ASX 200 Live Today - Thursday, 19th March

The S&P/ASX 200 is set to tumble and hit fresh year-to-date lows after a downbeat overnight session. Here are today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Thursday, March 19. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

ASX 200 lower as miners tank, defensives shine

[2:30 pm] ASX 200 down 1.53% and hovering near session lows. Big blowout for cyclicals, growth and miners, weighed by rising yields, weakening commodity prices and cost inflation.

Materials (-4.45%) now down almost 20% since 2-Mar-26, trading at the lowest since 22-Dec-25. Not a good time to be an energy/diesel hungry business.

It's even worse for gold, with the All Ords Gold Index down almost 30% since 2 March. When Russia invaded Ukraine in February 2022, gold miners managed to rally another ~12% by April 2022 but down ~40% seven months later (tightening global financial conditions, rising yields, energy security etc.)

Tech (-2.7%) is on the backfoot after global software stocks experienced a bounce in recent weeks. The local tech index is now ~2.4% away from recent lows

Real Estate (-2.6%) has been falling off a cliff, down around 18% since late December. Another causality of this rising yield environment. The Aussie 10-year

Utilities (+0.37%) and Staples (+0.33%) holding up relatively well. Its interesting to see how 28-30x super markets are acting as safe havens in today's session. Also odd how a name like Origin Energy (+0.60%) barely moves, despite how ~60% of its earnings come from LNG.

Energy (+4.6%) we've talked about how energy stocks tend to struggle to rally off of geopolitically driven moves. However, as oil prices continue to trend higher, and the energy supplies remain pressured, equities are reluctantly trading higher. Today was a massive session for refiners like Viva (+16.8%) and Ampol (+4.7%). They're starting to become our very own "critical" resource stock given ongoing diesel shortages

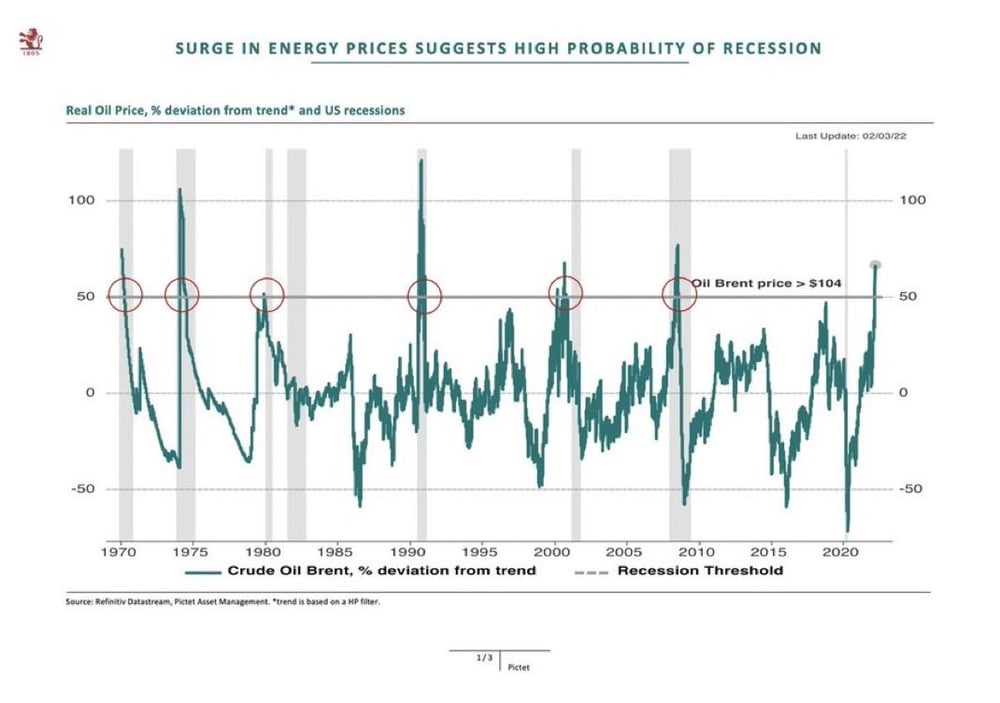

A fading of fears around Iran and energy supply disruptions would likely trigger a relief rally, but there's been no sign of de-escalation or improved tanker flows just yet. Markets are walking a dangerous tightrope as oil prices continue to climb. To close things out today, here's an interesting chart about historic energy price rallies and recessions.

CBA is ... breakeven?

[1:55 pm] It's pretty rough out there, but CBA is somehow clinging to breakeven after bouncing off a session low of -1.38%. Even with fuel prices crossing $2.50 a litre and the cost of just about everything else facing upward pressure, I guess we still need to pay our mortgages, right?

