ASX 200 Live Today - Monday, 9th February

The S&P/ASX 200 is set to bounce after a sharp rally on Wall Street and broad-based gains for commodities. Here are today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Monday, February 9. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Be sure to refresh manually for the latest updates — and let us know how we can make it even better.

ASX 200 rallies, recovers most of Friday's losses

[2:25 pm] ASX 200 up 1.96%, hovering around intraday highs. The market is pretty much back to breakeven in the last two sessions. Last Friday's laggards are topping the leaderboards, with Tech (+3.47%), Real Estate (+3.20%) and Materials (+3.03%) all up strongly. A much needed bounce at a time where the market was flagging poor breadth, with plenty of sectors starting to roll over key levels. Volatility may remain elevated as commodity prices continue to trade in a whipsaw-like action and tech stocks still need to show more strength. Very keen for Tuesday, as the volume of reporters begins to pick up. Let's see if the market can show some form of consolidation around these levels.

REA Group fades early gains

[1:50 pm] REA shares opened 3.7% higher ($174.47) thanks to a strong overnight lead and bounce in software stocks, rallying as much as 5.2% within the first hour of trade. However, the stock now back at breakeven ($168.40) and underperforming the broader tech sector, which is currently up 3.2%.

This intraday weakness might reflect REA's weaker-than-expected first-half FY26 result, which featured:

Revenue up 5% to $916m vs $927.7m ests (1% miss)

EBITDA up 6% to $569m vs $570.3m ests (in-line)

Net profit from core operations up 9% to $341m vs $344.1m ests (1% miss)

EPS up 9% to $2.58 vs $2.64 ests (2% miss)

Interim dividend up 13% to $1.24 per share vs. Morgans ests of $1.29 (4% miss)

Announced on-market buy-back of up to $200m as part of capital management plan

FY26 national residential Buy listing volumes to decline by 1-3% vs. prior expectations of listings growth to be broadly in-line with FY25

The average analyst target price was cut by 5.2% to $222.71 after the result,

Soul Patts weighs Ironbark stake sale

[1:48 pm] Washington H. Soul Pattinson is considering its position in Ironbark Asset Management as the wealth platform moves to secure a deep-pocketed partner to fund M&A and expansion into the US advisory market, according to the AFR.

Soul Patts owns 36.8% of Ironbark after investing since 2016 and is yet to decide whether it will sell down most or all of its holding as part of the proposed transaction.

Ironbark oversees more than $90bn across funds management, trusteeship and advice, with FY25 revenue forecast at $190m and 61% generated from wealth management.

A global wealth manager is in late-stage talks to acquire a significant equity stake to bankroll a $300m+ inorganic growth pipeline and support entry into the US RIA market.

Source: AFR

Australia household spending slips

[1:03 pm] Australian household spending fell 0.4% month-on-month in December, following rises of 1.0% in November and 1.4% in October. Here are some of the key takeaways from the ABS report:

Household spending over the year remains high, up 5.0 per cent compared to December 2024.

"Household spending declined in December. We saw high spending in October and November, which had major sales and cultural events boost spending," said Tom Lay, ABS Head of Business Statistics

"The fall in December indicates that households brought forward purchases during sales events in October and November."

"These falls were across a range of categories including discretionary items such as electronics, clothing and furniture, as well as essential items like healthcare."

The biggest fall was in Clothing and footwear, down 2.4 per cent. Furnishings and household equipment was close behind, down 1.7 per cent, and Health dropped 1.3 per cent.

