ASX 200 Live Today - Monday, 2nd March

The S&P/ASX 200 is set to slip ahead of a volatile session for global equity markets amid an escalation in the Middle East.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Monday, March 2. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

ASX 200 slips as stocks bounce off lows

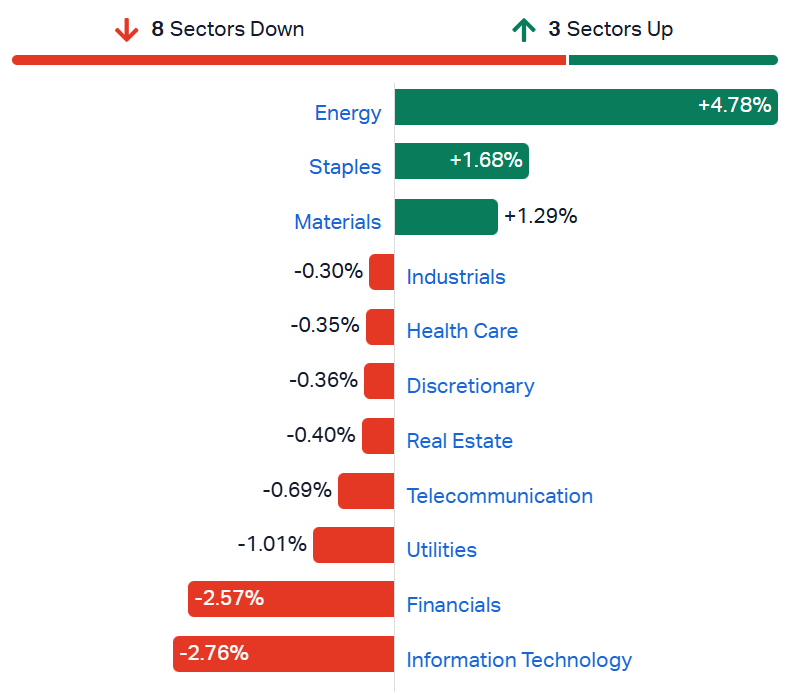

[1:50 pm] ASX 200 down 0.41%, recovering more than half of today's intraday losses (down as much as 0.86% in early trade). Most sectors bouncing off session lows, notable Tech (-2.9% now vs. -4.5% low) and Financials (-2.1% now vs. -3.1% low).

Materials (+1.1%) doing a lot of the heavy lifting today, with All Ords Gold (+3.8%) at record highs and a slight uptick for BHP (+0.07%) and Rio Tinto (+1.03%). If BHP closes higher, it'll make an eight straight record high. Energy (+4.5%) has almost halved from early highs (+7.7%), a move that matches the intraday reversal of oil prices. The situation remains highly fluid and headline driven.

That's all for today. Overall, the market remains in good shape following a strong February reporting season. UBS has described it as the best results season since 2019. ASX 200 earnings growth expectations have risen sharply to 13.6%, up from 11.3% a month ago and just 3.0% six months ago. Plenty of risks linger in the background, from geopolitical tensions and US-China trade friction to private credit concerns and sticky inflation, but the strength of the recent corporate earnings season is hard to ignore.

China's five-year plan: key commodity and supply-side signals

[1:37 pm] A Bloomberg article highlights how Beijing's pivotal five-year plan is set to launch this week, carrying significant implications for global commodity markets across critical minerals, clean energy, steel, and agriculture.

Critical minerals dominance is set to be reinforced, with potential for stronger export controls, producer consolidation and expanded strategic reserves. All of which would be bullish for rare earth and critical mineral prices at a time when the US is also pursuing a major stockpiling initiative

Clean energy infrastructure targets are expected to be raised, with new goals likely for long-distance power transmission, battery storage (already tracking ahead of the 30 GW 2027 target) and green hydrogen, supporting continued demand for renewables-related commodities

A tougher carbon intensity target, estimated at a 23% reduction to meet Paris obligations, will now be paired with an absolute emissions cap, replacing the more lenient energy intensity measure; overall Chinese emissions fell in 2025 for the first time since the pandemic

Industrial overcapacity remains an unresolved issue across solar, steel and oil refining, with government efforts so far relying on policy signalling rather than hard output targets; HSBC flags that supply-side measures may need to be complemented by demand-side stimulus to be effective

Agricultural commodity flows are in focus as China eases trade tensions with key exporters, with increased competition from US soybeans, Canadian canola and other suppliers likely to add to deflationary pressure across the farm sector

Source: Bloomberg

China home prices resume slide

[12:54 pm] New home prices fell in February, reversing January's brief uptick and casting doubt on the durability of policy-driven recoveries in the sector.

