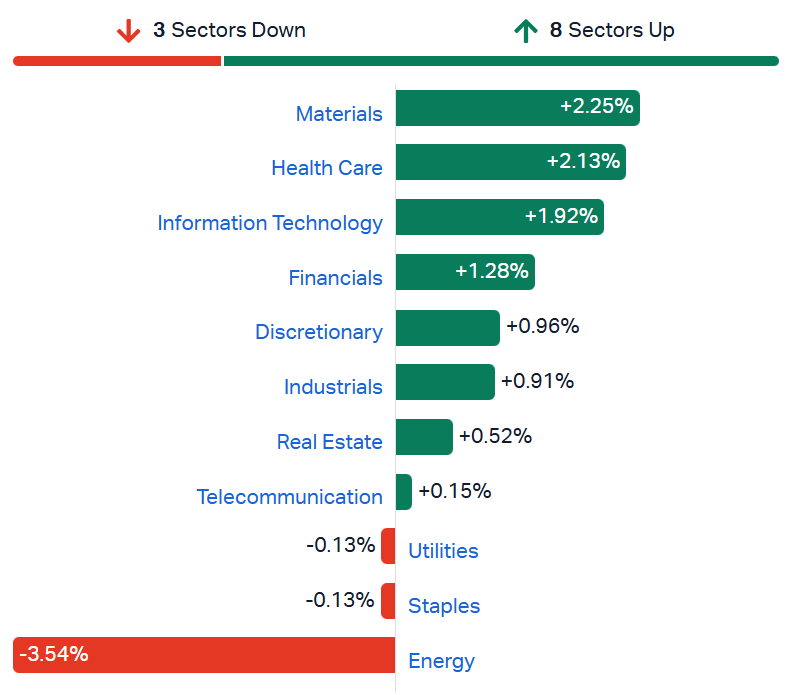

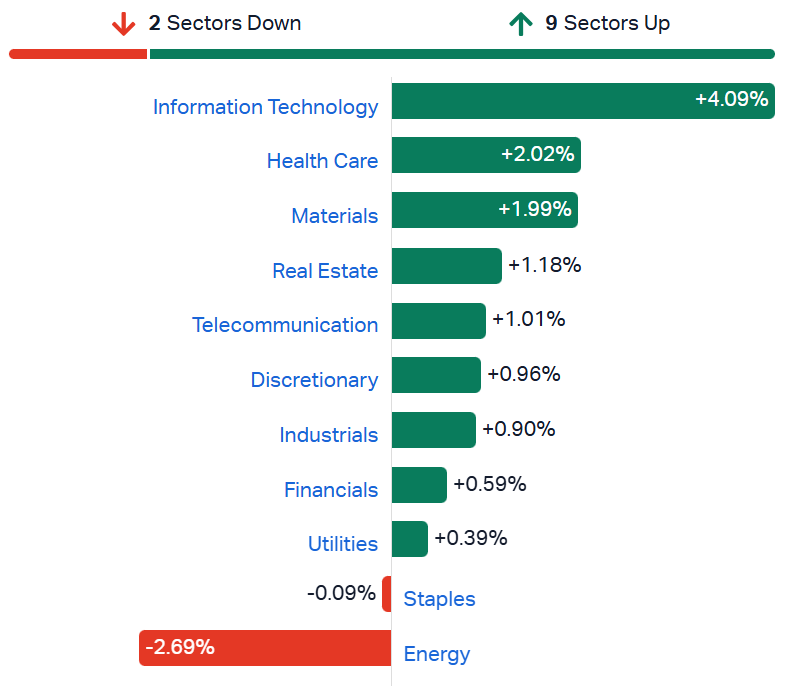

Materials topped the leaderboard today, snapping a five-day losing streak where the Materials Index dipped 14.6%. Tech has also been a pocket of relative strength in recent weeks, though the Tech Index will close well off session highs of 4.0%.

ASX 200 sectors (Source: Market Index)

ASX 200 daily chart (Source: TradingView)

Building conviction at times like this is difficult. Markets have historically shrugged off geopolitical events over the following month or two, but the oil supply challenge remains very real, and has already flipped some major central bank rate forecasts from cuts to hikes.