Source: ABS

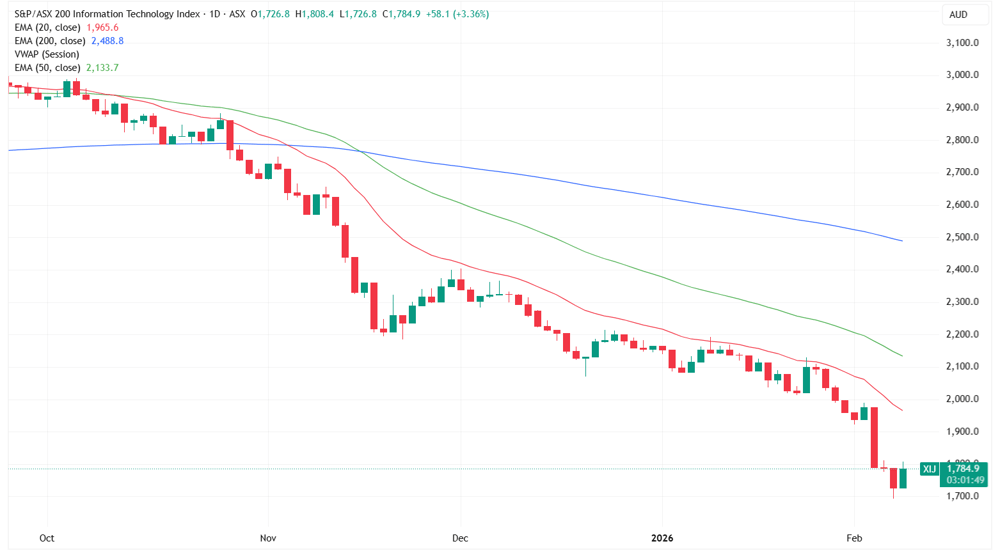

A bounce for ants

[1:00 pm] The Tech index is currently up 3.3%, easing from session highs of 4.7%. Despite the solid day, this is just one small green candle in what is still a steep downtrend.

S&P/ASX 200 Tech Index daily chart (Source: TradingView)

Some interest commentary from Macquarie this morning: "While catching a falling knife can sometimes be very rewarding, as stocks bottom at the end of Stage 4, the base rate of success low. You really need a positive catalyst, and it seems more likely the headwinds will grow."

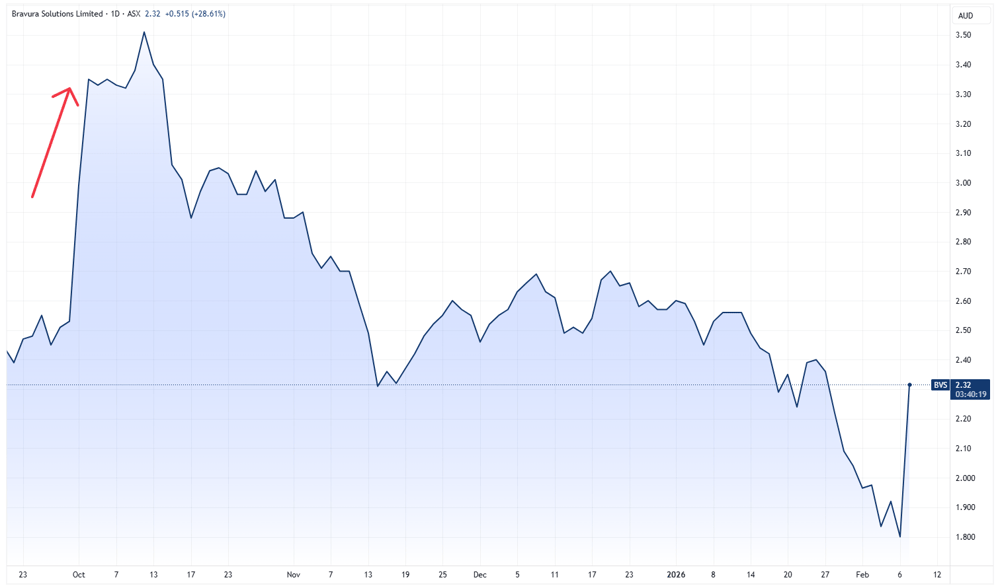

Bravura rallies on guidance upgrade

[12:23 pm] Bravura shares opened 23.3% higher ($2.22) after upgrading its FY26 guidance this morning. The stock has managed to trend slightly higher, currently up 27.7% ($2.30). Here are some of the key numbers from earlier:

Revenue guidance upgraded to $280–285m vs. prior $265–275m and $269.7m ests (4.6% upgrade vs. prior, 4% beat vs. ests at the midpoint)

Cash EBITDA guidance lifted to $69–73m vs. prior $55–65m, $67.7m ests (18.3% upgrade vs. prior and 8% beat vs. ests)

PPE CapEx ~$4m vs prior $2–3m, reflecting extra investment in internal technology

The interesting thing is that Bravura upgraded its FY26 guidance back in October, lifting revenue expectations by 2-6% to $265-275 million and cash EBITDA guidance by 10-30% to $55-65 million. The stock rallied 18.1% on the day of the announcement (1-Oct-25) and a further 17% over the next seven sessions to $3.51.

In other words, even after today's one-day rally, the stock is still 50% off where it was after the October upgrade.

