ASX 200 Live Today - Monday, 23rd March

The S&P/ASX 200 is set to enter correction territory as the Iran conflict continues to weigh on equity markets. Here's today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Monday, March 23. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

ASX 200 bounces off lows

[1:50 pm] ASX 200 currently down 0.66%, a strong reversal from intraday lows of -1.97%. The index's daily RSI has fallen to 29.3, its most oversold reading since 19 November, when the market shed roughly 7.5% over three week. This leaves the index in no man's land. A technical bounce looks overdue, yet the broader trend remains negative, with several headwinds still firmly in place, including: Australian 10-year yields sitting at 5.12%, Brent crude up 2.9% today to US$112.8, and ongoing escalation in Iran continuing to disrupt the Strait of Hormuz and key energy infrastructure. That last factor is feeding directly into bond yields, and markets have so far been reluctant to price in a worse outcome. The backdrop is difficult to argue against. Economists are now calling for three further RBA hikes, the likelihood of a Fed hike by year-end is increasingly being priced in, and it's worth remembering that the market's best days often occur right alongside its worst, this situation may prove no different.

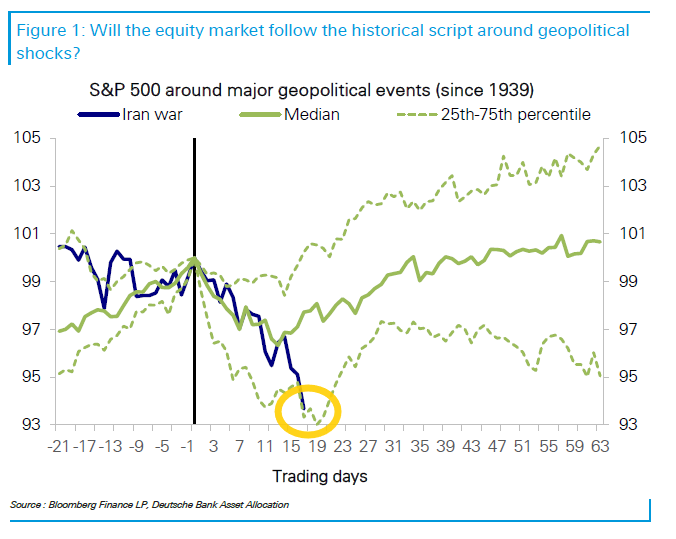

To close the blog on a more positive note, Deutsche Bank points out that the historical playbook for geopolitical shocks typically involves a sharp selloff of around 6–8%, with a bottom forming around the three-week mark and a full recovery in the three weeks that follow (well before the underlying event is resolved). In both size and timing, the current selloff is consistent with a typical bottom. Equities remain closely tied to oil prices, and a sustained drop in oil price volatility from current extremes would be an early signal that escalation risk is beginning to get priced in.

Banks continue to hold up

[12:55 pm] While the broader market continues to roll over, banks have slipped just 5.3% since the record close on 20-Feb. Even on days like this, the S&P/ASX 200 Banks Index is down just 0.5% (and bouncing strongly off session lows of -2.5%).

Ticker | Company | % Chg | Price |

|---|---|---|---|

BOQ | Bank Of Queensland | -1.81% | $6.79 |

NAB | National Australia Bank | -1.38% | $44.94 |

CBA | Commonwealth Bank | -0.52% | $174.72 |

JDO | Judo Capital | -0.52% | $1.53 |

WBC | Westpac | -0.44% | $40.52 |

MQG | Macquarie Group | -0.26% | $194.49 |

ANZ | ANZ | -0.22% | $36.52 |

BEN | Bendigo & Adelaide Bank | 0.10% | $10.06 |

Global LNG supply cliff: Gulf disruption leaves importers scrambling

[12:34 pm] Countries dependent on Gulf LNG face an imminent supply crisis as the last remaining cargoes from the region near their final destinations, according to the Financial Times.