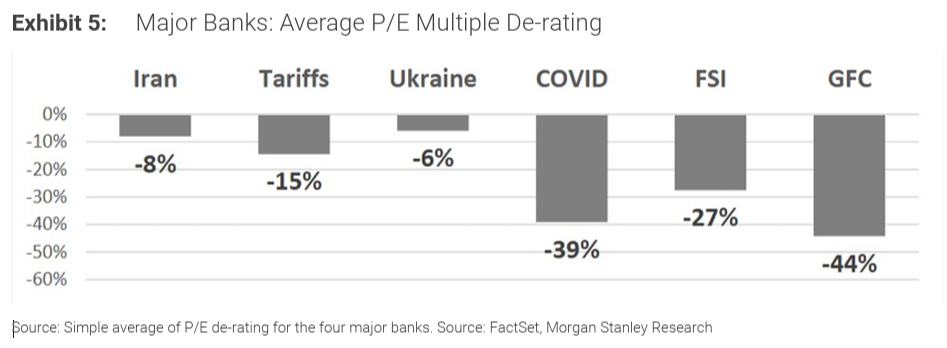

On a side note, here's an interesting chart from Morgan Stanley, which shows how bank valuations have de-rated from prior geopolitical/economic shocks.

UBS stress tests $100/bbl oil scenario

[1:46 pm] UBS has worked with over 165 analysts to stress test the impact of resetting oil to US$100 a barrel (and gas to US$15/mmbtu) for 2026-27, revealing significant divergence across markets, sectors and supply chains.

At the index level, Brazil and Mexico are the biggest beneficiaries with potential EPS upgrades of 15-50%, while broad-based cuts are expected across parts of Asia and EMEA, particularly Indonesia, India and South Africa

Energy is the clear sector winner, while airlines/transport face the most direct downside

Insurance, media, pharma, software/services and regulated utilities are largely indifferent to oil price moves

An additional 10% crude increase beyond US$100/bbl would hit South Africa, Taiwan and Thailand hardest in terms of further EPS cuts

Indirect macro risks are material: Philippines, Thailand and Poland face the greatest real GDP drag from a 10% crude price rise, while Thailand, Korea and Philippines are most exposed to inflation pass-through

Philippines and Korea EPS are seen as most vulnerable to the indirect GDP channel

SunRice flags FY26 revenue headwinds

[1:44 pm] SunRice Group has updated its FY26 outlook, warning that full year revenue is expected to be broadly in line with, or slightly below, the prior corresponding period, while still expecting NPAT growth.

Despite the revenue softness, management continues to expect NPAT growth in FY26, reflecting disciplined execution and a focus on margin management

Revenue pressure stems from strong competition in Pacific markets weighing on lower-margin volumes, and a smaller CY26 crop due to drier Riverina conditions and lower wholegrain mill-out rates from the CY25 crop

More recent headwinds include a sharp appreciation of the Australian dollar against the USD, negatively impacting the translation of foreign earnings, and Middle East conflict disrupting shipping routes and near-term sales in that market

Company page: Ricegrowers (SGLLV)

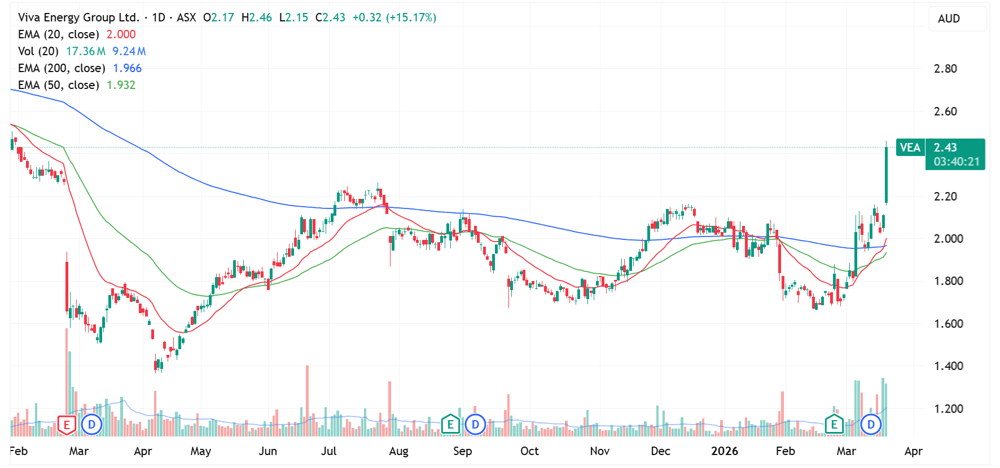

Viva Energy and Ampol in focus

[12:15 pm] Ampol and Viva Energy, which operate Australia's only two remaining refineries in Brisbane and Geelong respectively, might just be the country's most critical infrastructure right now, producing essential refined outputs like gasoline, diesel and jet fuel.

Viva was up around 23% from late February heading into yesterday's session, though that rally only brought the stock back to a three-month high.

Today, it's up a massive 16.3% to the highest since January 2025.

