ASX 200 Live Today - Monday, 15th December

The S&P/ASX 200 is set to fall after a weak lead from Wall Street and pullback in commodities. Here are today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Monday, December 15. Expect a high volume of posts pre-market and more periodic updates throughout the day. It'll wrap up around 2:00 pm AEST. Be sure to refresh manually for the latest updates — and let us know how we can make it even better.

ASX 200 lower amid miner pullback

[2:05 pm] ASX 200 trading 0.70% lower, a rather sharp pullback after the sizeable 1.23% rally last Friday. The Materials sector is a large outlier today, down 2.0% and giving back the entirety of Friday's gains. This weakness may be exacerbated by some of China's property woes (Vanke debt restructuring jitters) and some natural selling pressure after the sector moved out after trading sideways for four years. The market is still trying to find a low against a dicey backdrop of elevated yields and AI-related weakness. Last Friday's session was encouraging, and ideally, the market shows some form of bounce after today's pullback. Otherwise, it runs the risk of dipping back below the 200-day.

UBS sees 2026 as the year for base metals and critical minerals

[12:47 pm] Gold, copper and critical minerals outperformed in 2025 amid geopolitical uncertainty, tight supply, and supply-chain decoupling efforts, while bulk commodities lagged. UBS highlights lithium, gold, copper and aluminium as key picks for 2026, driven by structural demand and constrained supply.

Copper expected to face supply tightness in 2026, pushing the market into deficit and driving sustainable price upside

Aluminium remains constructive with China’s 45Mt cap limiting supply versus growing demand, though alumina prices are near the cost curve with limited upside

Lithium demand from battery energy storage systems (BESS) to create deficits mid-CY26, with prices forecast at US$1,800/t (US$2,850/t SC6) in CY26/27

Gold remains constructive with structural private and official demand supporting upside risk over the next 12 months

Bulk commodities: iron ore expected around US$100/t near term, trending to ~$90/t by 2027; metallurgical coal and thermal coal prices to moderate or remain range-bound, uranium outlook positive on policy support and Big Tech buy-in

Uranium stocks broadly lower

[11:51 am] Quite a broad pullback for uranium stocks, though not surprising given the overnight lead (URA ETF down 6.0%).

Ticker | Company | % Chg | Price |

|---|---|---|---|

PEN | Peninsula Energy | -8.70% | $0.53 |

DYL | Deep Yellow | -7.39% | $1.79 |

BMN | Bannerman Energy | -6.68% | $3.15 |

EL8 | Elevate Uranium | -6.67% | $0.25 |

BOE | Boss Energy | -6.21% | $1.66 |

NXG | Nexgen Energy.s | -4.93% | $13.50 |

LOT | Lotus Resources | -4.57% | $0.17 |

PDN | Paladin Energy | -4.47% | $8.97 |

RBC's take on Fortescue

[11:24 am] Fortescue announced its plans to acquiring the remaining 64% of Alta Copper to strengthen its long-term copper optionality. Here are the key takeaways from RBC's analyst Kaan Peker.

Offer represents a 50% premium to 30-day VWAP, with unanimous board support and voting agreements covering 12.5% of shares (16% including options)

Alta Copper’s Cañariaco project in Peru holds ~1.1Bt M&I resources @ 0.42% CuEq and ~0.9Bt inferred @ 0.29% CuEq, providing long-life, large-scale copper optionality

Transaction is strategic rather than earnings-driven as value lies in portfolio depth, scale optionality, and Fortescue’s ability to advance permitting, drilling, and JORC conversion

Intraday gainers

[11:21 am] The intraday gainer scan observes the stocks experiencing the largest gain from today's open. A handful of resources stocks appear to be bouncing, namely gold, coal and lithium names. Neuren has posted the largest intraday gain after its partner Acadia Pharmaceuticals announced the FDA approval of its DAYBUE STIX (trofinetide) for oral solution.