Prices in 100 cities fell 0.04% month-on-month in February, reversing a 0.18% gain in January and marking the steepest monthly decline since December 2022

Official data for 70 cities, due 16 March, has shown no monthly price increase since May 2023, highlighting the breadth and persistence of the downturn

Demand has remained weak despite repeated easing since 2021, including looser purchase rules, lower down-payment requirements and, most recently, Shanghai expanding mortgage limits and allowing eligible buyers to purchase additional homes

Macquarie's head of China economics cautioned that such measures can offer only a short-term boost and cannot reverse the broader down-cycle, noting home prices have fallen back to 2016 levels

A sustained recovery would require much stronger policy intervention to reset market expectations, though unconventional measures are not anticipated at this stage

Source: Reuters

ASX 200 lower, bouncing off worst levels

[11:48 am] ASX 200 currently down 0.44%, off session lows of 0.86%. A fairly calm session all things considered. Surprising to see the small end of town hold up relatively well, with the Small Ords up 0.33% and Emerging Companies Index up 0.13%. Some slight weakness across most sectors, with Financials and Tech notably lower amid the risk-off mood.

S&P/ASX 200 sectors (Source: Market Index)

Harvey Norman hit by target price cuts

[11:38 am] Harvey Norman shares tumbled 9.0% last Friday despite a relatively in-line 1H26 result. The main drag on sentiment was a below consensus underlying profit print, where Australia sales slowed materially through the key Black Friday and Christmas trading period.

JPMorgan maintained Neutral, lowered target from $7.30 to $6.50. Sales momentum eased materially late in the period with peak trading softer than expected, though premium positioning should cushion cost inflation and valuation looks broadly fair.

Jarden maintained Overweight, lowered target from $7.60 to $6.60. A Q2 slowdown drove an earnings miss, but inflation and AI are seen as upcoming catalysts with capital management signalling management confidence in the replacement cycle ahead.

UBS maintained Neutral, lowered target from $7.50 to $6.15. Franchising margins disappointed and late-half sales weakness raised concern, with UK losses set to persist near term, though New Zealand is benefiting from competitor exits.

Analysts upbeat on Virgin

[11:34 am] Virgin shares traded flat last Friday, despite reporting a stronger-than-expected 1H26 result. The beat was supported by above-guidance RASK growth of 6.4% and lower-than-expected depreciation and fuel costs. Though capex is expected to step up in the second half and into FY27 as management confirmed the purchase of remaining B737-8 MAX aircrafts. This move will lower leasing exposure, but weigh on near-term free cash flow.

Here's what analysts are thinking:

Jarden upgraded to Buy, maintained target at $4.00. EBIT beat consensus by ~5% with airline yield growth materially ahead of peers, though yield sustainability and fleet transition complexity remain key questions.

UBS maintained Buy, raised target from $4.20 to $4.25. PBT came in 6-10% ahead of expectations with strong deleveraging to 0.9x, and valuation looks attractive versus peers despite non-fuel cost disappointment.

E&P upgraded to Positive, raised target from $3.66 to $3.76. EBIT strength across Airlines and Velocity supported forecast upgrades over three years, with fleet renewal expected to improve unit economics as the balance sheet remains well-managed.

Analysts upgrade Coles despite earnings selloff

[11:30 am] Coles is receiving rating upgrades from several brokers this morning, despite the stock suffering a historic 7.4% selloff last Friday. The company's 1H26 result was largely in-line with market expectations, though the trading update for the first seven weeks of 2H26 was soft, relative to Woolworths.

Jarden upgraded to Overweight, lowered target from $23.00 to $21.60. Execution was steady with margin strength from mix and sourcing, though early H2 softness and liquor competition are key near-term risks.