Asian LNG prices (Platts JKM benchmark) have roughly doubled since the conflict began to around $23/MMBtu, with only one Gulf cargo still en route to Asia (which buys ~90% of the region's output) and six still headed to Europe

Pakistan is acutely exposed, with ~99% of its LNG previously sourced from Qatar; its two import terminals are operating at one-sixth capacity and will cease gas dispatch entirely by month end, with spot market prices too high to absorb

China (30% Gulf LNG exposure) and Japan (6% Hormuz exposure) are better positioned, with both pivoting toward coal and spot market purchases, while Japan is also leaning on nuclear after partially restarting the world's largest nuclear plant in Niigata

Taiwan moved quickly post-conflict to secure 22 replacement cargoes through to end of April, but flags the risk of severe energy shortages if the Strait remains closed heading into peak summer demand

What's catching a bid?

[12:33 pm] Markets are bleeding but what's catching a bid? The below table observes the S&P/ASX 200 stocks that have gained the most since market open. A clear bid for a few risk-oriented pockets of the market like 4DMedical, Dateline Resources and Zip.

Ticker | Company | % Chg from Open | Price |

|---|---|---|---|

DTR | Dateline Resources | 10.59% | $0.47 |

L1G | L1 Group | 8.61% | $1.10 |

PMV | Premier Investments | 6.88% | $12.42 |

4DX | 4DMedical | 6.57% | $4.38 |

MFG | Magellan Financial Group | 5.81% | $10.20 |

AUB | AUB Group | 5.20% | $23.47 |

PNI | Pinnacle Investment Management | 5.15% | $13.18 |

ZIP | Zip | 5.12% | $1.48 |

APE | Eagers Automotive | 4.87% | $20.99 |

REH | Reece | 4.85% | $13.63 |

Gold miners down 36% in three weeks

[11:48 am] It's a sea of red for gold names, hit with a double whammy of lower gold prices from the overnight and current session. The All Ords Gold Index is now down 36% since its 2 March record high.

Ticker | Company | % Chg | Price |

|---|---|---|---|

CYL | Catalyst Metals | -12.46% | $5.76 |

BC8 | Black Cat Syndicate | -11.18% | $0.94 |

OBM | Ora Banda Mining. | -11.02% | $1.05 |

PNR | Pantoro Gold | -10.71% | $3.00 |

ALK | Alkane Resources | -10.71% | $1.38 |

RSG | Resolute Mining | -8.97% | $1.20 |

MEK | Meeka Metals | -8.13% | $0.15 |

NEM | Newmont | -7.76% | $131.41 |

AMI | Aurelia Metals | -7.66% | $0.22 |

EVN | Evolution Mining | -7.49% | $11.48 |

EMR | Emerald Resources | -7.34% | $4.61 |

BGL | Bellevue Gold | -7.10% | $1.28 |

CMM | Capricorn Metals | -7.01% | $9.55 |

WGX | Westgold Resources | -6.99% | $4.92 |

NST | Northern Star Resources | -6.76% | $17.25 |

VAU | Vault Minerals | -6.57% | $3.63 |

RRL | Regis Resources | -6.14% | $5.81 |

RMS | Ramelius Resources | -5.73% | $3.29 |

PRU | Perseus Mining | -5.61% | $4.54 |

SBM | St. Barbara | -5.22% | $0.55 |

GMD | Genesis Minerals | -4.80% | $5.36 |

Gold continues to slide

[11:46 am] Gold has continued to slide on Monday, despite suffering its largest weekly decline last week. Bullion prices briefly traded positive this morning, now down 2.9% to US$4,359/oz. Prices are now up just ~0.5% year-to-date but still trading 3.5% away from the key 200-day moving average.

Real Estate stocks back at January 2024 levels

[11:01 am] The S&P/ASX 200 Real Estate Index is down 1.8% today, having fallen seven of the last nine sessions. It's also in 'bear market' territory, having declined ~23.6% since last October, trading at the lowest since January 2024.

S&P/ASX 200 Real Estate Index (Source: TradingView)

Tech hits lowest since October 2023

[10:58 am] The S&P/ASX 200 Tech Index is down 2.9%, now having undercut the recent low (24-Feb) to trade at the lowest since October 2023. The index managed to bounce ~14.7% between 24-Feb and 2-March but has since given back all of its gains.

