ASX 200 Live Today - Thursday, 9th April

The S&P/ASX 200 is set to slip after a massive rally on Wednesday. Here are today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Thursday, April 9. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

ASX 200 flat, US futures edge lower

[2:15 pm] A relatively uneventful day for markets, where the ASX 200 quickly reversed an initial 0.52% dip to spend most of the session trading around breakeven.

Tech (-6.4%) reversed almost the entirety of yesterday's 7.3% rally

Discretionary (-1.0%), Healthcare (-0.78%) and Materials (-0.70%) pulled back, but still holding onto most of Wednesday's gains

Energy (+2.3%) bounced after Brent staged a sizeable turnaround overnight, closing the session ~6% lower (vs. session lows of -12.6%)

Staples (+1.0%) edging higher, on the cusp of trading back at Feb-26 levels and within 2% of breaking out to the highest since Apr-24

Financials (+0.7%) have been unstoppable, up five of the last six sessions, gaining 7.7% in total and within ~1% of all-time highs

Breadth was slightly negative, with 115 constituents (58%) trading lower, but gains from Banks, Energy and Staples more than offset the weakness from Tech, Retailers and Miners. Overall, the market remains in a tricky spot. The rally appears driven by ceasefire hopes, likely further driven by short covering and extreme bearish sentiment. That said, no oil or gas tankers have transited the Strait of Hormuz since the ceasefire was announced, and physical oil prices continue to trade near record highs of around US$144/bbl, according to Bloomberg. S&P 500 and Nasdaq futures are currently off 0.2% and 0.24% respectively. Expect another volatile, headline-driven session overnight. Catch you all tomorrow.

Lynas climbs to highest since 2011

[1:56 pm] Lynas has been one of the most durable large cap stocks in recent weeks, having suffered a drawdown of no more than 10% and now back at YTD highs and trading at levels not seen since 2011.

I think one of the key catalysts behind this relative strength was the company's 10 March 2026 announcement, in which longstanding partner Japan Australia Rare Earths (JARE) revised its offtake agreement with Lynas, committing to purchase 5,000 tonnes of NdPr per annum at a market-linked floor price of US$110/kg.

To add some perspective, NdPr was trading at US$111.5/kg in late March, compared to US$74 in December 2025 and US$56 in December 2024. Lynas produced 3,407 tonnes of NdPr in 1H26, so the contract is significant in terms price protection and volume coverage. JARE also agreed to purchase 50% of all heavy rare earths produced by Lynas, at pricing terms that Lynas describes as representing no opportunity loss.

Commodities set up for a breakout of epic proportions

[1:40 pm] The Bloomberg Commodity Index represents a basket of 23 physical commodity futures across energy, metals, agriculture and livestock. Its formed a massive 12-year cup and handle, and currently trying to breakout to fresh all-time highs. Given the backdrop surrounding energy, fertilisers and agriculture, will it break right through it?

Bloomberg Commodity Index Futures monthly chart (Source: TradingView)

EOS ordered to pay $4m penalty for continuous disclosure breach

[1:34 pm] ASIC secured a Federal Court ruling against Electro Optic Systems for failing to disclose a material revenue downgrade for 14 weeks.

EOS was ordered to pay a $4m penalty after the Federal Court found it breached continuous disclosure requirements under the Corporations Act

By 25 July 2022, EOS knew its 2022 revenue was likely to come in around $164m (plus a possible additional $27m), well below its prior guidance of $212.3m or above, but did not correct this until 31 October 2022

The gap between actual expected revenue and guided revenue represented a downgrade of roughly 23% at the midpoint, a material miss that was withheld from the market for approximately 14 weeks

The penalty was accepted by Justice Jackman as sufficient to achieve both specific and general deterrence given EOS's size and financial resources

ASIC has separately commenced proceedings against former CEO and Director Dr Ben Greene for alleged breaches of directors' duties, meaning legal risk for the company is not yet fully resolved

Company page: Electro Optic Systems (EOS)

Software and tech names on the backfoot

[12:35 pm] The below table observes the S&P/ASX 200 stocks with the largest declines from the open price.

Tech stocks experienced a strong bounce on Wednesday, only to be aggressively sold down today. A name like Wisetech opened 3.9% lower, now down 10.3%. Other sectors like defence and travel also experiencing some intraday weakness.