Source: Author's own calculations

Tech stocks struggle to hold onto session highs

[1:00 pm] The S&P/ASX 200 Tech Index spiked 4.0% in early trade, now up just 1.8%. This reflects a relatively broad-based pullback for most large cap names (e.g. Wisetech rallied as much as 5.4%, now up just 0.8%). Nevertheless, the Tech Index has mustered up a solid bounce in recent weeks, up 11.2% from its 24-Feb low.

Here's how tech names are performing today, plus YTD performances.

Ticker | Company | % Chg | Price | YTD % Chg |

|---|---|---|---|---|

360 | Life360 | 10.51% | $22.55 | -30.03% |

WBT | Weebit Nano | 4.47% | $4.67 | -6.60% |

PME | Pro Medicus | 4.46% | $137.37 | -37.68% |

OCL | Objective Corporation | 4.14% | $13.58 | -17.95% |

TNE | Technology One | 4.03% | $27.38 | -0.58% |

DTL | Data#3 | 3.93% | $7.40 | -17.50% |

AD8 | Audinate Group | 3.21% | $2.89 | -28.57% |

CAT | Catapult Sports | 3.09% | $3.84 | -7.81% |

CDA | Codan | 2.90% | $35.43 | 24.67% |

MAQ | Macquarie Technology Group | 2.42% | $62.69 | -6.43% |

SDR | Siteminder | 2.07% | $3.45 | -43.64% |

PPS | Praemium | 2.05% | $0.75 | -6.29% |

NXL | Nuix | 1.69% | $1.81 | 0.00% |

HSN | Hansen Technologies | 1.36% | $5.22 | -1.14% |

MP1 | Megaport | 1.33% | $8.02 | -34.20% |

DDR | Dicker Data | 1.01% | $9.01 | -12.54% |

BVS | Bravura Solutions | 0.98% | $2.07 | -19.46% |

WTC | Wisetech Global | 0.85% | $51.09 | -25.36% |

IRE | Iress | 0.13% | $7.51 | -10.38% |

XRO | Xero | 0.04% | $83.45 | -26.69% |

NXT | NextDC | -0.16% | $12.79 | 1.75% |

DGT | Digico Infrastructure Reit | -1.76% | $1.85 | -33.80% |

WTI crude update: Prices fade early gains

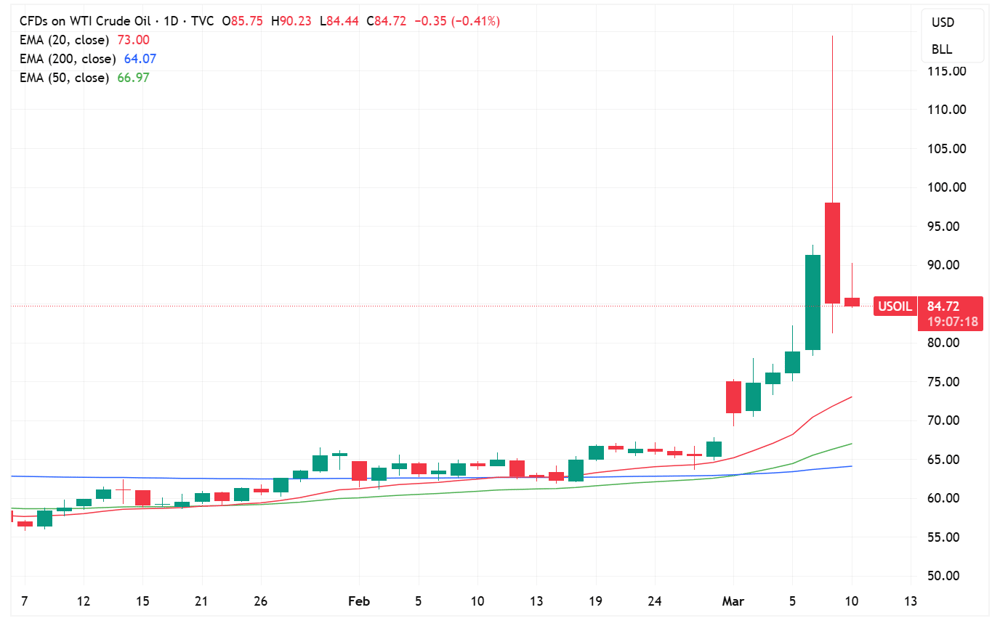

[12:55 pm] WTI crude was trading 6.0% higher (US$90.23) this morning but currently down 0.4% to US$84.77.