JPMorgan upgraded to Overweight, raised target from $21.70 to $23.50. The market reaction was seen as excessive given solid underlying performance, with liquor strategy favouring margin over volume.

Morgans upgraded to Accumulate, maintained target at $22.90. Core execution was strong despite a slightly softer result, with own-brand momentum supporting customer value amid intense competition.

ASX 200 earnings season delivers strongest upgrades since 2022

[11:05 am] UBS was impressed by the strength of February reporting season, with beats outnumbering misses 2:1 and guidance upgrades running 3:1, with the analysts upgrading their ASX 200 year-end target to 9,400.

NPAT beats outnumbered misses 2:1 and guidance upgrades outnumbered downgrades 3:1, with the average company received a +0.4% earnings upgrade post-result

ASX 200 FY2026 earnings growth now tracking at +13.6% year-on-year, up from +11.3% a month ago and just 3.0% six months ago

The pace of upward revisions is the strongest since mid-2022

Banks and Miners led the market to all-time highs in February, its strongest monthly gain in seven years, with domestic consumer-facing stocks and industrials exposed to structural capex themes also contributing

Twelve ASX 100 companies saw share price moves of more than 10% on result day, despite the volatility, stock correlations are low and dispersing, suggesting a favourable environment for stock pickers

AI is starting to show tangible results, with CBA, Telstra, Woolworths, Coles, Breville, Seek, WiseTech and others cited quantifiable productivity and profitability impacts from AI investments for the first time

ASX 200 year-end target upgraded to 9,400 from 8,900

While the RBA is expected to tighten again in May, the precedent of 13 hikes in 2022/23 having limited impact on corporate profits tempers concern about the effect of this cycle on earnings

Banks dip but off session lows

[11:01 am] Banks opened broadly lower, but starting to bounce off intraday lows. The S&P/ASX 200 Financials Index was down as much as 3.1% in early trade, currently down 2.5%.

Ticker | Company | % Chg | Price |

|---|---|---|---|

MQG | Macquarie Group | -6.77% | $199.02 |

NAB | National Australia Bank | -3.40% | $47.36 |

WBC | Westpac Banking | -2.84% | $41.33 |

ANZ | Anz Group | -2.58% | $39.01 |

CBA | Commonwealth Bank | -2.33% | $170.55 |

JDO | Judo Capital | -1.91% | $1.69 |

BOQ | Bank Of Queensland | -1.64% | $6.89 |

BEN | Bendigo & Adelaide Bank | -1.59% | $10.54 |

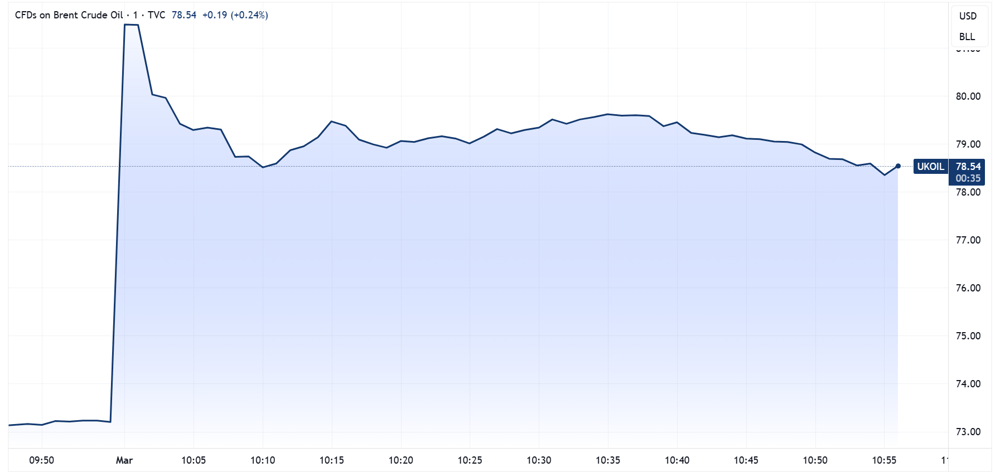

Brent finds a floor, Energy stocks fade

[10:57 am] Brent was trading 11% higher as the market opened, but gains quickly slipped to a 7% gain. Prices are now trying to stabilise around that ~7% level (US$78.5/bbl).