S&P/ASX 200 Tech Index chart (Source: TradingView)

Miners near four-month lows

[10:54 am] The S&P/ASX 200 Materials Index is currently down 3.7%, trading below the 200-day moving average for the first time since August 2025.

Since the technical definition of a 'bear market' is a decline of 20% of more ... the Materials Index is also in bear market territory having suffered a ~23.5% decline from its 2 March record high.

S&P/ASX 200 Materials daily chart (Source: TradingView)

All Ords and Emerging Companies indices enter bear market

[10:22 am] The S&P/ASX Small Ords and Emerging Companies indices have dipped 3.0% and 3.8% respectively in early trade. Both indices are now down just over 20% since their 23-Jan-26 record highs, officially entering bear market territory.

S&P/ASX Emerging Companies Index (Source: TradingView)

Top ASX 200 gainers

[10:15 am] Viva Energy and Ampol, which own Australia's only two remaining refiners, continue to grind higher. Santos and Woodside also cautiously higher. Surprised to see Life360 and Block eke out a small gain, though both stocks are down 42% and 13% respectively.

Ticker | Company | % Chg | Price |

|---|---|---|---|

VEA | Viva Energy | 2.97% | $2.43 |

360 | Life360 | 2.10% | $18.46 |

XYZ | Block | 1.97% | $84.49 |

ALD | Ampol | 1.36% | $33.56 |

STO | Santos | 1.25% | $8.08 |

IFL | Insignia Financial | 1.17% | $4.75 |

MPL | Medibank Private | 1.07% | $4.26 |

WDS | Woodside Energy Group | 0.91% | $34.35 |

AUB | AUB Group | 0.89% | $22.78 |

MEZ | Meridian Energy | 0.88% | $4.56 |

Top ASX 200 losers

[10:15 am] Eight of the ten top decliners are all gold miners as bullion prices fell 3.5% overnight to US$4,491 an ounce.

Ticker | Company | % Chg | Price |

|---|---|---|---|

CYL | Catalyst Metals | -9.27% | $5.97 |

ALK | Alkane Resources | -7.79% | $1.42 |

EOS | Electro Optic Systems | -7.37% | $9.17 |

RSG | Resolute Mining | -6.84% | $1.23 |

OBM | Ora Banda Mining | -6.78% | $1.10 |

GGP | Greatland Resources | -6.53% | $9.45 |

LTR | Liontown | -6.05% | $1.37 |

BGL | Bellevue Gold | -5.80% | $1.30 |

PDI | Predictive Discovery | -5.77% | $0.74 |

EVN | Evolution Mining | -5.64% | $11.71 |

ASX 200 dips to fresh 10-month low

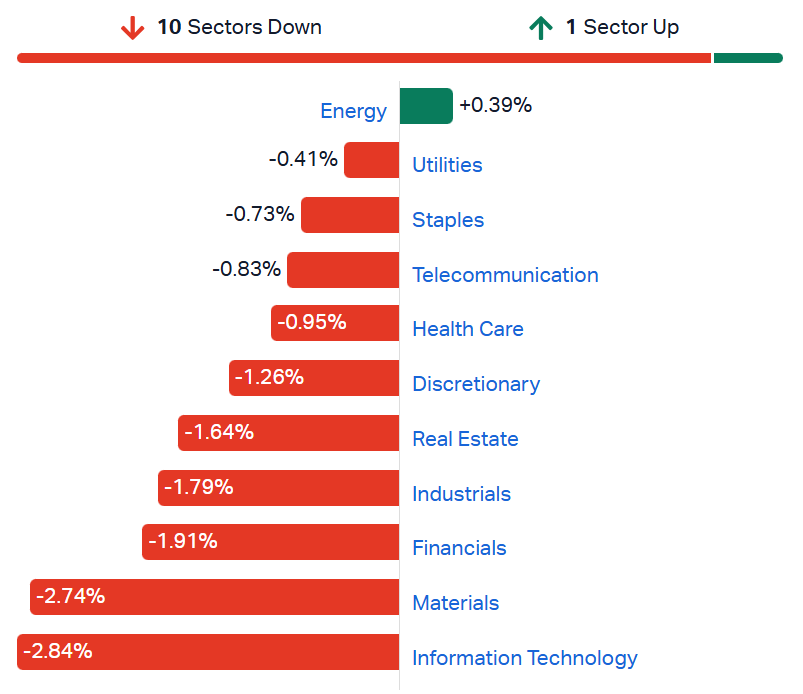

[10:05 am] It is carnage out there – the ASX 200 is currently down 1.84%, trading at the lowest since 15 May, 2025. The index has now dipped 4.3% in the last three sessions and official enters correction territory, down 10.1% since its 2 March record high.