Viva Energy daily price chart (Source: TradingView)

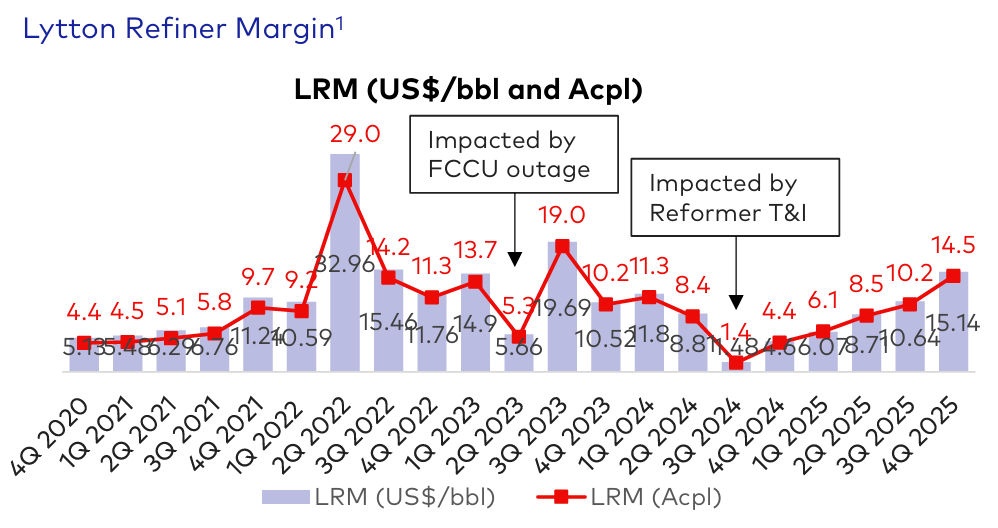

During Russia's invasion of Ukraine, Ampol's Lytton's refinery margins surged 215% from US$9.2 in Q1 2022 to US$29 the following quarter, with first-half EBITDA jumping 475% year-on-year to $475.6 million.

Ampol's Lytton Refinery key metrics (Source: Ampol's 2025 results presentation)

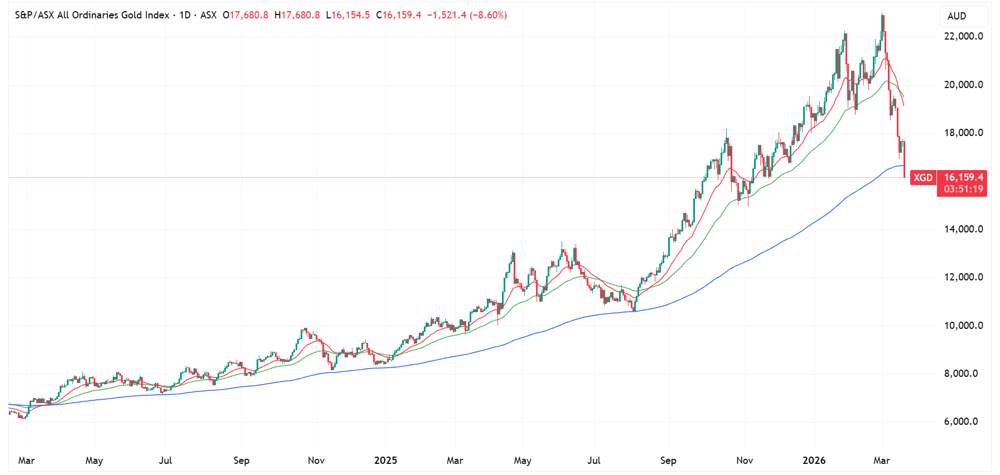

Gold stocks crushed

[12:10 pm] The All Ords Gold Index is down 8.4% today, and down almost 30% since its 2 March record high. What's incredible is that gold hasn't traded below the 200-day moving average for just over two years (since 4 March 2024 or 745 days). In some ways, this is mean reversion (I mean everything eventually comes back to the 200-day), but not when its a 30% drop over the course of ~2 weeks.

All Ords Gold daily price chart (Source: TradingView)

Sims rallies on analyst upgrades

[12:05 pm] I thought the price action for Sims was a little lacklustre on Wednesday, despite guiding to FY26 EBIT that was well-above market expectations.

Sims said it expects to deliver underlying FY26 EBIT of $350-400 million due to strong non-ferrous metals and DDR4 memory chip pricing. This was 23% ahead of consensus expectations of $305.5 million (at the midpoint).

We also noted (from yesterday's blog post):

1H26 result: Sims reported a stronger-than-expected 1H26 EBIT result, though statutory profit was weighed by tax and one offs. The stock dipped 4.0% on results day (17-Feb), likely due to i) shares had run ~49% since the Aug-25 result and ii) the lack of a formal second half guidance.

1H26 EBIT: Sims reported 1H26 underlying EBIT of $121.1m. Today's FY26 guidance of $350-400m (let's use the midpoint of $375m) implies a 2H26 EBIT of $254m.

UBS ests: After the 1H26 result, UBS said it expects 2H26 underlying EBIT of $177m (which is above consensus expectations of $143). Despite being more bullish than the average analyst, today's implied 2H26 EBIT guidance is still running 43% above UBS estimates

Despite the strong figures, Sims finished the session 9.8% higher, down from session highs of 16.8%. The stock is up 5.3% today, bucking the trend of the broader market. Analysts also seem pleased:

Jarden upgraded to Neutral from Underweight and raised its target from $19.50 to $21.50, saying the North America strategy was working across both metals and SLS, though SLS durability remained the key debate ahead of an upcoming Investor Day

RBC Capital Markets upgraded to Outperform from Sector Perform and raised its target from $23.00 to $25.50, expecting SLS momentum to continue on the back of memory tightness, though noted panic buying was likely to fade

Australia's unemployment rate rises to 4.3% in February

[12:01 pm] Australia's seasonally adjusted unemployment rate edged up to 4.3% in February vs. market expectations of no change at 4.1%.