Ticker | Company | % Chg vs. Open | Price |

|---|---|---|---|

WTC | Wisetech | -6.87% | $38.80 |

ZIP | Zip | -6.21% | $1.78 |

ORA | Orora | -5.00% | $1.62 |

EOS | Electro Optic Systems | -4.65% | $9.43 |

VGN | Virgin Australia | -4.65% | $2.46 |

XRO | Xero | -3.83% | $73.83 |

GDG | Generation Development Group | -3.66% | $4.21 |

TNE | Technology One | -3.64% | $27.50 |

REG | Regis Healthcare | -2.97% | $6.21 |

LLC | Lendlease Group | -2.88% | $3.21 |

Bendigo Bank's 3Q26 result takeaways

[12:33 pm] UBS says Bendigo Bank's 3Q26 trading update was a strong print, with cash NPAT and costs both beating consensus, NIM expanding 6bps quarter-on-quarter, and two new strategic technology partnerships announced alongside a restructuring program targeting $65–75m in run-rate savings by FY28.

Here are the key takeaways from UBS' first take of the result:

Cash NPAT of $138m, up 7.6% above the 1H26 quarterly average (12% beat to consensus)

NII of $433.2m, down 0.4% quarter-on-quarter, as subdued lending growth was largely offset by deposit pricing and mix improvements

NIM up 6bps quarter-on-quarter, also benefiting from a slight replicating portfolio uplift

Operating expenses of $305.1m, down 4.1% on the 1H26 quarterly average, driven by lower average FTE and fewer working days

Credit expense of $2.1m, well below consensus of $5.2m, with management cautious on geopolitical risks

What's catching a bid today

[12:30 pm] The below table observes the S&P/ASX 200 stocks with the largest moves from the open price.

Bendigo Bank's 3Q26 earnings has clearly been well received, while a broad basket of gold names are also catching a bid.

Ticker | Company | % Chg vs. Open | Price |

|---|---|---|---|

BEN | Bendigo & Adelaide Bank | 6.06% | $11.46 |

ALK | Alkane Resources | 5.92% | $1.79 |

SGM | Sims | 5.56% | $20.41 |

ASX | ASX | 5.37% | $56.89 |

CMM | Capricorn Metals | 5.09% | $12.17 |

4DX | 4DMedical | 4.08% | $6.38 |

OBM | Ora Banda Mining | 3.70% | $1.32 |

RRL | Regis Resources | 3.33% | $7.44 |

VAU | Vault Minerals | 3.30% | $4.55 |

BOQ | Bank Of Queensland | 3.12% | $7.45 |

Australian household spending holds up in February but oil shock clouds the outlook

[11:36 am] Consumer momentum was solid heading into the conflict period, but UBS expects the fuel price surge to show up in coming months, with two more RBA rate hikes now the base case.

February Household Spending Indicator (HSI) rose 0.3% month-on-month (UBS and market both expected 0.2%), up 4.6% year-on-year. This is broadly in line with the long-run average of 4.7% year-on-year and well above the pre-pandemic pace of 3.4%

The 3-month rolling trend slowed to 0.9% quarter-on-quarter in February, down from 1.5-2.0% since November 2025. UBS views this as a normalisation following the Black Friday and end-of-year sales pull-forward, with momentum now back near its long-run average of around 1% quarter-on-quarter

Car sales rose 16% month-on-month to 105k in March, though still 3.3% below year-ago levels, while electric vehicles surged to nearly 15% of all cars sold. The data captures deliveries not orders, so further strength is possible in coming months

The global oil shock is beginning to show up in hard data, with manufacturing input cost PMIs spiked 5 points month-on-month in March, the fastest increase since 2009, with Australian flash PMI data corroborating the trend. Fuel spending is expected to show up prominently in the March HSI release

UBS expects the RBA to hike rates 25bps in both May and August 2026, taking the cash rate to a new cycle peak of 4.60%, on the basis that Q2 CPI will remain too high. This is a notable hawkish call given market scepticism around further tightening

UBS notes households enter this period with large savings buffers and low unemployment, providing some capacity to absorb a temporary inflation spike in nominal spending terms

Gold stocks give back some gains

[10:53 am] The All Ords Gold Index is down 2.8% after gold prices faded a massive 3.3% rally overnight to close just ~0.3% higher.

Gold miners experienced a massive 8.8% rally on Wednesday, and up ~30% since the 24 March low.