Broad selling across sectors, with only Energy trading higher, while defensives like Utilities, Staples and Telcos outperform on a relative basis.

S&P/ASX 200 sectors (Source: Market Index)

St Barbara flags limited diesel exposure at Simberi

[9:44 am] With little corporate commentary from ASX miners on the impact of soaring diesel prices, St Barbara is one of the first to detail its fuel position at the PNG gold project.

Simberi currently consumes approximately 65,000 litres of diesel per day for mining and power generation. The company has around 4.7 million litres stored on the island, covering more than two months of operations, with an additional 3.5 million litres held at Lae and Port Moresby

Of the total 8.2 million litres in storage, 6.4 million litres have been locked in at pre-conflict pricing. The remaining 1.8 million litres at Lae will be priced at end of March, exposing a small portion to current elevated diesel costs

New Hope is the only other company that comes to mind regarding diesel commentary. At its 1H26 result, the company noted:

Diesel only accounts for ~13% of costs

No near-term supply risks identified

Coal price increases to significantly outweigh diesel cost pressures

Closely monitoring diesel and other input costs

St Barbara progresses Simberi transactions

[9:37 am] St Barbara has confirmed the Lingbao and Kumul transactions are expected to close in early April, triggering FID on the new Simberi gold project.

Chinese and PNG regulatory approvals for the Simberi transactions were completed in March, with completion of the Lingbao and Kumul deals planned for the first days of April

Final investment decision on the new Simberi gold project triggered on the same date as transaction completion

Company page: St Barbara (SBM)

Macmahon secures ~$250m LOI for Mount Carlton gold mine restart

[9:33 am] Macmahon has executed a Letter of Intent with Wolfram (a subsidiary of Bumi Resources) for surface and underground mining services at the Mount Carlton Gold Mine in North Queensland, with a contract worth approximately $250 million over an initial 33-month term expected to be finalised shortly.

Early works have already commenced, with surface mining set to restart in April 2026 and underground mining to follow, requiring no additional capital beyond the existing FY26 budget.

Company page: Macmahon Holdings (MAH)

Brent opens ~2% higher

[9:26 am] Brent is currently up 2.1% to US$111.86 a barrel, though prices will no doubt remain highly volatile. Here's a recap of how prices have performed since late February.