Unemployment rose 0.2 percentage points to 4.3%, with the number of unemployed people growing by 35,000.

Employment grew by 49,000, though the composition was weak: part-time employment rose 79,000 while full-time employment fell 30,000, suggesting softening labour demand

Hours worked fell 0.2% as more people shifted to part-time hours, with the ABS noting fewer people leaving jobs to retire compared to a year ago

Participation rate rose 0.2 percentage points to 66.9%, meaning more people are entering or remaining in the labour force, which partly explains the higher unemployment rate

Source: ABS

Rough day for gold stocks

[11:15 am] Gold prices fell 3.73% to US$4,818.77 overnight, the lowest price since 6th February.

Ticker | Company | % Chg | Price |

|---|---|---|---|

NEM | Newmont | -5.09% | $147.32 |

BMR | Ballymore Resources | -5.56% | $0.17 |

EVN | Evolution Mining | -6.81% | $12.58 |

PRU | Perseus Mining | -6.95% | $4.82 |

SBM | St. Barbara | -7.17% | $0.56 |

CYL | Catalyst Metals | -7.21% | $6.18 |

RSG | Resolute Mining | -7.45% | $1.31 |

AMI | Aurelia Metals | -7.55% | $0.25 |

MEK | Meeka Metals | -7.65% | $0.16 |

EMR | Emerald Resources | -7.68% | $5.29 |

PNR | Pantoro Gold | -7.71% | $3.59 |

NST | Northern Star Resources | -7.92% | $19.29 |

WGX | Westgold Resources | -8.35% | $5.66 |

RMS | Ramelius Resources | -8.54% | $3.70 |

VAU | Vault Minerals | -8.77% | $4.22 |

BC8 | Black Cat Syndicate | -8.88% | $1.06 |

CMM | Capricorn Metals | -9.00% | $10.52 |

BGL | Bellevue Gold | -9.03% | $1.46 |

GMD | Genesis Minerals | -9.40% | $5.59 |

RRL | Regis Resources | -9.43% | $6.39 |

ALK | Alkane Resources | -10.09% | $1.45 |

OBM | Ora Banda Mining | -10.74% | $1.33 |

By Stephanie Gardner

Copper stocks plummet

[11:08 am] Key copper stocks are down 5-10% as copper prices dropped 5.02% overnight, closing at US$5.49.

Ticker | Company | % Chg | Price |

|---|---|---|---|

CPM | Cooper Metals | 1.96% | $0.05 |

TAR | Taruga Minerals | 0.00% | $0.02 |

BHP | Bhp Group | -3.26% | $48.46 |

SFR | Sandfire Resources | -5.29% | $15.84 |

MC2 | Marimaca Copper Corp | -5.79% | $8.88 |

CSC | Capstone Copper Corp | -6.75% | $10.64 |

AR1 | Austral Resources Australia | -6.98% | $0.08 |

CYM | Cyprium Metals | -7.59% | $0.37 |

HCH | Hot Chili | -8.01% | $1.32 |

HGO | Hillgrove Resources | -8.11% | $0.03 |

29M | 29Metals | -8.11% | $0.34 |

AIS | Aeris Resources | -9.20% | $0.40 |

FFM | Firefly Metals | -10.40% | $1.55 |

By Stephanie Gardner

Higher yields pressuring real estate stocks

[10:53 am] The S&P/ASX 200 Real Estate Index is down 2.17% as the Australian 10-year yield is creeping higher at 4.9%.

Ticker | Company | % Chg | Price |

|---|---|---|---|

NSR | National Storage REIT | 0.00% | $2.76 |

VCX | Vicinity Centres | -0.42% | $2.38 |

PXA | Pexa Group | -0.78% | $15.35 |

CHC | Charter Hall Group | -1.50% | $19.34 |

RGN | Region Group | -1.60% | $2.16 |

GPT | Gpt Group | -1.61% | $4.60 |

SGP | Stockland | -2.01% | $4.39 |

LLC | Lendlease Group | -2.01% | $3.41 |

HDN | Homeco Daily Needs REIT | -2.02% | $1.22 |

SCG | Scentre Group | -2.08% | $3.53 |

DXS | Dexus | -2.30% | $5.96 |

MGR | Mirvac Group | -2.43% | $1.81 |

GMG | Goodman Group | -2.70% | $25.57 |

BWP | Bwp Trust | -2.77% | $3.69 |

By Stephanie Gardner

Healthcare stocks dip

[10:44 am] The S&P/ASX 200 Healthcare Index is down 2.47%, lagging the broader market, which is down 1.51%. Interestingly, other defensives such as Staples (-0.14%) and Utilities (-0.04%) are outperforming on a relative basis.