WTI crude daily price chart (Source: TradingView)

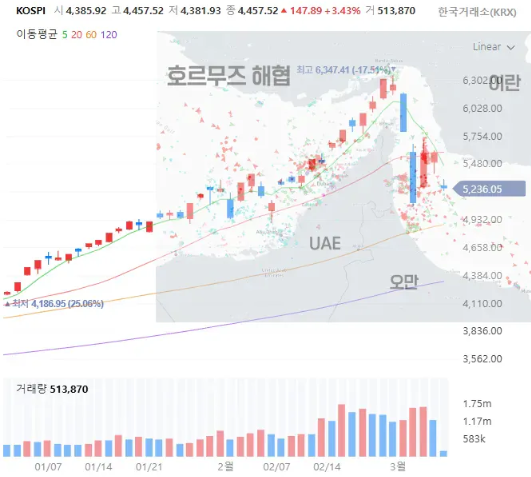

South Korea's KOSPI bounces 6pc

[12:48 pm] The KOSPI has arguably logged the most volatility in recent days, including:

Tuesday, 3 March: Down 7.2%

Wednesday, 4 March: Down 12.0%

Thursday, 5 March: Up 6.2%

Friday, 6 March: Up 0.02%

Monday, 9 March: Down 5.9%

Today: Up 6.2%

Through all of this volatility, the index is still up 32% year-to-date.

On a more light hearted note, an X user (@moneykhan80) laid the KOSPI chart over the Strait of Hormuz.

Mongolia pushes to renegotiate "unfair" Oyu Tolgoi deal with Rio

[12:45 pm] Senior Mongolian officials are meeting Rio Tinto executives in Ulan Bator this week to demand better terms on the $18 billion Oyu Tolgoi copper mine, citing cost overruns, delayed dividends and near-record copper prices as leverage.

Mongolia holds a 34% stake in Oyu Tolgoi via state miner Erdenes Mongol, but funded its share through a Rio Tinto loan now carrying an interest rate above 11%

Repeated cost overruns have pushed the expected dividend start date from 2017 to around 2037

Key government demands include reducing the loan interest rate to below 6% and phasing out Rio's annual management fee, estimated at $150-200m per year

Mongolia has flagged it could raise the export tax on copper beyond the current ~5% if negotiations fail, while Rio separately faces a $450m tax probe in the country over depreciation accounting differences in 2021-22

Oyu Tolgoi is Rio's largest copper development and is expected to become the world's fourth largest copper mine by 2030, producing ~500,000 tonnes per year, giving Mongolia significant political motivation ahead of elections next year

Source: Financial Times

UBS' take on global inflation shocks

[11:48 am] Monday's selloff left Energy as the only rising sector on the ASX, with rising oil prices driving a bond yield spike that UBS says historical precedent suggests could persist for weeks.

The AU 10-year yield hit a 15-year high on Monday, consistent with the roughly 50 bp selloff seen in the month following both the 1990-91 Gulf War and Russia's invasion of Ukraine in 2022, according to UBS

In both prior inflation shock episodes, UBS notes Resources and Energy outperformed Banks, with the 2022 Ukraine experience showing particularly clear price leadership from resource equities

Australian stocks also proved resilient over a 12-month horizon, outperforming global equities by 10% in the year following Russia's invasion

UBS notes the de-rate over the past month has pushed the ASX median PE to 16.9x, its lowest since October 2023 and below the 10-year average of 18.4x, with valuations now near the 20-year average of 16.5x

Healthcare is flagged by UBS as the most compelling valuation story among ASX sectors at current levels

Top ASX 200 gainers

[11:44 am] A rather tech-and-resources led session, with Life360 recouping all of yesterday's 6.9% dip, while lithium and copper stocks bounce.