Date | % Chg | Close (US$) |

|---|---|---|

27/02/26 | 3.42% | $73.20 |

2/03/26 | 6.67% | $78.08 |

3/03/26 | 4.96% | $81.95 |

4/03/26 | 0.76% | $82.57 |

5/03/26 | 2.10% | $84.30 |

6/03/26 | 10.71% | $93.33 |

9/03/26 | 6.03% | $98.96 |

10/03/26 | -7.65% | $91.39 |

11/03/26 | 2.44% | $93.62 |

12/03/26 | 8.69% | $101.76 |

13/03/26 | 2.08% | $103.88 |

16/03/26 | -2.76% | $101.01 |

17/03/26 | 2.48% | $103.51 |

18/03/26 | 5.92% | $109.64 |

19/03/26 | -1.88% | $107.58 |

20/03/26 | 1.84% | $109.56 |

23/03/26 | 2.10% | $111.86 |

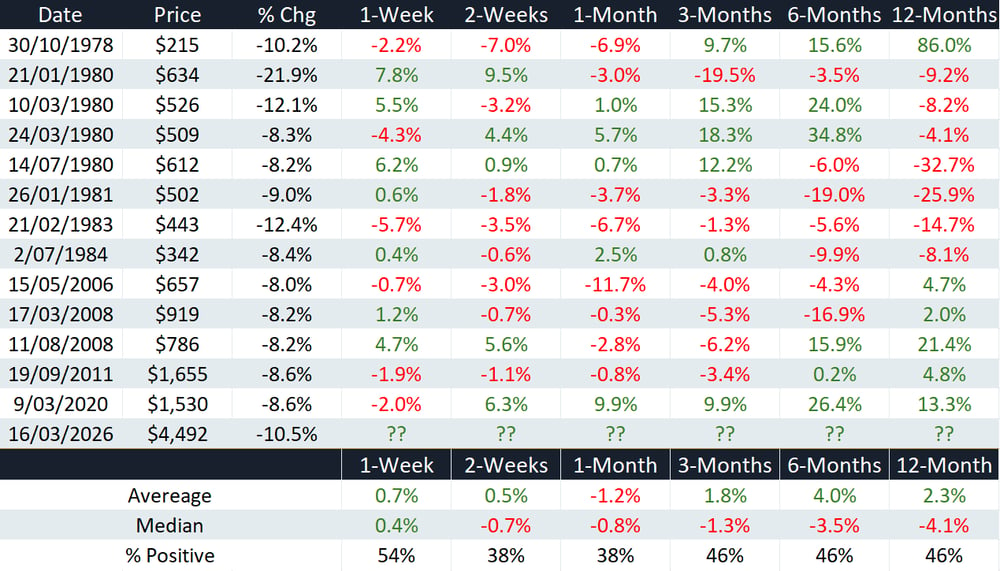

Gold suffers worst weekly decline since 1983

[9:23 am] Gold prices tumbled 10.5% last week, far outpacing the ~8% decline bullion experienced during the pandemic and GFC. This marks the worst weekly selloff since 1983, where prices tumbled 12.4%. Here's a look at how gold performs after large weekly selloffs.

Source: Author's own calculations

Bond yields continue to soar

[9:19 am] The Aussie 10-year yield has opened 10 bps higher this morning to 5.17%, the highest since June 2011. It's now surged 53 bps since 27 February. Not a good look for interest rate expectations and equity markets.

Australia 10-year yield (Source: TradingView)

Phosphate fertiliser crisis looms as Middle East war threatens sulfur supply

[9:04 am] The war in the Middle East is creating a second front in the global fertiliser crisis, with phosphate supplies now under serious threat due to the region's outsized role in sulfur production.

Almost half of global sulfur supply, a critical input for processing phosphate fertiliser, comes from Middle Eastern countries exposed to Strait of Hormuz disruptions, compounding what was already a tight market with sulfur prices at record highs

The supply chain effects could become "exponential" if the conflict continues, once producers exhaust existing sulfur and sulfuric acid reserves

Phosphate was already under pressure before the war, with Russian exports constrained by the Ukraine conflict, China curbing shipments to prioritise domestic use, and US duties on Moroccan phosphate still in place

India's typical ramp-up in phosphate purchases from April could push the market into "panic mode", while mining companies competing for scarce sulfur can outbid fertiliser producers

Trump's 48-hour ultimatum raises stakes

[9:00 am] It was a classic Trump weekend where he said "I don't want to do a ceasefire with Iran", followed by "considering winding down" just a few hours later, then planning "peace talks", followed by a threat to obliterate Iran's power plants if they don't open the Strait of Hormuz within 48 hours.

Trump threatened overnight to "obliterate" Iran's power plants if Tehran did not fully reopen the Strait of Hormuz within 48 hours, barely a day after floating the idea of winding down the war

Iran's Revolutionary Guards responded that the strait would remain completely closed until any destroyed power plants are rebuilt

In a separate Truth Social post, Trump said the US is "getting very close" to meeting its objectives and considering winding down military efforts

He suggested other nations should guard the strait, stating "the United States does not" use it

The Hormuz crisis has Trump in a bind. He originally wanted the war wrapped up by the end of March, but the strait closure has forced an extension. Options like seizing Kharg Island are being discussed, though allies have largely refused to contribute forces, prompting Trump to call NATO countries "cowards"

Iran fired its first known long-range ballistic missiles with a 4,000km range at a US-British Indian Ocean military base on Friday, expanding the risk of attacks well beyond the Middle East

Super Micro co-founder indicted for smuggling Nvidia AI chips to China

[8:57 am] Super Micro shares plummeted 33% after a federal indictment alleged co-founder Wally Liaw and two others used fake paperwork and dummy servers to illegally export Nvidia GPU-equipped servers to China.