All Ords Gold Index daily chart (Source: TradingView)

Ticker | Company | % Chg | Price |

|---|---|---|---|

BC8 | Black Cat Syndicate | -6.39% | $1.14 |

MEK | Meeka Metals | -5.41% | $0.18 |

GMD | Genesis Minerals | -5.06% | $6.29 |

CYL | Catalyst Metals | -4.89% | $6.62 |

OBM | Ora Banda Mining | -4.75% | $1.26 |

PRU | Perseus Mining | -3.71% | $5.45 |

EVN | Evolution Mining | -3.62% | $13.58 |

EMR | Emerald Resources | -3.44% | $6.04 |

RMS | Ramelius Resources | -3.41% | $3.96 |

CMM | Capricorn Metals | -3.18% | $11.86 |

RSG | Resolute Mining | -2.99% | $1.46 |

WGX | Westgold Resources | -2.80% | $6.60 |

NEM | Newmont | -2.78% | $166.68 |

BMR | Ballymore Resources | -2.78% | $0.18 |

PNR | Pantoro Gold | -2.56% | $3.81 |

VAU | Vault Minerals | -2.42% | $4.43 |

SBM | St. Barbara | -1.87% | $0.68 |

RRL | Regis Resources | -1.70% | $7.25 |

NST | Northern Star Resources | -1.21% | $23.64 |

BGL | Bellevue Gold | -1.08% | $1.84 |

Analysts' take on the ASX

[10:47 am] ASX delivered a stronger-than-expected Q3 result on Wednesday, with elevated market volatility driving a sharp uplift in cash equities and derivatives trading that more than offset persistent weakness in listings and capital raisings. Brokers broadly upgraded near-term earnings estimates and viewed the result as evidence of ASX's defensive earnings profile during volatile periods, though caution remained on the medium-term outlook given ongoing cost pressures, regulatory remediation, and leadership transition uncertainty.

JPMorgan retained Overweight, maintained target at $59.00.

Volatility drove standout trading across core franchises, with derivatives strength more than offsetting weaker listings, and the defensive earnings profile remained central to conviction despite ongoing regulatory and cost concerns.

UBS retained Neutral, raised target from $58.40 to $58.85.

March activity was exceptionally strong, with futures momentum reflecting heightened hedging demand and equity turnover benefiting from higher velocity, though near-term upgrades were tempered by likely normalisation and the leadership change limiting broader optimism.

Goldman Sachs retained Neutral, maintained target at $61.00.

Revenue conditions remained healthy outside primary markets, with rate uncertainty supporting futures participation and clearing trends improving alongside heavier cash trading, though lower margin balances and persistent expense caution tempered the earnings uplift.

Analysts' take on Regis Resources

[10:44 am] Regis Resources delivered a steady Q3 production result on Wednesday, broadly in line with expectations, with output from Duketon and Tropicana keeping the company on track to meet (and potentially beat the top end) of its full year guidance.

JPMorgan retained Neutral, maintained target at $7.00. Cash came in better than expected but may have been flattered by timing effects, diesel remains the key unresolved risk, and a limited growth profile versus peers kept conviction restrained.

Macquarie retained Outperform, maintained target at $9.70.

Steady operational delivery across assets and guidance reiteration reinforced execution confidence, with fuel contracts providing near-term comfort, though full cost detail remains the missing piece before a cleaner read on the outlook.

Analysts' take on Magellan

[10:42 am] Magellan's Q3 FUM update on Wednesday disappointed, with net outflows across both retail and institutional channels coming in worse than expected, compounding weakness from softer markets and ongoing underperformance in the flagship global equities strategy. Analysts flagged continued asset mix deterioration, with higher-margin retail outflows a key earnings headwind. While the Barrenjoey transaction drew mixed views, with some seeing strategic value and others citing limited disclosure and execution risk.

JPMorgan downgraded to Underweight, maintained target of $8.50. Disappointing flows across all channels, margin concerns from retail mix deterioration, and a less supportive market backdrop drove the downgrade.

Morgans maintained Buy, lowered target from $12.43 to $11.99. Despite a soft quarter, FUM is seen as broadly stabilising with Vinva a bright spot and the balance sheet supporting a constructive outlook.

Macquarie maintained Underperform, lowered target from $8.65 to $8.50. Worse-than-expected outflows, underperforming flagship funds, and downside earnings risk keep the cautious stance intact.