Bravura price chart (Source: TradingView)

Uranium stocks broadly higher

[11:43 am] Uranium stocks are broadly higher, but still struggling to recoup last Friday's decline. Paladin Energy (+3.8%) is still down 7.4% in the last two sessions. Uranium prices slipped 0.5% overnight to US$85.2/lb, and down 16% from recent highs of US$101/lb.

Ticker | Company | % Chg | Price |

|---|---|---|---|

BMN | Bannerman Energy | 8.83% | $3.82 |

BOE | Boss Energy | 8.39% | $1.55 |

AGE | Alligator Energy | 8.11% | $0.04 |

DYL | Deep Yellow | 7.95% | $2.38 |

EL8 | Elevate Uranium | 5.97% | $0.36 |

DEV | Devex Resources | 5.00% | $0.21 |

LOT | Lotus Resources | 4.33% | $2.17 |

PEN | Peninsula Energy | 3.91% | $0.67 |

PDN | Paladin Energy | 3.86% | $11.44 |

NXG | NexGen Energy | 0.32% | $15.65 |

Copper stocks bounce

[11:35 am] Copper stocks are trading broadly higher, with most names up 4-6%. Copper prices rallied 2.9% overnight to US$5.97/lb, and currently up 0.7% in today's session.

Ticker | Company | % Chg | Price |

|---|---|---|---|

AIS | Aeris Resources | 7.07% | $0.53 |

HCH | Hot Chili | 6.44% | $1.74 |

CSC | Capstone Copper | 6.09% | $16.19 |

FFM | Firefly Metals | 5.75% | $1.88 |

SFR | Sandfire Resources | 3.05% | $19.12 |

CYM | Cyprium Metals | 2.17% | $0.47 |

HGO | Hillgrove Resources | 2.04% | $0.05 |

AR1 | Austral Resources | 1.90% | $0.11 |

29M | 29Metals | 1.69% | $0.42 |

Analysts' take on REA Group

[11:25 am] REA reported a slightly weaker-than-expected 1H26 result last Friday, driven by soft buy volumes and a full-year guidance. The stock finished the session 7.8% lower, well-off session lows of -17%. Here's what analysts are thinking:

Jarden maintained Neutral, lowered target from $196.00 to $177.00. Result slightly below expectations, AI risk manageable but uncertain, adjusted valuation assumptions.

RBC Capital Markets maintained Sector Perform, lowered target from $225.00 to $200.00. Listings environment deteriorating, concerns over CoStar competition and AI impact on yield, reduced EBITDA forecasts.

JPMorgan maintained Overweight, lowered target from $225.00 to $215.00. Result broadly in line with soft volumes, proactive AI rollout, buyback supported by strong cash, positive yield outlook.

Tech snaps three-day slide

[10:38 am] Tech (+4.1%) snapped a three-day slide after a strong lead from Wall Street, where the Nasdaq rallied +2.1%, with most software names up 5-6% overnight.

Ticker | Company | % Chg | Price |

|---|---|---|---|

BVS | Bravura Solutions | 26.11% | $2.27 |

WBT | Weebit Nano. | 11.29% | $4.83 |

SDR | Siteminder | 7.39% | $4.36 |

NXT | Nextdc | 6.53% | $13.54 |

MP1 | Megaport | 6.41% | $10.96 |

ELS | Elsight | 5.98% | $3.90 |

CAT | Catapult Sports. | 5.72% | $3.61 |

TNE | Technology One | 4.60% | $22.87 |

360 | Life360 | 4.40% | $26.08 |

MAQ | Macquarie Technology Group | 3.99% | $64.19 |

CDA | Codan | 3.62% | $35.82 |

NXL | Nuix | 3.48% | $1.55 |

WTC | Wisetech Global | 3.17% | $49.11 |

OCL | Objective Corporation | 3.00% | $14.44 |

DDR | Dicker Data | 2.24% | $10.06 |

XRO | Xero | 1.42% | $82.92 |

Top ASX 200 gainers and losers

[10:13 am] Friday's losers are bouncing back strongly, with a mix of tech and resources trading sharply higher.