Ticker | Company | % Chg | Price |

|---|---|---|---|

360 | Life360 | 9.51% | $22.34 |

PDN | Paladin Energy | 8.84% | $12.19 |

TLX | Telix Pharmaceuticals | 6.18% | $10.83 |

RSG | Resolute Mining | 5.99% | $1.42 |

NXG | Nexgen Energy | 5.91% | $17.57 |

MIN | Mineral Resources | 5.14% | $57.10 |

VGN | Virgin Australia | 4.93% | $2.88 |

PDI | Predictive Discovery | 4.79% | $0.88 |

SFR | Sandfire Resources | 4.72% | $16.43 |

NWH | NRW | 4.70% | $5.79 |

Top ASX 200 losers

[11:44 am] Pretty much all of yesterday's top gainers are today's top losers. Though Pantoro is getting smashed after downgrading its FY26 production guidance.

Ticker | Company | % Chg | Price |

|---|---|---|---|

PNR | Pantoro Gold | -19.84% | $3.92 |

RYM | Ryman Healthcare | -6.15% | $1.83 |

YAL | Yancoal Australia | -5.02% | $6.81 |

NHC | New Hope Corporation | -4.54% | $4.95 |

WDS | Woodside Energy Group | -4.53% | $29.94 |

ALD | Ampol | -4.05% | $30.08 |

BPT | Beach Energy | -3.86% | $1.12 |

VEA | Viva Energy Group | -3.54% | $1.99 |

STO | Santos | -3.27% | $7.39 |

DNL | Dyno Nobel | -2.78% | $2.98 |

Australian consumer sentiment edges up but Middle East fears cloud the outlook

[10:51 am] The Westpac-Melbourne Institute Consumer Sentiment Index nudged higher in March, but intra-week deterioration signals the Iran conflict is increasingly weighing on household confidence.

The index rose 1.2% to 91.6 in March from 90.5 in February, leaving consumers firmly in pessimistic territory

Daily responses in the final three days of the survey week pointed to an index read of just 84, consistent with a sharp deterioration as Middle East headlines escalated

The "economy, next 12 months" sub-index fell 2.9% to 85.9, its weakest read since September 2024 and below the long-run average of 90.7

The "time to buy a dwelling" index hit a new cycle low of 82.9, more than 36 points below its long-run average of 120

Mortgage rate expectations remain elevated with over 75% of consumers expecting variable rates to rise further over the next 12 months

Recall rates on 'international news' doubled vs. December with nearly 90% of consumers viewing offshore developments unfavourably, a deterioration comparable to the period immediately following Russia's invasion of Ukraine in early 2022

Westpac expects the RBA to hold rates at its March 16-17 meeting given global uncertainty, with the next rate rise now expected in May