Ticker | Company | % Chg | Price |

|---|---|---|---|

NEU | Neuren Pharmaceuticals | 3.97% | $19.76 |

DRO | Droneshield | 3.81% | $2.18 |

OBM | Ora Banda Mining | 3.59% | $1.36 |

ZIM | Zimplats | 3.20% | $18.68 |

WHC | Whitehaven Coal | 2.59% | $7.74 |

MND | Monadelphous Group | 2.26% | $26.27 |

MIN | Mineral Resources | 2.23% | $52.73 |

ASB | Austal | 1.93% | $6.35 |

ANZ | ANZ Group | 1.92% | $36.32 |

GGP | Greatland Resources | 1.86% | $9.32 |

Top ASX 200 gainers and losers

[10:17 am] Droneshield tops the leaderboard, likely boosted by peer EOS securing a ~$120m weapons deal with Korea. Most other gainers are modest, up just 1–2%, while a number of resource-related stocks have fallen 2–3% following a broad overnight pullback in the commodity sector.

Ticker | Company | % Chg | Price |

|---|---|---|---|

DRO | Droneshield | 4.81% | $2.18 |

ZIM | Zimplats | 2.18% | $18.31 |

XYZ | Block | 2.06% | $97.17 |

LTR | Liontown | 1.82% | $1.51 |

JHX | James Hardie | 1.68% | $30.94 |

NEU | Neuren Pharmaceuticals | 1.63% | $19.32 |

REG | Regis Healthcare | 1.48% | $7.55 |

CHC | Charter Hall Group | 1.28% | $25.39 |

PMV | Premier Investments | 1.20% | $14.34 |

MPL | Medibank Private | 1.07% | $4.74 |

Ticker | Company | % Chg | Price |

|---|---|---|---|

GNE | Genesis Energy | -5.02% | $2.08 |

NXG | Nexgen Energy | -4.86% | $13.51 |

TLX | Telix Pharmaceuticals | -4.80% | $13.08 |

PDN | Paladin Energy | -4.69% | $8.95 |

FBU | Fletcher Building | -3.42% | $3.11 |

MP1 | Megaport | -3.08% | $12.77 |

ASX | ASX | -2.95% | $55.21 |

GMD | Genesis Minerals | -2.75% | $6.71 |

GLF | Gemlife Communities | -2.73% | $4.98 |

SLX | Silex Systems | -2.62% | $8.18 |

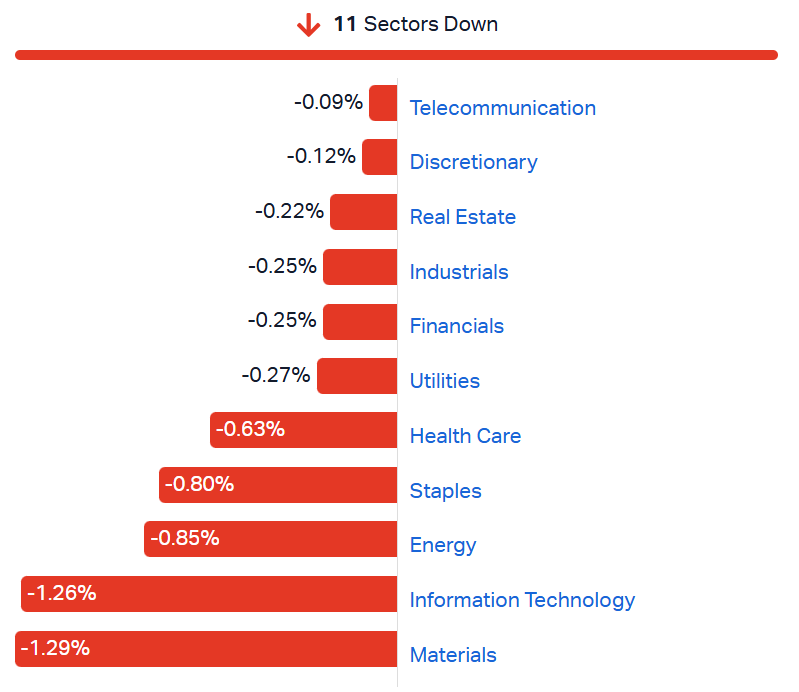

ASX 200 lower, all sectors red

[10:15 am] ASX 200 down 0.50% in early trade, all sectors lower, with Tech and Materials leading the downside move.