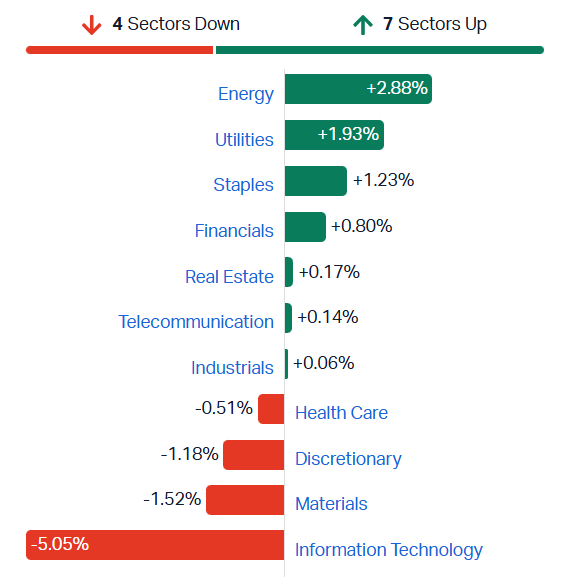

ASX 200 flat, Energy and banks offset Tech and resource weakness

[10:30 am] ASX 200 reversed a 0.5% decline in early trade, now trading around breakeven. Pretty much a 'opposite day' where big winners from Wednesday (Tech +7.3%, Materials +4.4%) are giving back their gains, and losers (Energy -7.1%, Utilities -4.1%) are bouncing.

The banks just keep going, up another 1.1% today. The S&P/ASX 200 Banks Index has now gained 8.4% over the last six sessions and within ~2% of all-time highs. CBA in particular has had no trouble defying gravity, pushing back to a nine-month high while trading at 28x earnings.

ASX 200 sectors (Source: Market Index)

Top ASX 200 gainers

[10:10 am] Bendigo Bank is trading sharply higher off the back of its Q3 update, while Energy stocks are bouncing after falling ~7% on Wednesday.

Ticker | Company | % Chg | Price |

|---|---|---|---|

BEN | Bendigo & Adelaide Bank | 5.26% | $11.01 |

ALD | Ampol | 4.51% | $33.57 |

VEA | Viva Energy Group | 4.13% | $2.52 |

WDS | Woodside Energy Group | 3.49% | $33.18 |

YAL | Yancoal | 2.54% | $7.68 |

STO | Santos | 2.13% | $7.93 |

BPT | Beach Energy | 2.07% | $1.23 |

ASX | ASX | 1.97% | $54.94 |

SNZ | Summerset Group | 1.89% | $7.55 |

4DX | 4DMedical | 1.79% | $6.24 |

Top ASX 200 losers

[10:10 am] Orora gapped sharply lower after downgrading its FY26 guidance, while yesterday's big winners (tech and growth) are trading broadly lower.

Ticker | Company | % Chg | Price |

|---|---|---|---|

ORA | Orora | -14.68% | $1.69 |

ZIP | Zip | -7.52% | $1.85 |

360 | Life360 | -6.79% | $20.19 |

WTC | Wisetech Global | -6.55% | $40.51 |

NWL | Netwealth Group | -6.50% | $22.44 |

XRO | Xero | -6.46% | $75.09 |

HUB | Hub24 | -5.76% | $85.76 |

GDG | Generation Development Group | -5.54% | $4.26 |

PNI | Pinnacle Investment Management Group | -5.06% | $14.44 |

OBM | Ora Banda | -4.53% | $1.27 |

Orora cuts Saverglass earnings guidance as Middle East conflict hits operations and demand

[9:50 am] Orora has materially downgraded FY26 Saverglass EBIT guidance, with both direct facility disruptions and indirect demand weakness weighing on the premium glass packaging business.

FY26 underlying Saverglass EBIT now expected at €63m-68m, down from prior guidance of broadly in line with FY25 EBIT of €79.2m. This represents a 17% downgrade at the midpoint

The Ras al Khaimah (RAK) facility in the UAE (representing approximately 15% of Saverglass production capacity) has been shifted to a closed-loop hot operation with no bottle production, as shipping and overland routes remain closed

Production is being redirected to the Acatlán facility in Mexico from late FY26

The direct €9m-€11m EBIT hit primarily relates to energy, staffing and fixed costs continuing with no revenue

The indirect €11m-€16m EBIT impact reflects weaker spirits demand and a sharper-than-expected mix shift toward lower-margin wine and champagne

Saverglass-owned inventory has increased at March 2026 reflecting softer customer offtake and increased competitive pressure, adding a working capital headwind alongside the earnings downgrade

Company page: Orora (ORA)

Sandfire Resources Q3 FY26 update: Guidance maintained but tracking to the lower half

[9:37 am] A softer March quarter at both MATSA and Motheo due to weather, maintenance and grade timing issues has pushed full-year production toward the bottom of guidance, though the balance sheet strengthened materially.