Ticker | Company | % Chg | Price |

|---|---|---|---|

SHL | Sonic Healthcare | -0.82% | $20.62 |

4DX | 4Dmedical | -0.88% | $3.95 |

MSB | Mesoblast | -0.96% | $2.07 |

RHC | Ramsay Health Care | -1.20% | $40.46 |

EBO | Ebos Group | -1.74% | $18.07 |

RMD | Resmed | -1.92% | $32.25 |

SIG | Sigma Healthcare | -2.05% | $2.63 |

TLX | Telix Pharmaceuticals | -2.34% | $12.10 |

CSL | Csl | -2.86% | $134.06 |

ANN | Ansell | -2.86% | $28.91 |

COH | Cochlear | -2.91% | $167.42 |

FPH | Fisher & Paykel Healthcare Corporation | -3.29% | $30.88 |

PME | Pro Medicus | -3.48% | $120.95 |

By Stephanie Gardner

Tech stocks sharply lower

[10:37 am] The S&P/ASX 200 Technology Index is down 3.06% following a downbeat overnight session where the NASDAQ fell 1.46% as yields ticked higher and the VIX spiked to 25.08.

Ticker | Company | % Chg | Price |

|---|---|---|---|

NXT | Nextdc | -1.68% | $13.48 |

TNE | Technology One | -1.77% | $25.48 |

CDA | Codan | -2.21% | $34.04 |

PME | Pro Medicus | -3.50% | $120.93 |

XRO | Xero | -3.68% | $76.47 |

WTC | Wisetech Global | -4.24% | $42.71 |

360 | Life360 | -4.57% | $18.59 |

By Stephanie Gardner

Energy stocks surge higher

[10:25 am] The S&P/ASX 200 Energy Index is up 2.77% following an attack on a major LNG site in Qatar by Iran. Brent oil closed 5.9% higher at US$107.38 per barrel.

Ticker | Company | % Chg | Price |

|---|---|---|---|

VEA | Viva Energy Group | 8.53% | $2.29 |

ALD | Ampol | 3.84% | $32.73 |

WDS | Woodside Energy Group | 3.34% | $32.49 |

STO | Santos | 2.90% | $8.00 |

WHC | Whitehaven Coal | 2.86% | $9.00 |

YAL | Yancoal Australia | 2.79% | $7.73 |

NHC | New Hope Corporation | 2.67% | $5.39 |

BPT | Beach Energy | 1.62% | $1.26 |

NXG | Nexgen Energy | -2.02% | $16.70 |

DYL | Deep Yellow | -4.91% | $1.65 |

PDN | Paladin Energy | -5.00% | $10.82 |

By Stephanie Gardner

Top ASX 200 gainers and losers

[10:13 am] Here are today's top gainers and losers on the S&P/ASX 200.

Ticker | Company | % Chg | Price |

|---|---|---|---|

VEA | Viva Energy Group | 6.64% | $2.25 |

ALD | Ampol | 3.76% | $32.71 |

WDS | Woodside Energy Group | 3.66% | $32.59 |

STO | Santos | 3.22% | $8.02 |

YAL | Yancoal Australia | 3.19% | $7.76 |

MCY | Mercury NZ | 2.93% | $5.27 |

WHC | Whitehaven Coal | 2.86% | $9.00 |

EOS | Electro Optic Systems | 2.58% | $9.95 |

NHC | New Hope Corporation | 2.48% | $5.38 |

BPT | Beach Energy | 2.43% | $1.27 |

Ticker | Company | % Chg | Price |

|---|---|---|---|

IPX | Iperionx | -8.15% | $3.72 |

ALK | Alkane Resources | -8.05% | $1.49 |

WGX | Westgold Resources | -7.62% | $5.70 |

RRL | Regis Resources | -7.52% | $6.52 |

BGL | Bellevue Gold | -7.48% | $1.49 |

GMD | Genesis Minerals | -7.46% | $5.71 |

CMM | Capricorn Metals | -7.09% | $10.74 |

RMS | Ramelius Resources | -6.93% | $3.76 |

EVN | Evolution Mining | -6.81% | $12.58 |

VAU | Vault Minerals | -6.71% | $4.31 |

By Stephanie Gardner

Lynas achieves first Samarium oxide production

[9:54 am] Lynas has produced its first Samarium oxide at its Malaysia facility, expanding its separated Heavy Rare Earth product range to three and reinforcing its position as the only commercial producer of separated Heavy Rare Earth oxides outside China.

First production was forecast for April 2026 but has been delivered ahead of schedule, marking the first milestone in the expanded Heavy Rare Earths separation facility development

Samarium oxide has applications across high-performance magnets, electronics, aerospace, optics, catalysts and medical uses, broadening Lynas' addressable market

The expanded facility's initial flowsheet will include six separated Heavy Rare Earth products: Samarium, Gadolinium, Dysprosium, Terbium, Yttrium and Lutetium, with full capacity expected within two years

This announcement was marked as non-market sensitive.