ASX 200 sectors (Source: Market Index)

Macquarie downgrades CSL, slashes target price

[9:40 am] Macquarie downgraded CSL to Neutral (from Overweight) and cut its target price by 32% from $275.20 to $188.00. The investment bank has been Outperform rated on CSL for more than three years.

The key takeaways from the report include:

CSL’s share price has nearly halved since the COVID period, weighed down by recent R&D setbacks, structural shifts including China albumin, and a string of downgrades that have framed the company as ex-growth.

The core Behring franchise is under increasing pressure, initially from FcRn antagonists and now complement inhibitors, while declining US vaccination volumes signal risks extending beyond FY26.

Analysts estimate that roughly 25% of CSL’s immunoglobulin (IG) share in CIDP could be at risk, potentially reducing EPS by around 4% by FY33.

Looking ahead, CSL faces potential risk to its FY26 guidance, with the second half heavily dependent on mitigating the effects of China’s albumin market.

Uranium stocks set to tumble

[9:36 am] The Global X Uranium ETF (URA) suffered a 6.0% dip last Friday. No major catalyst behind this move besides broader market weakness and a pullback for the commodity sector.

A dual-listed name like NexGen finished the overnight session down 5.5%. It wouldn't be surprising to see a sizeable pullback for most local names this morning.

Fortescue moves to fully acquire Alta Copper

[9:26 am] Fortescue will buy the remaining 64% of Alta Copper it does not already own, in a deal valued at C$139m. Given the size of the transaction, this is relatively immaterial to Fortescue.

Alta Copper’s directors unanimously recommend shareholders vote in favour, supported by 12.5% of shares under voting agreements

Haywood Securities and Fort Capital Partners confirm the offer is financially fair to Alta shareholders

Transaction expected to close in the March quarter of 2026

Company page: Fortescue (FMG)

ASX pledges reforms after inquiry flags governance and culture issues

[9:20 am] The ASX has committed to a series of reforms following an interim inquiry report, addressing governance, culture and financial resilience concerns.

Inquiry found ASX prioritised short-term performance over obligations as critical national market infrastructure and lacked long-term strategic vision

Defensive organisational culture and governance gaps were highlighted, including insufficient independence and investment oversight in Clearing and Settlement subsidiaries

Current supervisory practices were deemed ineffective in achieving desired outcomes

Reforms include strengthening independence and governance of Clearing and Settlement boards, a strategic reset of the ‘Accelerate’ transformation program with clear milestones, and stronger leadership accountability

An additional A$150m capital charge imposed to ensure ASX maintains robust financial resources until remediation is complete

This outcome is hardly surprising given recent events: i) Halted TPG when the market sensitive announcement was referring to TPG Capital Asia; ii) publishing outage halted over 50 stocks on 1 December; iii) removed staggered opening earlier this year to lower volatility and improve liquidity (when in reality its increased volatility and worsened liquidity) and more.

Company page: ASX (ASX)

Australia targets supermarket price gouging with new laws

[9:15 am] The government has introduced regulations to curb excessive pricing in groceries, alongside broader measures to improve competition, transparency and food security.