Group CuEq production of 34.5kt in Q3 FY26, bringing the nine-month total to 106.5kt

While full-year guidance of 149-165kt is unchanged but now expected to be within the lower half of the range (implying roughly 149-157kt)

MATSA produced 21.7kt CuEq in Q3, constrained by unusually high rainfall and unplanned maintenance, now expected to finish comfortably within the lower half of its 91-101kt guidance range

Motheo produced 12.8kt CuEq in Q3 as the transition into higher grade ore was delayed and now expected to finish at the bottom of its 58-64kt guidance range, though record annualised ore mining and processing rates of 6.5Mt and 6.1Mt respectively were achieved and a strong Q4 is anticipated as grade improves

The reduced throughput at MATSA is expected to have temporarily lifted unit costs above the 1H26 level of $87/t, though full-year unit costs at both operations are still expected to be materially aligned with guidance of $86/t (MATSA) and $44/t (Motheo)

Group capex guidance reduced by $15m to $225m, primarily due to a slight delay in Kalkaroo mobilisation and timing of the new MATSA tailings facility

Company page: Sandfire Resources (SFR)

Morgan Stanley cuts target prices on ASX Technology, Media, and Telecommunications stocks

[9:31 am] No rating changes but Morgan Stanley issued broad target price cuts across its TMT coverage, citing higher range of possible long-term earnings outcomes as AI rapidly reduces the time to build alternative solutions and software.

Airtasker retained Underweight; target cut from $0.23 to $0.20

CAR Group retained Overweight; target cut from $38 to $32

Catapult Sports retained Overweight; target cut from $6.50 to $5

hipages Group Holdings retained Equal-weight; target cut from $1 to $0.78

Megaport retained Equal-weight; target cut from $10 to $9

Nuix retained Overweight; target cut from $3.75 to $2.50

Pro Medicus retained Overweight; target cut from $275 to $200

PEXA Group retained Overweight; target cut from $17.50 to $15.50

REA Group retained Overweight; target cut from $250 to $230

SEEK retained Overweight; target cut from $28 to $21

Technology One retained Overweight; target cut from $34 to $32

Tyro Payments retained Underweight; target cut from $0.90 to $0.70

WiseTech Global retained Overweight; target cut from $100 to $70

Xero retained Overweight; target cut from $225 to $130

Bendigo Bank Q3 update: Earnings growth and major outsourcing partnerships flagged

[9:29 am] Bendigo Bank delivered steady earnings growth in Q3 while announcing two significant outsourcing partnerships that will reshape its cost base but require meaningful upfront investment.

NPAT up 13% to $137.9m

Net interest income up 4.0% to $433.2m,

NIM up 6 bps quarter-on-quarter to 1.98%

BEN has entered a seven-year IT services partnership with Infosys

Also entered a six-year business operations partnership with Genpact, following the Google partnership announced in November

The partnerships are expected to deliver an annual run-rate expense benefit of $65-75m by FY28, but will require upfront transition costs of $85-95m, the majority falling in FY27

Workforce reductions are flagged in technology and business operations teams as a direct consequence of the outsourcing arrangements

Company page: Bendigo & Adelaide Bank (BEN)

Alkane Resources Q1 2026 update

[9:26 am] Alkane delivered a solid March quarter with production tracking to full-year guidance and a rapidly strengthening cash position underpinned by elevated gold prices.

Group production of 45,776 AuEq oz in Q1, including 44,669oz of gold and 377 tonnes of antimony

FY26 guidance of 160,000-175,000 AuEq oz at AISC of $2,600-$2,900/AuEq oz remains unchanged

Cash, bullion and listed investments of $374m at quarter end, up $128m from the prior quarter

8,700oz of gold hedging was filled during the quarter and $15m in tax instalments were made, yet the cash balance still grew by $128m

Diesel supply disruptions are not a concern: Alkane noted diesel represents a small portion of total costs given three underground mines draw power from grid suppliers in Australia and Sweden

Company page: Alkane Resources (ALK)

West African Resources Q1 2026 production update

[9:24 am] WAF delivered 107,728 ounces in Q1, tracking comfortably within full-year guidance, with Kiaka emerging as the dominant production centre and gold sold at near-record realised prices.