Local energy stock also slipped from the open, with the S&P/ASX 200 Energy Index up almost 12% in early trade, now up just 7.0%.

Brent intraday price chart (Source: TradingView)

Top ASX 200 gainers and losers

[10:34 am] Defence, gold and energy stocks have opened sharply higher after the weekend’s escalation in the US-Iran conflict lifted oil and safe-haven demand.

Tech and Financials are dragging in line with S&P 500 where they were the only two sectors to finish lower overnight.

Ticker | Company | % Chg | Price |

|---|---|---|---|

DRO | Droneshield | 10.91% | $4.02 |

BPT | Beach Energy | 9.13% | $1.20 |

RSG | Resolute Mining | 7.74% | $1.60 |

GMD | Genesis Minerals | 6.73% | $7.93 |

YAL | Yancoal Australia | 6.31% | $6.23 |

EVN | Evolution Mining | 6.09% | $17.59 |

NEM | Newmont Corporation | 6.06% | $187.93 |

STO | Santos | 5.84% | $7.16 |

WDS | Woodside Energy Group | 5.79% | $29.95 |

Ticker | Company | % Chg | Price |

|---|---|---|---|

ZIP | Zip Co | -6.81% | $1.78 |

MSB | Mesoblast | -6.25% | $2.10 |

FLT | Flight Centre Travel Group | -6.20% | $12.10 |

MQG | Macquarie Group | -6.12% | $200.41 |

QAN | Qantas Airways | -5.83% | $9.37 |

XYZ | Block, Inc | -4.75% | $89.68 |

FMG | Fortescue | -4.40% | $20.21 |

XRO | Xero | -4.37% | $79.51 |

WTC | Wisetech Global | -4.25% | $45.52 |

By Warren Masilamony

Gold stocks open at record highs

[10:11 am] The All Ords Gold Index is up 4.5% to fresh all-time highs this morning, with gold prices up 1.8% overnight and currently up 1.2% to US$5,344.