Ticker | Company | % Chg | Price |

|---|---|---|---|

DRO | Droneshield | 11.03% | $3.22 |

CAR | Car Group | 10.05% | $26.94 |

DYL | Deep Yellow | 7.05% | $2.36 |

CSC | Capstone Copper Corp | 7.01% | $16.33 |

XYZ | Block | 6.27% | $81.40 |

SLX | Silex Systems | 6.09% | $6.45 |

IPX | Iperionx | 6.06% | $6.13 |

RYM | Ryman Healthcare | 5.78% | $2.38 |

NXT | NextDC | 5.66% | $13.43 |

ZIM | Zimplats | 5.15% | $21.63 |

Ticker | Company | % Chg | Price |

|---|---|---|---|

CGF | Challenger | -3.70% | $8.59 |

MGH | Maas Group | -2.02% | $4.12 |

SNZ | Summerset Group | -1.86% | $9.52 |

GQG | GQG Partners | -1.18% | $1.68 |

AUB | AUB Grou | -0.90% | $27.64 |

AMC | Amcor | -0.84% | $68.24 |

ASX | ASX | -0.53% | $55.99 |

APA | APA Group | -0.46% | $8.69 |

BPT | Beach Energy | -0.44% | $1.14 |

AZJ | Aurizon | -0.28% | $3.53 |

Bhagwan Marine to acquire Riverside Marine

[9:40 am] The deal expands Bhagwan’s fleet management operations, adding Riverside’s ~30 vessels and boosts FY26 earnings.

Enterprise value of up to $130m, with upfront consideration of $120m funded by $70m debt, $20m vendor equity, and $30m institutional share placement

Riverside FY26 forecast: revenue $63m, EBITDA $26m, with earn-out up to $10m based on EBITDA milestones

Highly earnings accretive, with pro forma EPS of ~14% and return on equity of over 20%

Equity raising: $30m secured via 63.9m new shares at $0.41 (8.3% discount to last close)

Split into Tranche 1 (40m shares) and Tranche 2 (23.9m shares), plus 9.3m shares from directors raising $3.8m

Overall, a pretty solid acquisition that values Riverside at 5x FY26e EBITDA, although $70 million debt is pretty substantial for the ~$123 million market cap company. Bhagwan recently lowered its debt to $1.0 million in the December half, down from $5.3 million at 30 June 2025.

Company page: Bhagwan Marine (BWN)

SEEK takes $356m impairment on Zhaopin

[9:33 am] The impairment reflects weak macro conditions, strategic review outcomes, and a planned simplification of Zhaopin’s ownership structure. Seek’s investment relates to Zhaopin, its China-based recruitment platform.

Post-tax impairment of $356m reduces Seek’s investment in Zhaopin to $182m from $529m at 30-Jun-25

Discussions underway to simplify Zhaopin’s ownership, including reducing certain minority holdings, which would increase Seek's stake from 23.5% to ~30% with no cash outflow

Zhaopin’s new management completed a strategic review, shifting focus to growth areas aligned with China’s economic priorities, requiring additional investment that may pressure margins in CY2026–27

Company page: Seek (SEK)

Pepper Money receives indicative acquisition proposal

[9:29 am] Challenger and Pepper Group have made a non-binding, conditional proposal to acquire 100% of Pepper Money.

Proposal values Pepper Money at $2.60 per share, less any 2025 final or special dividends

This represents a 47.7% premium to Pepper Money's closing price on Friday ($1.76)

Challenger would hold no more than 25% of total shares, with Pepper Group maintaining an interest at least equal to its current stake

Company page: Pepper Money (PPM)

Bravura upgrades FY26 guidance

[9:27 am] Higher project engagement and controlled costs support a lift in revenue and EBITDA forecasts, with additional tech investment boosting CapEx.

Revenue guidance upgraded to $280–285m vs. prior $265–275m and $269.7m ests (4.6% upgrade vs. prior, 4% beat vs. ests at the midpoint)

Cash EBITDA guidance lifted to $69–73m vs. prior $55–65m, $67.7m ests (18.3% upgrade vs. prior and 8% beat vs. ests)

PPE CapEx ~$4m vs prior $2–3m, reflecting extra investment in internal technology

Bravura shares have tumbled 48% since October, trading at the lowest level since December 2024. The stock rallied to multi-year highs in October after the company upgraded its FY26 revenue guidance by 2-6% to $265-275 million and cash EBITDA guidance by 10-30% to $55-65 million. The stock rallied 18.1% on the day of the announcement (1-Oct-25).

Company page: Bravura Solutions (BVS)

CAR Group 1H26 results

[9:17 am] CAR Group delivered a solid performance across major regions, with a record interim dividend and reaffirmed its FY26 guidance.