New law bans very large retailers from charging prices deemed excessive relative to supply cost plus a reasonable margin, taking effect 1 July 2026

Maximum penalty per contravention is the greater of $10m, three times the benefit gained, or 10% of prior-year turnover if benefit cannot be determined

Food and Grocery Code to become mandatory from 1 April 2025, with ACCC funding boosted by over $30m to enforce consumer protections

Government will consult on strengthening Unit Pricing Code, implement ACCC recommendations on price transparency, and fund CHOICE to inform shoppers

Source: ALP

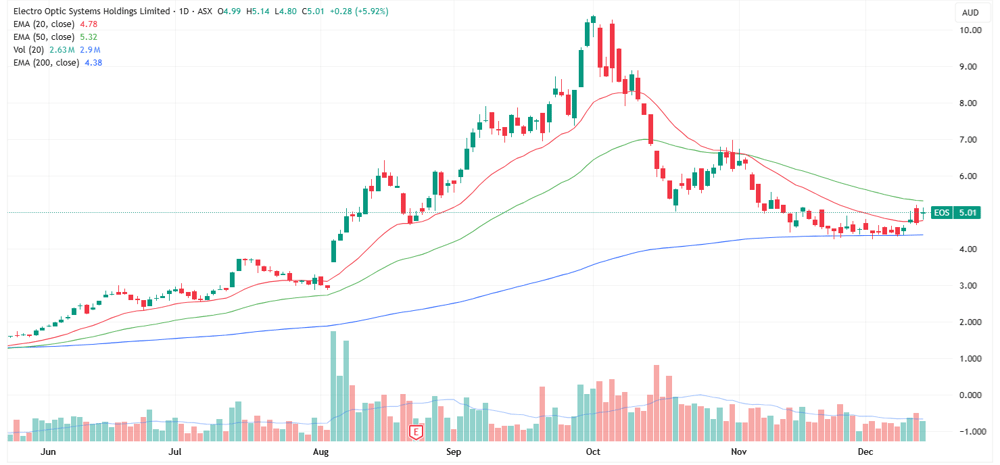

EOS secures conditional $120m Korean laser weapons deal

[9:13 am] Electro Optic Systems signed a binding conditional agreement with a Korean customer, marking a potential step-change contract tied to high energy laser defence systems.

Total contract value of US$80m (A$120m)

Scope includes manufacture and sale of a 100kW high energy laser weapon, with delivery scheduled for end 2027

Agreement includes the establishment of a joint venture to develop and supply 100kW laser weapons into the Korean market

EOS would license intellectual property for the 100kW laser system to the Korean joint venture, expanding its regional footprint

Fulfilment contingent on delivery and successful post-delivery demonstrations, pushing revenue recognition beyond FY27

EOS experienced a massive ~750% run up between May and October, but now down around ~52% from recent highs. The stock has managed to find some support around the 200-day moving average.

Large contract wins once drove outsized share price gains, but market reactions have become more volatile following the re-rate and higher valuation backdrop. For example, EOS reported a $108m contract win on 6 October, where the stock opened 16.1% higher but finished the session up just 2.5%. It'll be interesting to see how it trades following the recent pullback.

Company page: Electro Optic Systems (EOS)

China's housing giant loses state support

[9:04 am] Vanke’s debt crisis deepened after its key state-backed shareholder capped funding and demanded collateral, shattering assumptions of an implicit rescue and accelerating market fallout.

Shenzhen Metro imposed limits on further financing and required collateral on existing loans, signalling waning state tolerance and triggering a sharp reassessment of Vanke’s solvency

Dollar bonds have collapsed to around 20 cents, state banks are cutting exposure and regulators are shifting focus from rescue to containing systemic risk

CICC concluded Vanke was insolvent in the third quarter, while regulators later indicated the state would not step in, effectively abandoning the “too big to fail” narrative

More than $50bn of debt is now in play, around 45% unsecured, raising the likelihood of a complex, multi-year restructuring with losses for domestic and offshore creditors

The crisis threatens broader confidence in China’s property sector, even as its share of economic output has fallen, with policymakers scrambling to stabilise housing demand amid growing censorship and market anxiety

The outcome leaves Vanke needing to repay the note by Monday or within a five business day grace period, or negotiate an alternative agreement to avoid a technical default.

The setback highlights the depth of China’s prolonged property downturn, now in its fifth year, which has already seen high profile collapses at Evergrande and Country Garden.