Source: Westpac Economics

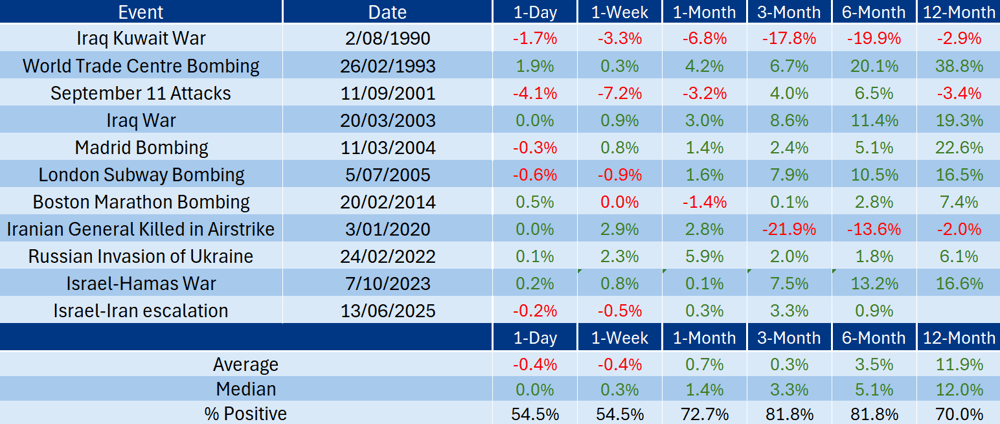

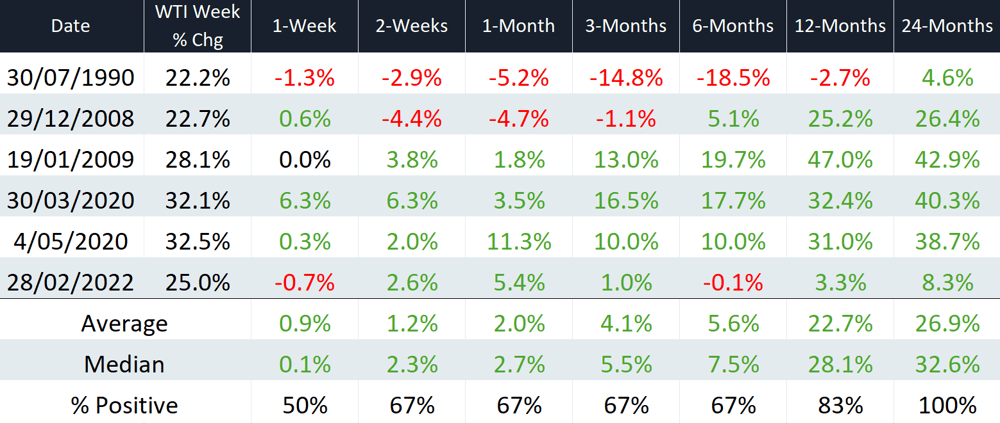

How does the market perform after an oil price shock?

[10:34 am] WTI crude rallied 35% last week to US$91 a barrel (vs. US$89 right now) – which got me thinking, how does the market perform after an oil price spike?

The table below looks at how the S&P/ASX 200 (price, not total returns) has performed in the weeks following a crude oil rally of 20% or more, going back to 1990.

How the S&P/ASX 200 performs after an oil price shock (Source: Author's own calculations)

ASX 200 bounces, Tech and Healthcare lead

[10:07 am] The ASX 200 is up 1.28% in early trade, recovering just under half of yesterday's decline as the index rallies back toward the 200-day moving average, though it has yet to push through. Tech is shaping up as one of the stronger sectors out of this drawdown (unsurprising given the recent beating and record shorts), with the XIJ recovering almost all of yesterday's losses. WiseTech, Xero, NextDC and Technology One are all up between 2% and 5%.

S&P/ASX 200 sectors (Source: Market Index)

ASX 200 daily chart (Source: TradingView)

Orica first half EBIT to edge higher

[9:47 am] Orica's first half trading update flagged a mixed divisional performance with group EBIT slightly above the prior year, alongside a new cost-out program targeting at least $100 million in annualised savings.

Group 1H26 EBIT to be slightly higher year-on-year

Blasting Solutions EBIT slightly below year-on-year, offset by Digital Solutions EBIT up ~20% and Specialty Mining Chemicals EBIT up ~15%

Significant items of $45-60m ($55-75m pre-tax) to weigh on first half reported earnings

A company-wide restructure has commenced targeting at least $100m in annualised cost savings to be realised over the next three years

Net operating cashflow for both the half and full-year 2026 expected to be lower than 2025, driven by FX movements, US litigation costs and the CF Industries plant outage in North America

No immediate operational constraints from the Middle East conflict

Company page: Orica (ORI)

FleetPartners launches $20m on-market buyback

[9:37 am] FleetPartners has approved a $20 million on-market share buyback, supplementing its existing 60-70% dividend payout ratio. The stock is down 16% year-to-date and down 13% in the last twelve months.

Company page: FleetPartners Group (FPR)

Pantoro cuts FY26 production guidance

[9:32 am] Pantoro delivered a sharp earnings uplift in H1 on the back of higher gold prices, but lowered full-year production guidance below its prior range.

Revenue up 56% to $238.6m

NPAT up 755% to $56.4m

FY26 gold production guidance cut to 86-92koz vs. prior guidance of the lower end of 100-110koz, a midpoint reduction of roughly 15%

Pantoro previously (22-Jan) tempered its FY26 production guidance to hit the lower end of 100-110koz, resulting in a 11% selloff on the day of the announcement.

Company page: Pantoro (PNR)

Westgold approves $145m expansion of Higginsville Processing Hub

[9:31 am] Westgold has taken FID on a capacity expansion at its Higginsville Processing Hub, lifting throughput from 1.6Mtpa to 2.6Mtpa and targeting a material uplift in Southern Goldfields gold production.