NPAT up 16% year-on-year to $197m vs. $196.4m ests (0.3% beat)

Revenue up 8% year-on-year to $626m vs. $619.1m ests (1.1% beat)

Adjusted EBITDA $339m vs. $340.3m ests (0.4% miss)

Interim dividend up 10% to 42.5 cents vs. Morgans ests of 41 cents (3.6% beat)

Regional performance: Australia maintained market leadership and delivered growth across all segments, North America saw strong premium product uptake, Latin America and Asia delivered double-digit growth driven by new products and expanded market share

The company reaffirmed its FY26 guidance (which was left unchanged at the November AGM).

Revenue growth of 12-14%

Proforma EBITDA growth of 10-13%

Adjusted NPAT growth of 9-13%

Overall, a solid set of numbers, but CAR is navigating a tricky patch. The stock has fallen roughly 40% since last August, hitting its lowest level since August 2023. Despite the pullback, CAR still trades on a trailing PE of 33x, in line with levels seen in 2020–22, although the stock had aggressively re-rated to the low 50s in 2024–25. Can the stock muster up a strong bounce off the back of this solid result and overnight tech bounce?

Company page: CAR Group (CAR)

Block to cut up to 10% of staff

[9:04 am] Jack Dorsey’s payments firm is restructuring, integrating Cash App with Square, and expanding initiatives like Bitcoin mining and AI tools. Job cuts are part of efficiency drives to support a US$12 billion gross profit target for 2026.

Source: Bloomberg

Pepper Money set for privatisation

[9:00 am] KKR is seeking to take Pepper Money private again, using its portfolio insurer Global Atlantic to originate loans, according to the AFR.

Pepper Money, 60% owned by KKR, is in advanced talks to be taken private, with a deal expected in the coming weeks.

Global Atlantic Financial, another KKR-owned company, would use Pepper to originate loans, potentially selling unwanted loans to a partner, likely ASX-listed Challenger.

The move aligns with a trend of insurers acquiring origination capabilities, similar to Apollo’s interest in HSBC’s Australian loan portfolio and KKR’s involvement in RAMS loan sales.

Pepper was first taken private by KKR in 2017, relisted in 2021 at $2.89, and last traded at $1.76.

Company page: Pepper Money (PPM)

S&P 500 Q4 earnings beat expectations

[8:58 am] Corporate results for Q4 show stronger-than-expected earnings and revenue growth, though fewer companies are exceeding EPS forecasts than historical averages, according to FactSet.

EPS growth is 13.0% vs. 8.3% expected

76% of companies have beaten consensus EPS, below the one-year average of 79% and five-year average of 78%.

73% of companies have beaten sales estimates, above the one-year average of 71% and five-year average of 70%.

Earnings are 7.6% above expectations on average, slightly above the one-year positive surprise rate of 7.4% but below the five-year average of 7.7%.

Revenue surprises average 1.4% above expectations, above the one-year rate of 1.3% but below the five-year average of 2.0%.

Japan election fuels stocks, weakens yen and bonds

[8:57 am] Prime Minister Takaichi’s landslide win paves the way for stimulus-driven equity gains while raising pressure on the yen and government bonds.

The LDP secured a two-thirds lower house majority, exceeding market expectations and giving Takaichi a clear path to implement fiscal stimulus.

Nikkei and Topix are set to extend rallies, with sectors like defense, nuclear energy, AI and semiconductors likely to benefit most from government spending.

The yen weakened 0.2% to 157.57 USD after falling 1.6% last week, with further declines possible as markets anticipate stimulus and BOJ rate adjustments.

Japanese government bonds remain under pressure, particularly super-long maturities, amid fiscal concerns and proposals like a temporary food sales tax cut.

Market pricing suggests a 25 bp BOJ rate hike is 75% priced in for April, fully priced in by June, reflecting expectations of tighter monetary policy.

Source: Bloomberg

US–Iran talks restart under military pressure

[8:55 am] Washington and Tehran resumed indirect negotiations with signals of flexibility on nuclear terms, while the US ramps up military presence and investors watch Middle East risk closely.

Trump said talks with Iran were “very good” and will continue next week, warning consequences would be “very steep” without a deal, while hinting a nuclear-only agreement could be acceptable.

Indirect talks in Oman were the first since the US joined Israel’s 12-day war in June, with Iran saying discussions started well despite deep mistrust on both sides.