Company page: Lynas Rare Earths (LYC)

Austin Engineering renegotiates Chile OEM contract

[9:47 am] Austin Engineering has successfully renegotiated its loss-making Chile OEM contract, with revised pricing and payment terms expected to return the arrangement to targeted profitability from May 2026.

The previous contract had been loss-making, prompting Austin to suspend new orders

Remaining legacy orders are expected to be completed in April 2026, ending the recurring EBITDA drag

Revised terms include a pricing adjustment and improved payment terms, with deliveries under the new agreement expected to commence May 2026

Company page: Austin Engineering (ANG)

Well that's embarrassing: ASX futures error

[9:45 am] Oh the stresses of such an overnight session. I messed up this morning's futures line which said: "ASX 200 futures are up 149 pts (-1.74%) as of 8:30 am AEDT."

Instead of: ASX 200 futures are down 149 pts (-1.74%) as of 8:30 am AEDT.

Apologies for the stitch up.

Putting it all together: Inflation risks, energy shock, hawkish central banks and war escalation converg

[9:31 am] The past 24 hours have crystallised a more stagflationary backdrop, with stalling inflation progress, central banks shifting toward hikes and energy prices surging on fresh escalation.

To summarise everything we've posted this morning:

Powell said the Fed "wasn't making as much progress on inflation as we had hoped," flagging upside inflation risks from the war while pushing back on stagflation fears. The Fed held at 3.50-3.75% with only ~25bp of cuts still pencilled in for 2026, well below the ~60bp priced just last month

Central banks are repricing from cuts to hikes. Swaps now fully price 50bp of ECB hikes in 2026, markets put a 50% chance of a BOE hike to 4% by December, and the two-year German yield hit its highest since August 2024

February US PPI came in hot, with headline up 0.7% month-on-month versus 0.3% ests and the three-month annualised core pace at its highest since May 2022. Critically, soaring energy prices have yet to fully pass through

Iran struck Qatar's Ras Laffan LNG facility overnight, causing extensive damage, while Saudi Arabia intercepted ballistic missiles aimed at Riyadh. Brent is nearing US$110 and Wood Mackenzie warns flows could take considerably longer to normalise than markets assume even after the Strait reopens

Trump is reportedly considering operations targeting Iran's nuclear material and has threatened strikes on Kharg Island, Iran's main oil export hub, suggesting limited appetite for an early offramp

Four rate decisions in 24 hours

[9:25 am] The Bank of Canada and Fed kept interest rates unchanged overnight, while the Bank of Japan, Bank of England and European Central Bank are all also expected to hold today.

That said, European markets are rapidly repricing for monetary tightening as the conflict escalates, with the region's status as a major energy importer leaving it particularly exposed to a sustained inflation shock.

Swaps markets are now fully pricing 50 bp of ECB rate hikes in 2026, a sharp shift that comes just ahead of Thursday's policy meeting where the ECB is widely expected to hold the deposit rate steady at 2%.

The two-year German yield jumped as much as 9bp to 2.47%, the highest since August 2024, while the euro fell 0.2% to $1.1522, with both European bonds and the currency reversing a short-lived relief rally earlier in the week.

The Bank of England is also expected to shift hawkish and potentially complicate the UK's rate cut trajectory.

Markets now price a 50% chance of a rate hike to 4% by December, a sharp reversal from prior expectations of two cuts to 3.25% this year, with household inflation expectations at particular risk of becoming entrenched given energy's salience in the CPI basket

A full hawkish follow-through remains unlikely given rising unemployment and weak demand, which limit workers' ability to push for higher wages and firms' ability to pass through price increases

Commodity prices smashed

[9:20 am] A very rough overnight session for most base and industrial metals.