Ticker | Company | % Chg | Price |

|---|---|---|---|

RSG | Resolute Mining | 7.41% | $1.60 |

CMM | Capricorn Metals | 6.59% | $15.69 |

NEM | Newmont | 6.09% | $187.99 |

EVN | Evolution Mining | 5.97% | $17.57 |

RRL | Regis Resources | 5.30% | $9.94 |

OBM | Ora Banda Mining. | 5.04% | $1.36 |

RMS | Ramelius Resources | 4.79% | $4.81 |

GMD | Genesis Minerals | 4.51% | $7.77 |

NST | Northern Star Resources | 4.36% | $31.60 |

VAU | Vault Minerals | 4.25% | $6.13 |

PRU | Perseus Mining | 4.25% | $6.26 |

CYL | Catalyst Metals | 3.41% | $8.80 |

WGX | Westgold Resources | 2.71% | $7.96 |

ALK | Alkane Resources | 2.29% | $1.79 |

PNR | Pantoro Gold | 2.09% | $5.87 |

BGL | Bellevue Gold | 1.92% | $1.86 |

EMR | Emerald Resources | 0.85% | $7.14 |

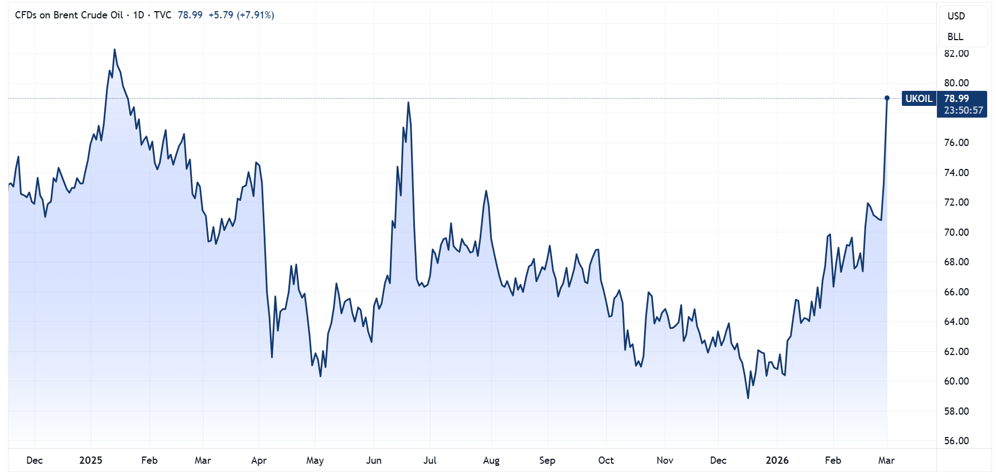

Oil prices open sharply higher

[10:10 am] Brent opened 11% higher to US$75.33 a barrel but has already started to give back gains within the first eight minutes of trade, currently up just 6.0% to US$71.3.

Brent price chart (Source: TradingView)

EOS secures new RWS orders and flags pipeline of Middle East and Korea opportunities

[9:51 am] Electro Optic Systems has announced two new remote weapon system orders totalling up to $19 million, while flagging a growing pipeline of opportunities tied to escalating regional conflicts and a major UAE-Korea defence partnership.

New order of US$12m (~$17m) for R400 RWS with 30mm cannons to a Middle Eastern GCC government customer, with delivery expected across 2026 and 2027

First sale into India's defence industry, with an R800 RWS order valued at $1-2m to a large prime contractor competing for a potential end-user requirement of over 130 systems

EOS is in discussions with a UAE manufacturing partner to develop proposals for local production of RWS products to support counter-drone requirements in both the UAE and Korea, separate to the previously announced conditional US$80m High Energy Laser Weapon contract with Goldrone

The UAE and South Korea recently announced a US$35bn defence industry cooperation agreement that EOS understands extends to counter-drone supply chains, potentially accelerating local manufacturing opportunities

EOS flagged that the current military conflict in the Middle East could accelerate negotiations already underway with several governments for advanced air defence systems, including its Slinger cannon-based RWS and APOLLO High-Energy Laser products

Company page: Electro Optic Systems (EOS)

Lynas secures 10-year Malaysia licence renewal

[9:47 am] Lynas has received confirmation from Malaysian authorities that its operating licence has been renewed for a decade from 3 March 2026, providing a significant boost to investment certainty for the company and its supply chain partners.

Company page: Lynas Rare Earths (LYC)

Magellan to merge with Barrenjoey

[9:42 am] Magellan Financial Group has announced a merger with investment bank Barrenjoey Capital Partners, acquiring 100% of the business and reshaping itself into a diversified financial services group.

MFG to own 100% of Barrenjoey, with implied value of $1.62 billion for Barrenjoey and total consideration of $903 million to MFG

MFG will issue 106.8m consideration shares to Barrenjoey shareholders

Post-completion ownership: MFG shareholders 58.2%, Barrenjoey parties 31.7%, Barclays 4.9% and placement shareholders 5.3%

MFG is raising up to $130m via placement and $20m via SPP at $8.45 per share vs. last close of $8.46

Merger completion expected in the June quarter 2026

Company page: Magellan Financial Group (MFG)

NRW Holdings chair trims stake

[9:38 am] NRW Holdings chair Michael Arnett has cut his stake in half, offloading 300,000 shares on 27 February, leaving him with a beneficial holding of 300,000 shares following the transaction.

NRW shares have soared 27% year-to-date and 99% in the last twelve months.

Company page: NRW Holdings (NWH)

Wagner family cashes out amid 190% share price surge

[9:35 am] One of the Wagner brothers has sold roughly 30 million shares in the family-founded construction materials group via a block trade at $4.40, according to the AFR. The stock has rallied 182% in the last twelve months to record levels, recovering from a ~88% drawdown between 2018 and 2023.

The block trade was managed by Unified Capital Partners at $4.40 per share

Wagners shares were trading around $4.64 at the time of writing, implying a modest discount to market

The four Wagner brothers collectively hold around 45% of the company

The trade follows a strong December half result, with after-tax profit up 70% to $21m on improved operating margins

Wagners supplies roughly one-third of the entire cement market in south-east Queensland and also operates bulk haulage services

Company page: Wagners Holding Company (WGN)

Star Entertainment posts deep losses as going concern risks intensify

[9:30 am] The Star's first-half result dropped at 8:26 pm last Friday, with the company reporting a 1H26 statutory net loss of $109.7 million as gaming revenue continued to deteriorate under regulatory pressure.