Committing $145m to expand the hub to 2.6Mtpa, which increases ore processing capacity in the Southern Goldfields by 62.5%

Expansion adds ~60kozpa in Southern Goldfields gold production and cuts processing costs by 24% to $34/t

Pre-tax NPV of $1.4bn at A$4,905/oz gold and $2.7bn at spot (A$7,305/oz), with IRR of 43% at the base case rising to 140% at spot

Southern Goldfields production uplift expected from mid-FY28

Company page: Westgold Resources (WGX)

Woodside kicks off Trion Field drilling campaign in Gulf of Mexico

[9:29 am] Woodside has commenced drilling at the Trion Field in ultra-deep waters off Mexico, a key step toward first oil in 2028.

The campaign covers 24 subsea wells to be connected to the Tláloc floating production unit, which has nameplate capacity of ~100,000 barrels per day

Drilling is being conducted by Transocean's Deepwater Thalassa, which arrived in Mexican waters on March 5, with logistics operating out of the state of Tamaulipas

Trion reached FID in 2023 and is one of Mexico's most significant offshore developments, operated in partnership with PEMEX

First oil remains on track for 2028

Company page: Woodside Energy (WDS)

The Ides of March

[9:25 am] Mid-March has an uncanny record of marking moments that reshape markets and economies.

The dot-com bubble peaked on March 10, 2000, Bear Stearns collapsed March 16, 2008, COVID circuit breakers fired March 9, 2020 followed by the largest single-day drop since 1987 a week later, and SVB failed March 10, 2023

March 8, 2026 now joins the list: the Iran war triggered a 20% spike in oil prices, the latest in a pattern of mid-March shocks that have consistently wrong-footed investors

US energy stocks finish slightly lower

[9:21 am] The S&P 500 Energy sector (-0.43%) underperformed the broader index (+0.83%) but marked a rather muted move despite whipsawing oil prices. The Energy sector is pretty much unchanged in the last four sessions and up just 0.25% since the Iran conflict commenced on Friday, 27 February.

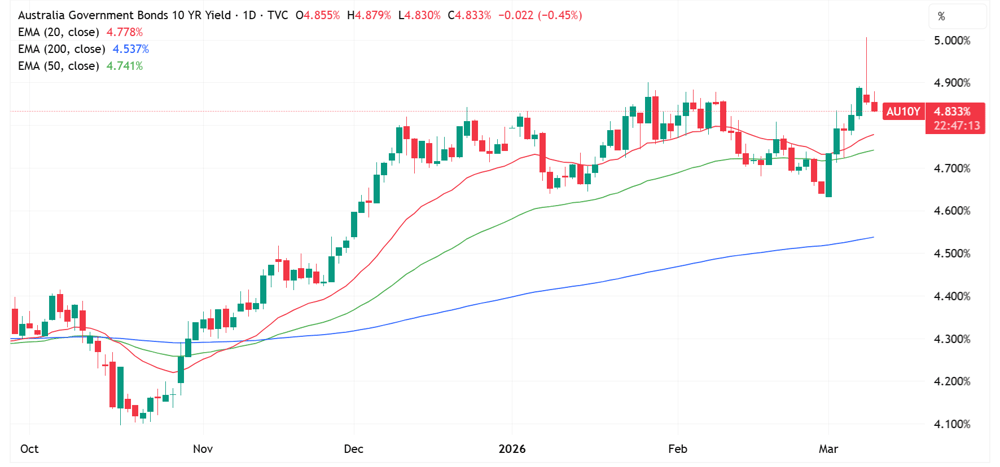

Massive yield reversal

[9:19 am] Things got pretty dark yesterday, with the Australian 10-year yield yield surging as much as 11 bps to 5.00%, the highest since July 2011.

Yields reversed sharply overnight, with the 10-year closing the session down 3 bps to 4.85%, and currently down another 2 bps in early trade to 4.83%.

Australia 10-year bond yield daily chart (Source: TradingView)

Energy shock forces markets to reprice ECB and BOE rate paths

[9:14 am] Soaring energy prices have flipped European rate expectations from cuts to hikes, with traders now fully pricing two ECB increases this year and central banks caught between inflation and growth risks.

Swaps now imply around 70% probability of two 25 bp ECB hikes this year, up from one move priced on Friday, with a first hike fully priced by July.

BOE rate-cut bets have reversed, with markets now pricing roughly 50% odds of a hike by year-end.