The scheme allegedly generated ~$2.5bn in sales for Super Micro since 2024, with $510m in shipments between late April and mid-May 2025 routed through a Southeast Asian middleman to conceal the China destination

Defendants allegedly used dummy servers at storage facilities to deceive compliance teams and even a visiting US export control officer, while real servers were forwarded to China without the required Commerce Department licence

Liaw has resigned from the board and been placed on administrative leave alongside sales manager Steven Chang, while contractor Willy Sun has been dropped by the company

Source: CNBC

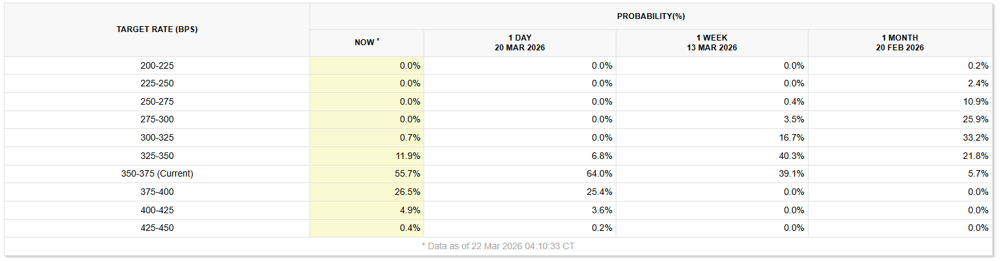

Fed now more likely to hike than cut

[8:56 am] The likelihood of one 25 bp hike was non-existent a week ago, now it's 26.5%, according to CME's Fedwatch Tool.

Source: CME Fedwatch Tool

Fed officials signal rate cuts still in play despite war uncertainty

[8:51 am] Fed Vice Chair Bowman and Governor Waller both indicated rate cuts remain possible this year, though flagged the Iran conflict and inflation as key risks to the outlook.

Bowman said she still sees three rate cuts before year-end and expects strong economic growth, though noted it is too early to assess the full impact of the Iran conflict

Waller struck a more cautious tone, saying cuts are possible if the labour market continues to weaken and inflation stays contained, but flagged four negative payrolls prints out of the last five as a concern

Waller also warned that if tariff-linked inflation does not roll off by mid-year, it could create a challenging policy environment for the Fed

Comments follow Wednesday's FOMC hold and median dot plot projection of 25bp of cuts this year, with only two officials forecasting three cuts and one forecasting four

Markets have moved sharply hawkish in response, with CME FedWatch now pricing in 17 bp of rate hikes by year-end, a notable divergence from the dovish tone of both officials

FedEx beats across the board, raises full-year guidance

[8:50 am] Probably one of the only noteworthy results to have come out overnight. FedEx delivered a strong fiscal Q3 with earnings and revenue comfortably ahead of expectations, though the stock finished the session up just 0.7%, despite rallying as much as 7.5% in early trade.

Revenue of $24bn vs. $23.43bn ests (2% beat)

Net income of $1.06bn, up 17% from $909m in the prior year

Adjusted EPS of $5.25 vs. $4.09 ests (28% beat)

FY26 adjusted EPS guidance raised to $19.30-$20.10, up from prior range of $17.80-$19.00, with revenue growth now expected at 6-6.5% vs. 5.6% ests

Network 2.0 cost savings now expected to exceed the original $1bn target, driven by automation and AI-led efficiencies

Asian buyers snap up US oil at three-year high

[8:48 am] The closure of the Strait of Hormuz due to the US-Israel-Iran conflict has triggered a surge in Asian purchases of American crude, with April-loading volumes hitting roughly 60 million barrels, the most since April 2023.