Revenue down 10% to $584.9m

Gaming revenue down 9% excluding the Treasury Brisbane closure, driven by declines in table games and the ongoing impact of mandatory carded play and cash limits at The Star Sydney

Statutory net loss of $109.7m after $34.0m in significant items (post-tax) covering restructuring, debt refinancing, JVP transaction and regulatory costs

January 2026 trading remained soft, with Star Sydney revenue 6% below January 2025 and 3% below the Q2 FY26 average

The state of play:

The company executed a non-binding term sheet with WhiteHawk Capital Partners on 26 February for a proposed debt refinancing, with a binding commitment required by 31 March and completion targeted by mid-May 2026

A covenant waiver was received on 27 February covering the 31 December 2025 test, failure to execute the WhiteHawk refinancing by 15 May 2026 would trigger a default under the existing Senior Facility Agreement

The board has flagged material uncertainty around the group's ability to continue as a going concern, with key risks including the quantum of the AUSTRAC penalty, the JVP transaction exit (which carries a ~$700m parent guarantee on DBC debt), and restoration of casino licences in both NSW and Queensland

Company page: The Star Entertainment Group (SGR)

Michael Hill delivers strong first-half earnings recovery

[9:27 am] Michael Hill reported its 1H26 result after market close on Friday, noting a sharp rebound in profitability for the first half of FY26 as same-store sales growth accelerated across all three markets.

Group sales up 3% to $371.0m

Comparable EBIT up[ 28.6% to $31.0m

Canada delivered record sales with SSS growth of 6.1%, Australia up 4.8% and New Zealand returned to growth at 1.8%

Gross margin broadly flat at 61.2%, with higher gold, silver and metal input costs offset by improved product mix and promotional discipline

Net cash position of $20.7m at half year, a $30.5m improvement on the $9.8m net debt position a year earlier

No interim dividend declared, though the board intends to reinstate dividends at the full year result subject to trading conditions

Early second-half trading is encouraging, with group SSS up 6.0% in the first eight weeks of 2H26 (Australia up 6.5%, Canada up 13.0% and New Zealand up 7.1%)

Company page: Michael Hill International (MHJ)

Oil markets and Iran: cutting through the noise

[9:23 am] A market data aggregator platform, PiQSuite, has an interesting take on why geopolitical flare-ups in Iran consistently fail to deliver the $100 oil that headline-chasers predict and there's a clear structural reason why.

Oil closed lower the week after the US bombed Iran's nuclear facilities in June 2025, with the initial 4-5% spike reversing within 48 hours as markets distinguished between dramatic headlines and actual supply disruption

The only credible path to US$100 oil is a genuine closure of the Strait of Hormuz but Iran is unlikely to act given ~90% of its own oil exports pass through the same waterway

Structural shifts have raised the bar for sustained price spikes: Western Hemisphere production now accounts for ~37% of global output (up from 26.7% in 1978), OPEC's share has fallen from 44% to ~34%, and China continues absorbing sanctioned barrels from Iran, Russia, and Venezuela

Options markets moved swiftly and efficiently, with the implied probability of Brent above $100 resetting from 17% to 9% within days of the June 2025 strikes, as the tail risk failed to materialise

Fundamentals remain the dominant price driver, with the EIA's January 2026 forecast expecting Brent to average US$56 for the year. This reflects a projected global supply surplus of 3.8 million barrels per day in 2026, slowing Chinese demand growth, and US shale near record highs

Energy shorts near decade highs

[9:14 am] An interesting chart from SubuTrade – S&P 500 Energy sector short interest remains near the highest in over a decade, heading into the US-Iran escalation.

Source: SubuTrade

A lot of varying commentary being thrown around:

JPMorgan: "Oil is rallying on risk, not tightness: physical signals eased as option skew surged. We map four Iran scenarios ... and keep our base case of Brent drifting towards ~US$60 as risk premia fade and balances soften."