European natural gas rose as much as 30% on Monday, driving a European inflation expectations gauge to its highest close since July 2024, up 7bp to 2.23%.

Source: Bloomberg

Wall Street divided on US equity downside risks

[9:11 am] Major banks are split on how far US equities could fall, with Deutsche Bank and Goldman flagging historical context while JPMorgan and RBC point to still-elevated positioning and valuations.

Deutsche Bank argued that larger selloffs of >15% have historically required a sustained 50-100% oil price spike, a hawkish central bank response, or recession, noting risks are rising but not yet at levels seen in the 2022 turmoil or 1970s shock.

JPMorgan noted hedge fund leverage fell around 7 percentage points last week, a two standard deviation move, though it remains in the 97th percentile over the past five years, suggesting positioning is still stretched.

Goldman Sachs flagged ETF shorts jumped by the most since Liberation Day last week, the second largest in five years, while its US Panic Index spiked to 9.7 out of 10, which Goldman noted may be one of the few contrarian bullish signals in the current environment.

RBC Capital Markets said US equities remain vulnerable given still-elevated valuations, though it held its 2026 S&P 500 price target at 7,750, and noted 72% of non-energy analysts surveyed see broader EPS impact from higher oil and gas prices as minimal, with risks concentrated in staples and materials.

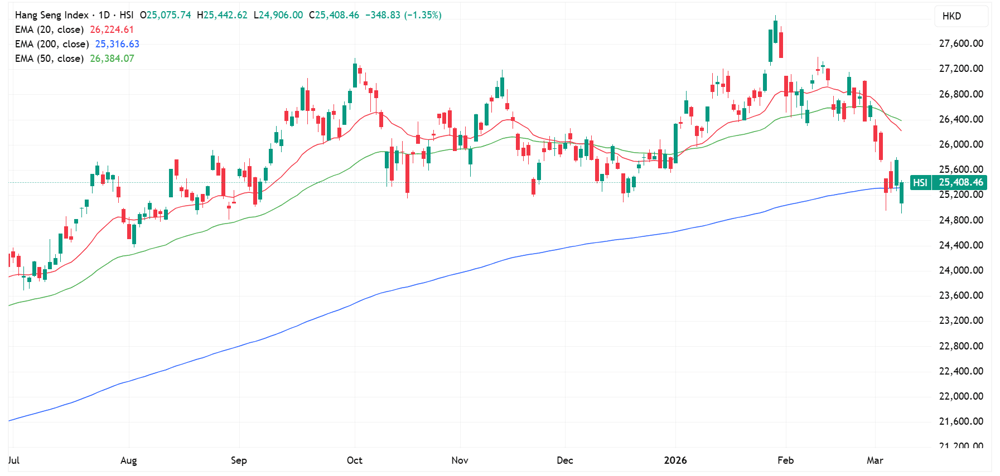

Mainland investors snap up record HK$37.2bn in Hong Kong shares

[9:10 am] Mainland Chinese investors posted a record single-day buy through Stock Connect on Monday, according to Bloomberg.

Monday's HK$37.2bn inflow via Stock Connect topped the previous record of HK$35.9bn set in August 2024, bringing year-to-date net buying to HK$188.7bn, roughly 60% of the comparable period last year

The buying helped the Hang Seng Index pare a 3.3% intraday decline to close 1.35% lower, a notably resilient outcome on a day when a broader Asian equities gauge fell close to 4% on surging oil prices and Iran war concerns

Chinese stocks have underperformed regional peers including Japan and South Korea year-to-date, though Beijing's supportive policy stance for local markets and technology at the ongoing National People's Congress has provided a floor

The record inflow follows record outflows the prior week, a pattern consistent with historical precedent where extreme moves through Stock Connect are often quickly reversed

Hang Seng daily price chart (Source: TradingView)

Bessent flags potential un-sanctioning of Russian oil

[9:05 am] Treasury Secretary Scott Bessent said the US is actively considering removing sanctions on Russian crude, a day after Washington issued a 30-day waiver allowing stranded Russian barrels to continue flowing to India, with hundreds of millions of sanctioned barrels currently sitting on the water representing a potential near-term supply lever.

Source: Reuters

China's inflation spike masks fragile recovery

[9:01 am] Lunar New Year holiday spending pushed China's CPI to a 37-month high in February, but analysts are sceptical the momentum will hold.