Asian refiners nearly doubled their US crude purchases from ~35m barrels per month in January-February to ~60m barrels for April loadings

Pricing has surged sharply, with premiums over Dubai jumping to ~$18/bbl from $5-$6/bbl last month, while one Taiwan cargo was priced at $12-$13/bbl above Dated Brent

Shipping markets are strained, with vessel bookings spiking and traders resorting to smaller Aframax tankers instead of the typical VLCCs due to capacity constraints

Source: Bloomberg

Iran strikes cripple Qatar's LNG exports

[8:46 am] The latest Iranian missile attack on Qatar's Ras Laffan facility has knocked out 17% of the country's LNG export capacity, with repairs expected to take up to five years.

Trains 4 and 6 at Ras Laffan were severely damaged, representing 12.8 million tons of annual LNG production capacity. QatarEnergy estimates approximately $20bn in lost revenue over the repair period

QatarEnergy has declared force majeure on some long-term contracts for up to five years, directly impacting buyers in China, South Korea, Italy and Belgium

The adjacent Pearl gas-to-liquids facility, operated by Shell, is expected to be offline for at least one year. Both damaged trains are joint ventures with ExxonMobil

Beyond LNG, Qatar also expects to lose approximately 18.6 million barrels of condensates production (24% of exports), 13% of LPG exports and 14% of helium exports

Source: Bloomberg

A rough session on Wall Street

[8:44 am] That's not the kind of lead in you want if you're looking for a bounce.

Major US benchmarks broadly lower overnight and closed near worst levels

S&P 500 (-1.51%), Dow (-0.96%), Nasdaq (-2.01%), Russell 2000 (-2.26%)

US weekly recap: Russell 2000 (-1.68%), S&P 500 (-1.90%), Nasdaq (-2.07%), Dow (-2.11%)

Fourth consecutive weekly loss for all four US indices

S&P 500 and Nasdaq both closed below their 200-day moving averages for the first time since May 2025

US 10-year yield up 13.5 bps to 4.38%, the highest since August 2025

Yield-sensitive sectors smashed overnight, with Utilities (-4.1%), Real Estate (-3.1%) and Tech (-2.2%) trading sharply lower

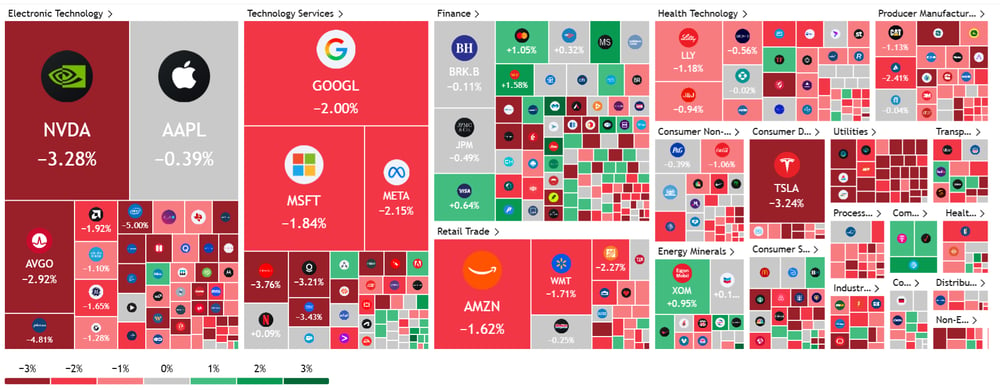

S&P 500 heatmap (Source: TradingView)

S&P 500 daily chart (Source: TradingView)

Good morning!

[8:33 am] ASX 200 futures are down 156 pts (-1.86%) as of 8:30 am AEDT.

The overnight session in a nutshell:

The local sharemarket is set to open near a fresh 10-month low, potentially entering correction territory

US indices dropped sharply overnight as bond yields jumped broadly, with the 10-year yield climbing 13 bps to its highest level since August 2025

Gold closed out the week down 10.5%, its worst weekly selloff since 1983, far exceeding the 8–9% declines seen during the pandemic and GFC

The Iran conflict remains volatile after a flurry of mixed remarks from Trump over the weekend that pointed to both de-escalation and escalation