Ed Yardeni: "We wouldn’t be surprised if any selloff in the S&P 500 on Monday morning turns into a rally, driven by expectations of lower oil prices once the latest Middle East war ends. The price of gold might also round-trip on Monday. Bond yields might fall due to both safe-haven demand and post-war prospects for lower oil prices."

ING Economics: "We still expect prices to ease with a surplus this year, but the downside now looks smaller ... Our Brent 2026 forecast revised up from US$57 to US$62."

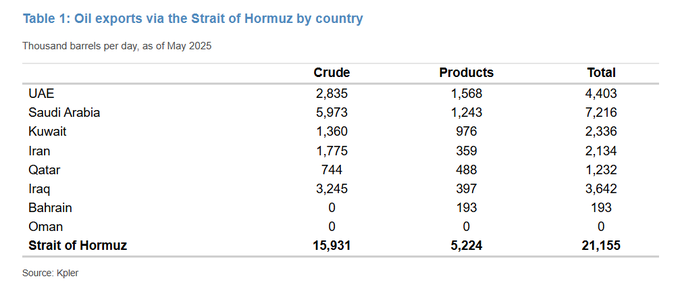

Strait of Hormuz closure threatens global energy markets

[9:03 am] Multiple sources have flagged the effective closure of the world's most critical oil choke-point. Here's what you need to know:

The Strait of Hormuz carries around 20 million barrels of crude per day (~20% of global consumption) and one-fifth of global LNG trade, with more than 80% of shipments destined for Asian markets including China, India, Japan and South Korea

At least 250 ships have dropped anchor across the Gulf and coasts of Oman and the UAE, Maersk has suspended all shipments through the strait, and war risk insurers are submitting policy cancellation notices

Brent crude is trading up 10% over the counter, with regional leaders warning that US$100 per barrel oil is a "clear and present danger"

A prolonged closure would hit Asian economies hardest given their import dependency, though the disruption would also severely damage Iran's own oil export revenues, which flow through the same waterway

According to JPMorgan, approximately 76% of oil exports via Hormuz goes towards Asia

China's exposure is the key geopolitical constraint on a full closure, as the largest buyer of Gulf crude. Beijing has significant leverage to pressure Tehran against a sustained shutdown, making a complete, long-term blockade unlikely but not impossible in the near term

Source: Kpler

US-Iran conflict escalates as markets brace for volatility

[8:55 am] No doubt the most important market event right now. US and Israeli strikes killed Iranian Supreme Leader Khamenei and dozens of senior officials over the weekend, triggering retaliatory Iranian attacks across the Gulf region and sending shockwaves through energy and equity markets.

Iran's Supreme Leader Khamenei has been killed in joint US-Israeli strikes, marking a historic escalation, a temporary leadership council is being formed while the Assembly of Experts determines a successor

Three US service members were killed and five seriously wounded, marking the first American casualties in the conflict

Oil markets are pricing in a widening escalation cycle, with Brent crude widely expected to approach the US$80 a barrel level

Tanker traffic through the Strait of Hormuz has all but halted, the world's largest shippers are cutting Gulf bookings, and DP World has suspended operations at its main Dubai port, raising the prospect of significant energy supply disruption

Emirates suspended flights indefinitely, Etihad and Qatar Airways have extended cancellations, and several Gulf airports were struck, with Abu Dhabi reporting one fatality from an intercepted drone

OPEC+ agreed in principle to a slightly larger production increase next month, a move likely aimed at cushioning any supply shock from the conflict

Source: Bloomberg

All things AI: OpenAI funding, Corewave and Amazon

[8:52 am] A landmark funding round for OpenAI headlined a busy week for AI news, though rising capex commitments and workforce displacement concerns kept sentiment mixed.