Group gold production of 107,728 oz and gold sales of 104,145 oz at a realised price of US$4,945/oz

On track to meet 2026 annual guidance of 430,000-490,000 oz, with Q1 representing roughly 23% of the midpoint (460,000 oz)

Kiaka contributed 65,704 oz (61% of group output) at a realised price of US$4,922/oz, with gold production up 6% quarter-on-quarter driven by an 8% increase in mill throughput

Sanbrado produced 42,024oz, down 15% quarter-on-quarter due to a 12% lower mill grade from the M1 South underground, though this was flagged as planned — mined ounces from M1 South are expected to increase over the remaining three quarters as additional stoping areas open

WAF continues confidential discussions with the Burkina Faso government (via SOPAMIB) regarding the State acquiring an additional equity interest in Kiaka SA beyond its current 15%

Company page: West African Resources (WAF)

Transurban March quarter traffic update: Melbourne and North America lead growth

[9:18 am] Transurban delivered solid traffic growth across most markets in the March quarter, with West Gate Tunnel's contribution and North America ramp-up the key highlights.

Melbourne ADT (average daily traffic) up 3.8% to 866k transactions, driven by the West Gate Tunnel opening (14 December 2025) and strong large vehicle growth of 17.1% on CityLink

North America ADT up 7.9% to 164k trips, with the 495 NEXT ramp-up the primary driver, with 495 Express Lanes grew 17.2% and 95 Express Lanes grew 4.5%

Brisbane ADT up 5.2% to 474k trips, though underlying growth was a more modest 0.7% after stripping out the favourable base effect from Tropical Cyclone Alfred in the prior corresponding period

Sydney ADT up just 0.6% to 1,032k trips, weighed down by Warringah Freeway construction disruptions. The project is expected to open by end of 2026, with widened M7 sections progressively opening in the June quarter

Transurban flagged it is monitoring the geopolitical and macro environment, noting resilience from more than 90% of revenue being CPI-linked or carrying fixed escalations

Company page: Transurban (TCL)

Overnight price action: Energy stocks and gold

[9:16 am] The S&P 500 Energy sector dipped as much as 6.6% overnight but finished the session down just 3.5%, marking a strong bounce off the 50-day moving average. This perhaps marks continued Israeli military action across Lebanon and the lack of vessel activity moving through the Strait of Hormuz. It'll be interesting to see how the local energy sector performs, given the S&P/ASX 200 Energy Index tumbled 7.1% on Wednesday, with Woodside tanking 10.4%.

S&P 500 SPDR Energy ETF daily chart (Source: TradingView)

Gold also staged a rather interesting reversal, rallying as much as 3.3% to US$4,857 but closing the session up just 0.3% to US$4,699. Though gold equities didn't seem to mind too much, with NYSE-listed Newmont shares still up 3.0%.

Gold price chart (Source: TradingView)

Hormuz remains effectively closed despite ceasefire

[9:02 am] Just three ships left the Persian Gulf on Wednesday vs. a normal daily rate of around 135, with over 800 vessels stranded and shipowners unwilling to move without clearer safety guarantees.

Only three ships were observed departing the region on Wednesday, with Iran subsequently reporting tanker passage remains blocked following attacks on Lebanon. This serves as a stark reminder that the ceasefire has not reopened the world's most critical oil chokepoint

More than 800 freighters are stuck inside the Gulf, including 426 crude oil and clean fuel tankers, 34 LPG carriers and 19 LNG vessels

Iran and the US appear to have fundamentally different interpretations of the ceasefire terms — Iran says passage requires coordination with its armed forces within "technical limitations," while Trump declared a "complete, immediate, and safe opening," a disconnect creating significant uncertainty for owners and insurers

Iran has been charging tolls of up to US$2 million per transit for some carriers, and a crew on one vessel reported receiving a warning that navigation still requires Iranian permission

Major shipping groups including Maersk, Hapag-Lloyd and Bimco are all maintaining caution

No loaded LNG carrier has successfully transited Hormuz since the war began, with roughly 20% of global LNG traffic normally passing through the strait, a prolonged closure has significant implications for energy markets beyond oil