Commodity | % Chg | Price (US$) |

|---|---|---|

Palladium | -7.8% | $1,476 |

Platinum | -5.0% | $2,025 |

Copper | -5.0% | $5.49 |

Silver | -5.0% | $75.36 |

Gold | -3.7% | $4,818 |

Zinc | -2.8% | $3,136 |

Aluminium | -1.1% | $3,351 |

Nickel | -1.0% | $17,278 |

Oil prices: Can't stop, won't stop

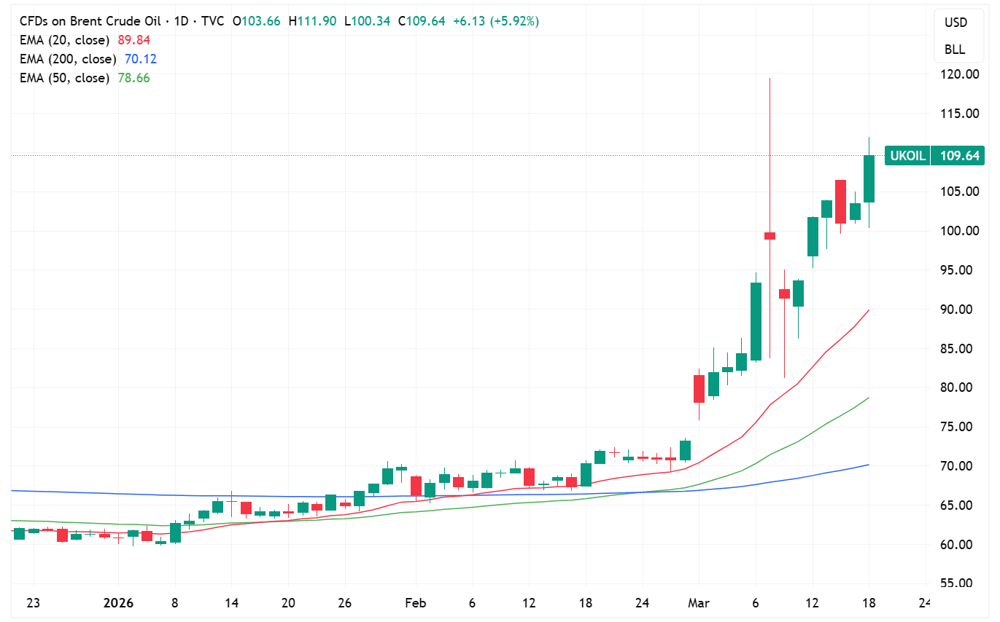

[9:14 am] Brent crude finished the overnight session up 5.9% to US$109.64 a barrel, the highest close since July 2022. Prices are now approaching the brief US$119.50 it hit on 9 March 2026.

Brent daily price chart (Source: TradingView)

Powell flags "difficult situation"

[9:10 am] Powell's press conference struck a notably cautious tone, with the Fed chair explicitly acknowledging the war's inflationary impact while pushing back on stagflation comparisons and signalling rates will move only if the economic outlook clarifies.

The key line: Powell said the Fed "wasn't making as much progress on inflation as we had hoped."

Powell flagged labour market risks are to the downside, calling for lower rates, while inflation risks are to the upside, calling for rates to stay on hold or move higher

He described the Fed as sitting "on the borderline of restrictive vs. not restrictive."

Powell directly attributed near-term inflation pressure to the war, noting higher energy prices from Middle East supply disruptions will push up overall inflation in the near term, though he said it is too soon to assess the full scope and duration of effects.

Powell pushed back on stagflation fears, arguing the term applies to a far more serious set of circumstances than today's environment, where unemployment is close to its longer-run normal and inflation is only around one percentage point above target.

Powell flagged that higher US energy production could partially offset the oil shock, noting that as a net energy exporter, more profitable domestic oil companies may increase drilling if prices remain elevated, though only if they are convinced the increase is persistent.

Fed holds rates steady, nudges up inflation forecasts

[9:06 am] The March FOMC meeting delivered no surprises on rates but revealed a committee grappling with rising inflation projections and war-related uncertainty, with only modest easing still pencilled in for 2026.

Rates were held unchanged at 3.50-3.75% as widely expected, with only one dissent from Governor Miran in favour of a 25bp cut, fewer than the up to three dissenters some previews had flagged.

The updated SEP maintained roughly 25 bp of cuts through end of 2026 to a midpoint of 3.375%, unchanged from December's projections,

Though this is well below the ~60 bp of cuts markets were pricing just last month before oil prices surged and PPI came in hot.

The Fed lifted its 2026 headline PCE forecast to 2.7% from 2.4% and core PCE to 2.7% from 2.5%

GDP growth was nudged up slightly to 2.4% from 2.3% and the unemployment rate forecast was left unchanged at 4.4%.

The FOMC statement added an explicit reference to the uncertain implications of the Middle East war, and softened its characterisation of the labour market, replacing "shown some signs of stabilisation" with "little changed in recent months."

This is just the FOMC meeting, we'll post Powell's conference takeaways above.

February PPI surges well above consensus, with goods inflation at a two-year high

[9:03 am] Producer price inflation came in hot across both headline and core measures in February, with the three-month annualised core pace hitting its highest level since May 2022 and pointing to renewed upstream price pressures.

Headline PPI rose 0.7% month-on-month vs. 0.3% ests, with the annualised rate climbing to 3.4% vs. 2.9% a month ago

The monthly gain was the largest since July 2025.

Core PPI rose 0.5% month-on-month vs. 0.3% ests, the three-month annualised core pace of 7.81% is the highest since May 2022.

Goods prices jumped 1.1%, the largest increase since August 2023, with over 20% of the final demand goods rise attributable to a 48.9% surge in fresh and dry vegetable prices

Energy was also a significant contributor, up 2.3% after falling 2.3% in January.

Services rose 0.5% on the month, with eggs jumping 93.6% after collapsing 63.9% in January, while transportation and warehousing was up 0.5% and trade services rose 0.4%.

Overall, a very ugly print, at a time where soaring energy prices have yet to fully pass through.

Hedge funds suffer worst drawdowns since Liberation Day as Iran conflict upends crowded trades

[8:58 am] The oil price surge and broad risk-off shift have hit hedge funds across nearly every strategy, with traditional diversification providing little protection as markets reprice around an inflation and growth shock simultaneously.

The hedge fund industry is down around 2.2% since the war began on 28 February, with long/short equity funds the hardest hit, falling approximately 3.4% in March alone, according to HFR data.