CPI rose 1.3% year-on-year in February, beating the 0.8% consensus estimate, with monthly CPI up 1.0% versus 0.5% expected

Core CPI accelerated to 1.8% from 0.8% in January

Holiday distortions drove the beat, with flight ticket prices rose 29.1% year-on-year and gold jewellery surged 76.6%, suggesting the print flatters underlying demand conditions

PPI deflation eased to -0.9% year-on-year (vs. -1.4% prior, -1.2% expected), the smallest drop since July 2024, with crude oil price rises and computing-related demand cited as partial offsets

Capital Economics warns any inflationary pickup will reverse once Middle East tensions ease, noting China's five-year plan disappointed on domestic demand stimulus

PBOC easing remains on the table, with ING flagging room for a rate cut in Q2 given a soft start to 2026, and analysts noting the oil shock alone is unlikely to derail further monetary loosening

Source: Reuters

Oil's epic reversal

[9:01 am] This one's for the history books. Here are the key price points:

WTI crude opened the Monday session 7.3% higher to US$98 a barrel

Prices rallied as much as 30.9% in early trade to a high of US$119.48

This would've marked the largest daily gain on record, excluding the 21 March 2020 bounce (where prices went to zero/negative). All the other pandemic-related bounces were around 18-24%

Crude faded aggressively amid Trump's remarks about the war being "very complete, pretty much"

Crude finished the session down 6.7% to US$85 a barrel

This represents a 28.8% decline from session highs

Excluding the 20-21 March 2020 decline, this marks the largest intraday decline dating back to the 80s

G7 signals strategic reserve release but stops short of pulling trigger

[8:52 am] G7 finance ministers met virtually to coordinate on Middle East energy disruptions but stopped short of releasing strategic oil reserves, signalling readiness without action.

Brent crude surged as much as 29% on Monday before paring gains after news of the G7 discussion emerged, with Saudi Arabia, Kuwait, Iraq and the UAE all cutting output amid the Hormuz closure.

The IEA's Fatih Birol described the Hormuz situation as presenting "significant and growing" risks to oil markets, a notable shift from his comments just days earlier on Friday when he emphasised how well-supplied the market was.

French Finance Minister Lescure said the group is "not there yet" on a stockpile release, with Portugal's minister adding there is no supply problem currently, only a price problem.

Coordinated strategic reserve releases have occurred only five times historically, including twice following Russia's Ukraine invasion in 2022, underscoring the significance of the tool being on the table.

Germany signalled openness to a release "at the right time" but stressed G7 coordination is essential before any action, with Spain flagging concern about potential inflationary pass-through to consumers.

Source: Bloomberg

The big overnight story: Trump says "the war is very complete"

[8:47 am] The main catalyst that drove a sharp reversal for US indices and oil prices was this phone interview with CBS News. Trump claimed the US has effectively destroyed Iran's military capacity, though mixed signals from the Pentagon suggest the conflict is far from resolved.

Trump told CBS News "I think the war is very complete, pretty much," and Iran has "nothing left" militarily after the US struck over 3,000 Iranian targets in the first week of operations, saying the campaign is "very far ahead of schedule" on his initial one-month timeline.

Trump said the US "could do a lot" with the Strait of Hormuz and hinted at "taking it over."

Iran's new supreme leader is Ayatollah Mojtaba Khamenei, who replaced his father following a late Sunday announcement, with Trump declining to engage and saying he has "someone else in mind" to lead the country.

The Pentagon posted "We have Only Just Begun to Fight" and "no mercy" on the same afternoon Trump declared the war near complete, raising questions about whether US military objectives have been fully defined or agreed upon.

Good morning!

[8:32 am] ASX 200 futures are up 184 pts (+2.14%) as of 8:30 am AEDT.

The overnight session in a nutshell:

Major US benchmarks reversed earlier declines, closing the session higher and near best levels

WTI marked one of its largest intraday moves on record, closing the session 6.7% lower to US$85.07, marking a 28.8% decline from session highs of US$119.48

Trump said the Iran war was "very complete, pretty much" and considering taking control of the Strait of Hormuz

Bond yields and VIX both down sharply from session highs, while commodity prices reversed from session lows