OpenAI closed $110bn in funding at a $730bn pre-money valuation ($840bn post-money), with Amazon contributing $40bn, SoftBank $30bn and Nvidia $30bn

The Amazon deal includes an agreement for OpenAI to use Trainium chips and spend an additional $100bn on AWS over eight years, though analysts flagged circularity concerns around the structure of these commitments

Microsoft confirmed its relationship with OpenAI remains unchanged, though the lack of detail did little to settle investor questions about the evolving partnership dynamic

CoreWeave flagged plans to spend $30-35bn in capex in 2026 against sales expectations of just $12-13bn, and will raise an additional $8.5bn in bank financing to fund capacity, adding to broader AI return-on-investment concerns

Block surged after announcing it would cut more than 4,000 staff, nearly half its workforce, citing AI's ability to automate more work with smaller teams, echoing displacement fears that weighed on markets earlier in the week

US wholesale inflation runs hot in January

[8:49 am] Producer prices jumped more than expected in January, with services costs leading the way and raising concerns about sticky inflation ahead of key PCE data due in March.

January core PPI up 0.8% month-on-month vs. 0.25% ests, and highest since March 2022, annual core PPI up 3.6% year-on-year vs. ests of 3.0%, highest since March 2025

Headline PPI up 0.5% month-on-month vs. 0.3% ests, highest since Sep-25, annual headline up 2.9% vs. 2.6% ests, though lowest since Oct-25

Services costs rose the most since July, with wholesaler margins posting the largest single-month gain in data going back to 2009, pointing to companies passing on tariff-related costs

Goods prices fell on cheaper gasoline and food, but ex-food and energy the increase was among the largest since early 2022, with metals, communications equipment and machine tools rising sharply

A volatile overnight session

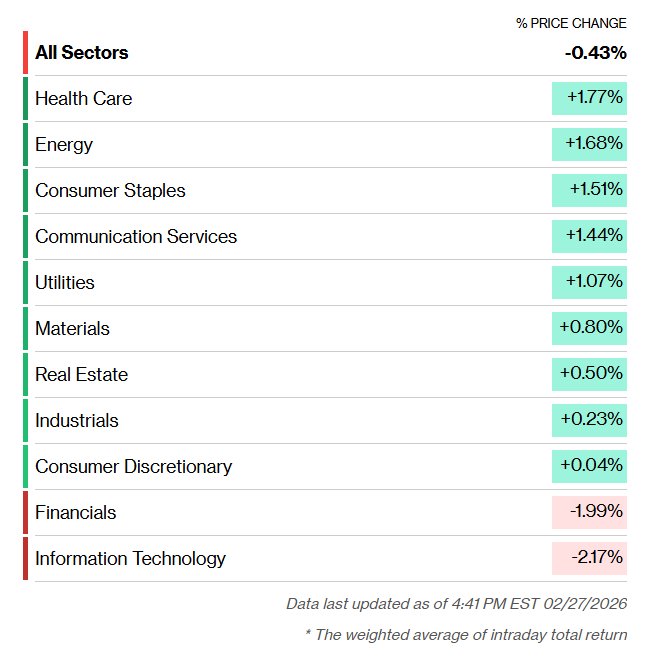

[8:47 am] A rather dicey overnight session, though the US-Iran situation occurred after market close. Major US benchmarks finished mostly lower, but bounced off intraday lows. S&P 500 (-0.43%), Dow (-1.05%), Nasdaq (-0.92%) and Russell 2000 (-1.68%) all weighed by sharp declines across tech and financials. This is despite nine out of eleven S&P 500 sectors closing the session in positive territory. Taking a closer look at the Dow, more stocks finished higher than lower, but heavyweights likes Goldman Sachs (-7.4%), Caterpillar (-1.3%) and Microsoft (-2.2%) weighed heavily on the price-weighted index.

S&P 500 sectors (Source: Bloomberg)

Good morning!

[8:30 am] ASX 200 futures are down 20 pts (-0.20%) as of 8:30 am AEDT.

The overnight session in a nutshell:

Major US benchmarks lower but off worst levels

Breadth was positive, with the Equal-weight S&P 500 (+0.12%) outperforming the cap-weighted benchmark by 55 bps

Nine out of eleven sectors traded higher, offset by sharp declines for Tech (-2.1%) and Financials (-1.9%)

US and Israel launched attacks on Iran over the weekend, with gold and oil prices expected to spike this morning

Middle East situation remains volatile, all eyes on the Strait of Hormuz (a key route for ~20% of global oil supply), where ~250 ships have dropped anchors and Maersk has suspended all shipments through the area