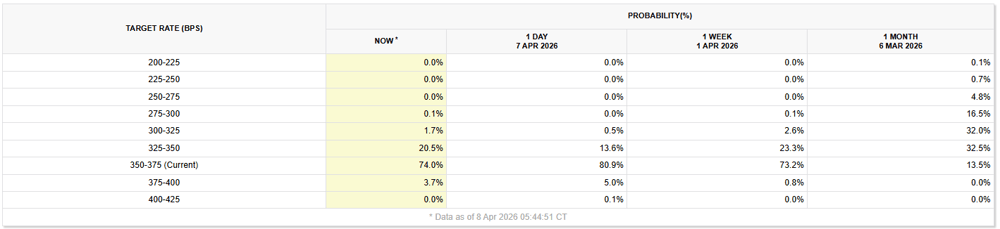

Fed rate odds largely unchanged

[9:00 am] The ceasefire announcement has tipped the likelihood of a 25 bp rate cut by year end slightly higher, from 13.6% to 20.5%.

Target rate probabilities for 9-Dec-26 Fed meeting (Source: CME Fedwatch Tool)

Fed minutes reveal growing rate hike risk

[8:57 am] March FOMC minutes show a divided Fed wrestling with stagflationary risks, with a growing cohort of officials flagging the possibility of rate increases if inflation remains elevated.

The Fed held rates at 3.50-3.75% at the March meeting, with policymakers signalling one cut expected in 2026 — though futures markets are pricing no cuts at all this year

A growing number of officials pushed for "two-sided" rate language in the post-meeting statement, explicitly acknowledging rate hikes as a possibility — the group using the word "some" is larger than the "several" flagged in January minutes, a meaningful shift in the Fed's counting lexicon

The "vast majority" of officials believe it may take longer than previously expected to return inflation to the 2% target, reflecting the persistence of energy-driven price pressures

Most officials see labour market risks skewed to the downside, noting the economy is in a state of "low rates of net job creation" and vulnerable to adverse shocks, setting up a classic stagflationary dilemma for the Fed

Officials warned that with inflation already running above target for five years, longer-term inflation expectations could become more sensitive to energy price increases

Meta debuts closed AI model Muse Spark in strategic pivot

[8:52 am] Meta launched its first model from its new superintelligence lab, marking a significant shift away from its open-source roots and a direct push to compete with OpenAI, Anthropic and Google.

Muse Spark is Meta's first closed model, developed over nine months by Meta Superintelligence Labs under Chief AI Officer Alexandr Wang

The lab was built on the back of a $14bn investment into Scale AI last year, with Zuckerberg committing tens of billions more on data centre infrastructure after feeling Meta had fallen behind rivals

Meta acknowledged Muse Spark is currently less capable than ChatGPT, Claude and Gemini, describing it as "an early data point on our trajectory" with larger models in development

The model was trained using third-party open-source models including Alibaba's Qwen — a potentially sensitive detail given US policymaker concerns around Chinese AI and national security risks

Meta shares rose 6.5% following the announcement

Delta beats on Q1 earnings but fuel costs cloud the outlook

[8:49 am] An interesting quarterly from Delta, which beat expectations but missed on guidance. The airline is pulling back on capacity growth as a historic jet fuel spike weighs heavily on the near-term outlook. Perhaps a good read-through for local names like Qantas and Virgin?

Adjusted EPS of $0.64 vs. $0.57 ests (12% beat)

Revenue of $14.2bn vs. $14.0bn ests (1% beat)

Q2 adjusted EPS guidance of $1.00-$1.50 (midpoint $1.25) vs. $1.41 ests (11% miss)

Delta expects $1bn in pretax profit but flagged a $2bn higher fuel bill this quarter

All-in fuel costs guided at $4.30 per gallon in Q2 as jet fuel prices in major US cities were up nearly 88% since late February through early April

Capacity cut 3% in Q1 and guided flat year-on-year in Q2 — less capacity typically supports higher airfares, which are already rising

Delta's refinery near Philadelphia is a key differentiator, expected to contribute a $300m benefit in Q2 and partially offset the fuel shock

Physical oil premiums signal the market remains severely undersupplied despite ceasefire

[8:44 am] North Sea crude is trading at record premiums to futures, highlighting a stark disconnect between paper markets and real-world supply availability.