The key fault line remains uranium enrichment, with the US pushing for a permanent halt while Iran insists on its right to enrich under the non-proliferation treaty and refuses to negotiate missiles.

Israel is pushing back on any softening stance, with Netanyahu set to meet Trump to demand limits on Iran’s ballistic missiles and regional proxy support as Tehran remains politically and economically vulnerable.

Source: FT

PBOC extends gold buying despite selloff

[8:52 am] China’s central bank kept accumulating gold through recent market turmoil, reinforcing official demand even as speculative positioning in bullion was violently unwound.

The PBOC lifted gold holdings by 40,000 ounces last month, extending its buying streak to 15 consecutive months since restarting purchases in November 2024.

Global central bank purchases exceeded 860 tonnes in 2025, according to the World Gold Council, below the ~1,000 tonnes seen in each of the prior three years but still structurally supportive.

Official sector demand remains a key stabiliser for bullion, helping underpin gold’s role in reserves even as speculative flows drive short-term volatility.

Source: Bloomberg, World Gold Council

Big Tech’s AI capex arms race

[8:48 am] US tech giants are unleashing unprecedented capital spending to dominate AI, driving a global data centre boom while unsettling investors and distorting economic signals.

Alphabet, Amazon, Meta and Microsoft forecast combined capex of about US$650bn in 2026, up roughly 60% year-on-year, with each company set to spend near or above the last three years combined.

Meta flagged capex up to $135bn (about 87% jump), Microsoft’s quarterly capex rose 66% with about $105bn projected for FY26, Alphabet plans up to $185bn and Amazon up to $200bn, all aimed at AI data centres and compute.

The spending surge is fuelling a global build-out of data centres, driving heavy borrowing, pinching energy and water supplies, and creating bottlenecks in labour, construction and Nvidia chip availability.

Concentrated investment by a few mega-cap firms risks skewing US macro data like construction, GDP and employment, making the economy appear stronger than underlying demand.

Investors are growing uneasy, with the four stocks shedding over $950bn in market value since earnings, even as AI hardware suppliers like Nvidia, AMD and Broadcom benefit from the capex wave.

Source: Bloomberg

Silver whipsaws as liquidity vanishes

[8:46 am] Silver saw extreme two-way volatility as thin liquidity and speculative positioning triggered forced selling and sharp rebounds across precious metals.

Spot silver rebounded nearly 10% to US$77.9/oz after plunging to intraday lows of US$64, this follows a 20% drop the prior session that erased last month’s rally.

Silver is down more than one third from its Jan 29 peak, marking the most violent moves since 1980 due to its smaller, less liquid market versus gold.

Market makers are widening spreads and cutting balance sheet usage as volatility spikes, weakening liquidity when it is needed most and amplifying price swings.

Chinese demand has faded, with local prices flipping to a discount, Shanghai Futures Exchange open interest at a four year low, and investors closing positions ahead of Lunar New Year.

Big bounce on Wall Street

[8:44 am] A very encouraging overnight session, with major US benchmarks and commodities trading broadly higher.

S&P 500 (+1.97%) reversed declines from the last two sessions and within 1% of all-time highs

Dow (+2.47%) rallied to fresh all-time highs after trading relatively sideways for the past four weeks

Nasdaq (+2.18%) bounced but still down 1.8% for the week and trading below its 50-day moving average

Russell 2000 (+3.6%) bounced off the 50-day, still 1.8% off its record high on 22-Jan

Nine out of 11 S&P 500 sectors higher, with Communication Services (-1.5%) and Discretionary (-0.6%) weakness reflecting declines from heavyweights Alphabet (-2.4%) and Amazon (-5.5%)

Good morning!

[8:28 am] ASX 200 futures are up 102 pts (+1.18%) as of 8:30 am AEDT.

The overnight session in a nutshell:

Major US benchmarks sharply higher, with the S&P 500 reversing declines from the last two sessions and the Dow rallying to fresh all-time highs

Sharp bounce in software stocks, a move largely tabbed to extreme oversold conditions

Broad-bounce for commodities, with gold up ~4% and just shy of US$5,000, silver up 9.8% to US$77.9 and copper up 2.9% to US$5.93/lb

A quite day for 1H26 results, with CAR reporting relatively in-line numbers and reaffirming its full-year guidance

To catch up on all overnight developments, check out today's Morning Wrap.