This is not a good look for the iron ore sector. Last Wednesday, China-listed property developers rallied on renewed policy optimism and signs of progress in Vanke’s debt restructuring. Vanke shares rallied almost 20% on the Hang Seng while most developers gained ~3-5%.

This 180 will likely place some downward pressure on the names like BHP, Fortescue etc.

Ioneer eyes strategic US boron deal as funding hunt continues

[8:55 am] Ioneer has flagged interest in bidding for Rio Tinto’s US boron assets, viewing the potential divestment as a strategic opportunity to consolidate boron and lithium operations across Nevada and California.

Chief executive Bernard Rowe said there are “a lot of synergies” between Ioneer’s Rhyolite Ridge project in Nevada and Rio’s boron assets in California, which Bloomberg reported in November are heading towards a sale process.

Boron was added to the US critical minerals list last month, given its applications across fertilisers, industrial materials, rare-earth magnets and electronics. Rio’s California operations, which include mining, processing, refining and port infrastructure, account for roughly 30% of global boron supply.

Alongside the potential acquisition, Ioneer is continuing its search for new funding partners after Sibanye Stillwater exited plans to take a major stake in Rhyolite Ridge earlier this year.

Source: Bloomberg

Busy day for Fedspeak

[8:49 am] Lots of commentary over the weekend from key Fed policymakers, highlighting diverging views on inflation persistence, labour market risks and how restrictive policy should remain.

Goolsbee said delaying further rate cuts carries little risk and allows time for more data, remains uneasy about inflation being fully transitory but expects rates to fall significantly over the next year and is projecting more cuts than the median for 2026

Schmid argued conditions have not shifted materially since November, warned inflation uncertainty could push up long-term rates and prefers policy to stay modestly restrictive to contain inflation pressures

Paulson said the labour market remains sound but downside risks are rising, is more concerned about employment weakness than inflation upside and sees a good chance inflation eases through 2026 as tariff effects fade mid-year

Hammack said policy is now around neutral but, given risks on both sides of the mandate, favours keeping settings slightly restrictive

Broadcom dips despite solid earnings

[8:45 am] Broadcom delivered a clean quarterly beat and raised guidance on surging AI demand, but the stock dipped 11.4% as the market focused on its ballooning valuation and limited FY26 visibility.

Revenue up 28% to $18.02bn vs. $17.47bn ests (3.1% beat)

Adjsuted EBITDA of $12.22bn vs. $11.69bn ests (4.5% beat)

Quarterly dividend up 10% to 65 cps, targeting FY26 annual dividend of $2.60 per share (15th consecutive annual increase)

1Q26 revenue guidance of $19.1bn vs. $18.48bn ests (3.4% beat)

1Q26 adjusted EBITDA guidance to be 67% of projected revenue

Other takeaways: Additional $11bn order from Anthropic, fifth XPU customer with a $1bn order for late 2026 and massive $73bn backlog

Management commentary:

“Accordingly, in Q1, we forecast non AI semiconductor revenue to be approximately $4.1bn flat from a year ago. Down sequentially due to wireless seasonality.”

"On non-AI semiconductor...We don't see a sharp recovery that is sustainable yet..We don't see any further deterioration in demand. It's more, I think, maybe the AI is sucking the oxygen a lot out of enterprise spending elsewhere and hyperscaler spending elsewhere"

“You can say that $73bn is the backlog we have today to ship over the next six quarters. You might also say that given our lead time, we expect more orders to be able to be absorbed into our backlog for shipments over the next 6 quarters.”

Good morning!

[8:33 am] ASX 200 futures are down 51pts (-0.58%) as of 8:30 am AEDT.

The overnight session in a nutshell:

Major US benchmarks lower, with the S&P 500 closing out the week down 0.63%

Broadcom dipped 11% despite a solid quarterly result and massive $73bn backlog

Commodities mostly lower after recent breakout move, with copper (-2.3%) and silver (-2.6%) leading the pullback

Catch up on all the overnight moves and news via today's Morning Wrap.