US crude delivered to Europe sold at more than US$20 above the Dated Brent benchmark, roughly double the previous record set just weeks ago, with multiple grades trading at similar premiums

Dated Brent hit a record above US$140 per barrel on Tuesday vs. US$109 for Brent futures

A ~US$30+ gap reflecting the extreme premium traders are paying for immediate physical delivery

The Strait of Hormuz remains largely blocked despite the ceasefire, with sporadic fighting continuing across the Middle East and no meaningful return of normal tanker flows

Four different North Sea crude grades were bid above US$20 over Dated Brent on Wednesday, with a further eight unanswered bids, suggesting demand for physical barrels is far outpacing available supply

The record physical premiums are a key signal for investors: futures prices have sold off sharply on ceasefire optimism, but the underlying supply disruption has not resolved, creating a potential divergence worth watching

Source: Bloomberg

Saudi Arabia's East-West pipeline holds firm despite drone strike

[8:43 am] Despite a drone strike on one of its pumping stations, Saudi Arabia's key East-West pipeline continues to flow, offering some relief to an oil market already rattled by the Strait of Hormuz blockade.

Damage to the pipeline was limited and crude flows were uninterrupted, with oil exports from the Red Sea port of Yanbu unaffected — Saudi Aramco declined to comment

The pipeline is running at full capacity, moving close to 5 million barrels per day, roughly 70% of Saudi Arabia's pre-war export levels, by bypassing the largely closed Strait of Hormuz across 1,200 kilometres

The Strait of Hormuz remains largely blocked despite the ceasefire, with Iran's Fars news agency reporting tanker movement through the waterway was halted following Israeli attacks on Lebanon — shipowners are still assessing whether safe transit is possible

Hedge funds rush to cover shorts as Iran ceasefire sparks market squeeze

[8:41 am] Goldman Sachs reports hedge funds are closing bearish positions at the fastest pace since the pandemic rebound, fuelling a sharp equity rally.

Short-covering in US macro products (indexes and ETFs) is on track to match volumes seen in early 2020, with hedge fund short exposure having peaked at 12% of total gross exposure — the highest since the pandemic

The catalyst was Trump's announcement of a temporary ceasefire with Iran, which Goldman's John Flood described as "the offramp the market has been waiting for," with investors viewing it as the likely beginning of the end of the conflict

Major indexes rallied more than 2% overnight, the sharpest single-day gain since 31 March, driven in part by the mechanical bid from short-covering (borrowed shares being repurchased to close positions)

Goldman's trading desk expects near-term profit-taking in war beneficiaries such as energy, commodity chemicals and defence. Heavily shorted consumer discretionary and housing-linked stocks are seen as the most likely candidates for sustained covering

Flood flagged an "offensive phase" ahead as earnings season approaches, anticipating long-only managers and sovereign wealth funds to rotate back into pre-war leaders including memory-chip makers and semiconductor stocks

Source: Bloomberg

Ceasefire eases tanker risk but oil supply remains constrained

[9:39 am] Bank of America warns that while a two-week ceasefire may normalise shipping through the Strait of Hormuz, the structural tightness in oil markets remains firmly intact.

The ceasefire allows safe passage through the Strait of Hormuz, potentially relieving tanker traffic, but 11 million barrels per day of production remains shut in and reactivating those fields will take weeks to months

The 400 million barrel inventory build from 2H25, which had threatened to double in 1H26 and push oil into the low US$50s, has been fully wiped out within just five weeks of the conflict

Fundamentals have shifted materially as balances are tighter, mid-cycle oil prices are higher, geopolitical risk premiums have been validated, and global strategic petroleum reserve (SPR) refilling is expected to support future demand

BofA's base case is that oil stocks will still reverse course, but not fully, given the more constructive supply/demand backdrop

The ceasefire is explicitly short-lived, meaning any relief to supply is temporary and the underlying market tightening trend remains in place

Good morning!

[8:30 am] ASX 200 futures are down 22 pts (-0.24%) as of 8:30 am AEST. Here's the overnight session in a nutshell:

Massive rally across Asian, European and US markets, broadly in-line with what we experienced on Wednesday

S&P 500 (+2.51%) now up for six straight sessions, the longest winning streak since October 2025

Every ex-defensive/value sector rallied at least 2% on Wall Street, though ceasefire and Hormuz reopening remains volatile as Israel continues to strike Lebanon

Commodity prices remain highly volatile, with Brent closing 6.5% lower (vs. session lows of -12.6%) and gold pretty much flat despite rallying as much as 3.3%