The MSCI World Index has declined over 3% since the start of the war after hitting a record high in early February, while the US dollar index has strengthened around 2% over the same period as crowded short-dollar positions are rapidly unwound.

Unusually, strategies that typically benefit from volatility have also struggled, with global macro and CTA funds both down around 3% since the conflict began, reflecting the difficulty of trading a shock that combines inflation fears with a potential negative growth impulse.

JPMorgan flagged a structural difference from prior oil shocks, where normally higher crude prices generate petrodollar recycling back into global financial assets, but shipping disruptions through the Strait of Hormuz are interrupting those flows, removing a key source of liquidity for markets.

JPMorgan views equities as more vulnerable than bonds from a positioning perspective in both developed and emerging markets, suggesting further unwinds are possible if the conflict persists.

Source: CNBC

Conflict escalates as Trump weighs seizing nuclear material

[8:57 am] The war is entering a potentially decisive phase with Trump considering a highly complex operation targeting Iran's nuclear material, while mixed signals emerge on the Strait of Hormuz.

Trump is considering a military operation to seize or destroy Iran's near-bomb-grade nuclear material, with Secretary of State Rubio indicating such an operation would require a commando force

The US bombed Iranian missile installations along the Strait of Hormuz on Wednesday, with officials citing the sites as a direct risk to international shipping.

Axios reported Trump is the most bullish person in the White House on prosecuting the war and appears more aligned with Israeli PM Netanyahu's maximalist objectives than his own aides, suggesting limited appetite for an early offramp despite Trump's public comments about leaving "in the near future."

Trump has threatened to expand strikes on Kharg Island, Iran's main oil export hub, which would represent a significant escalation with direct implications for global oil supply.

The Strait of Hormuz is showing tentative signs of thawing, with around 90 ships including oil tankers reported to have crossed since the war began

Iran strikes Qatar's Ras Laffan in major escalation targeting Gulf energy infrastructure

[8:56 am] The conflict has crossed a critical threshold with Iran directly striking the world's largest LNG export facility, raising the prospect that supply disruptions will persist well beyond any ceasefire.

Qatar's Ras Laffan Industrial City, home to the world's largest LNG export plant, suffered "extensive damage" in the strike, representing the first direct hit on a major LNG production facility since the conflict began.

Iran's IRGC formally declared energy assets in Saudi Arabia, the UAE and Qatar as "direct and legitimate targets," with Saudi Aramco evacuating the Samref refinery and Jubail petrochemical complex, and the UAE's Al Hosn gas asset also being evacuated.

The conflict has now triggered production curtailments across Saudi Arabia, the UAE, Kuwait and Iraq, while Qatar had already halted LNG output at the world's biggest plant prior to the strike.

Wood Mackenzie's Tom Marzec-Manser warned that even once the Strait of Hormuz reopens, flows could take considerably longer to normalise given the risk of damaged infrastructure, shifting market focus from shipping disruption to physical production impairment.

Source: Bloomberg

A stacked overnight session

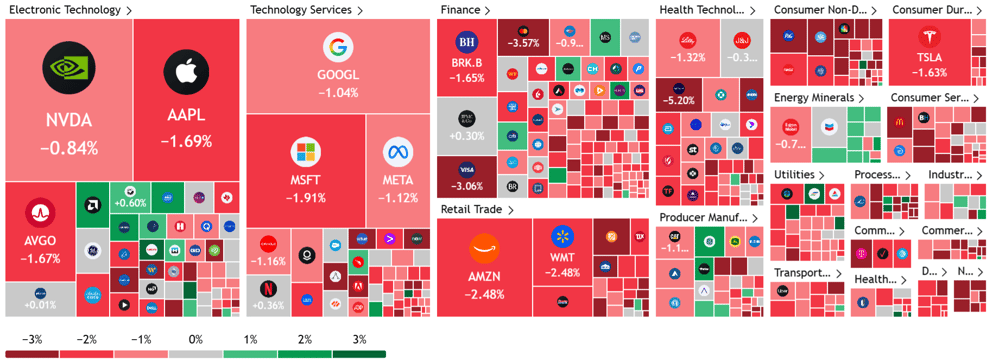

[8:51 am] US indices traded sharply lower after a catalyst rich overnight session that featured higher oil prices, more key energy infrastructure damage in the Middle East and hawkish takeaways from Powell's press conference.

Every S&P 500 sector finished lower, though Energy (-0.16%) outperformed on a relative basis, while Materials (-2.25%), Discretionary (-2.32%) and Staples (-2.44%) underperformed.

S&P 500 heatmap (Source: TradingView)

Good morning!

[8:36 am] ASX 200 futures are down 149 pts (-1.74%) as of 8:30 am AEDT.

The overnight session in a nutshell:

Local sharemarket set to give back Tue-Wed gains and mark fresh year-to-date lows after a downbeat overnight session

Major US benchmarks sharply lower after hawkish remarks from the Fed, an intensifying Middle East conflict that continues to damage key energy infrastructure and a hotter-than-expected US PPI print

Brent rallied 6.6% to US$110.4 a barrel, while most commodity prices, including copper, gold and palladium, fell more than 3%