ASX 200 Live Today - Friday, 9th Jan

The S&P/ASX 200 is set to trend higher today amid a rotation back into cyclical pockets of the market. Here are today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Friday, January 9. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Be sure to refresh manually for the latest updates — and let us know how we can make it even better.

ASX 200 edges higher, on track to close the week flat

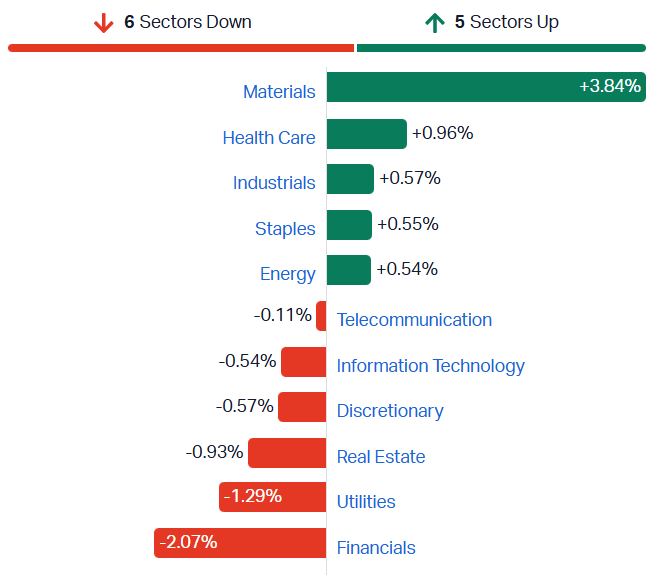

[1:55 pm] A bit of a nothingburger session (and week). The ASX 200 is currently up 0.12% and on track to finish the week around breakeven. Materials has done most of the heavy lifting this week (+3.84%), offsetting weakness from banks, select defensives and tech. Honestly, not much to look at (which isn't a bad thing ahead of February reporting season). That's all for today, have a good weekend and ... try to stay cool.

ASX 200 sectors, weekly performance (Source: Market Index)

ASX 200 intraday movers

[12:44 pm] The below tables look at the stocks that have experienced the largest price swings since open. Zip continues to catch a bid, with the stock now up more than 12% in the last two sessions. Meanwhile, plenty of resource names (rare earths, gold, uranium and nickel) continue to trend lower.

Ticker | Company | % Chg since open | Price |

|---|---|---|---|

ZIP | Zip Co | 4.23% | $3.58 |

VEA | Viva Energy Group | 3.43% | $2.11 |

MSB | Mesoblast | 2.88% | $3.22 |

ORA | Orora | 2.52% | $2.24 |

PXA | Pexa Group | 2.46% | $13.34 |

NEU | Neuren Pharmaceuticals | 2.24% | $19.19 |

DRR | Deterra Royalties | 2.20% | $4.18 |

REA | Rea Group | 2.14% | $189.73 |

REH | Reece | 2.11% | $13.79 |

Ticker | Company | % Chg since open | Price |

|---|---|---|---|

LYC | Lynas Rare Earths | -4.53% | $14.11 |

MAF | MA Financial Group | -4.52% | $10.88 |

PNR | Pantoro Gold | -3.65% | $5.01 |

CMM | Capricorn Metals | -3.43% | $13.94 |

PDN | Paladin Energy | -3.36% | $10.50 |

RIO | Rio Tinto | -3.11% | $143.92 |

4DX | 4DMedical | -3.04% | $4.46 |

EMR | Emerald Resources | -3.02% | $6.26 |

CNU | Chorus | -2.53% | $8.09 |

NIC | Nickel Industries | -2.42% | $0.93 |

China inflation edges higher

[12:41 pm] China's consumer price index inflation rose to 0.8% year on year in December, up from 0.7% in the prior month and marked the highest since February 2023. The print was slightly below market expectations of 0.9%.

Factory gate deflation also slightly improved to -1.9% year-on-year in December vs. market expectations of -2.0% and up from -2.2% in the prior month.

Building and construction stocks broadly higher

[11:41 am] Building and constructions stocks like James Hardie (+4.5%), Reece (+2.7%), Reliance Worldwide (+3.0%) and GWA Group (+2.4%) are trading broadly higher after Trump announced plans to tap the Fed's balance sheet to force mortgage relief.

Most of these building and constructions companies derive significant earnings from the US market.

The White House is using Fannie Mae and Freddie Mac’s retained portfolios to push mortgage rates lower ahead of the midterms, with mixed views on how much impact remains.

Trump directed Fannie Mae and Freddie Mac to buy $200bn of mortgage-backed securities, arguing higher GSE demand will compress MBS risk premiums and flow through to lower mortgage rates.

The GSEs have already expanded retained portfolios by more than 25% in the five months to October, making bond purchases a fast, operationally simple policy lever.

Estimates suggest a $200bn to $250bn increase in GSE portfolios could cut mortgage rates by around 0.25 percentage points, with the 30-year rate already down to 6.16%, near its lowest since October 2024.

ASX 200 fades early gains

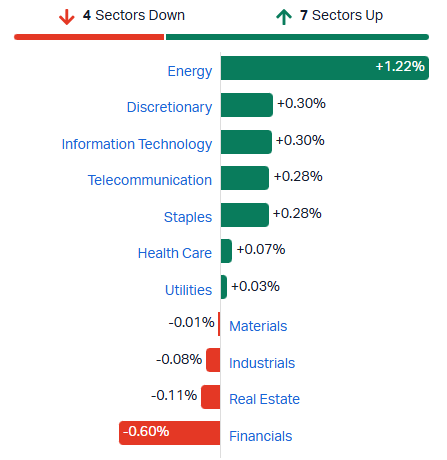

[10:47 am] ASX 200 currently down 0.11%, fading early gains of 0.48%. Sectors are all over the place, with Energy sharply higher following the oil price bounce overnight. The main driver of the intraday weakness is the Financials sector, which was briefly up 0.61% at the open, now down 0.55%.

ASX 200 sector performance (Source: Market Index)

Top ASX 200 gainers and losers

[10:07 am] Codan and Mesoblast are trading sharply higher off the back of trading updates, while resource stocks experience a broad-based pullback in early trade.

Ticker | Company | % Chg | Price |

|---|---|---|---|

CDA | Codan | 20.63% | $38.07 |

MSB | Mesoblast | 8.06% | $2.95 |

APE | Eagers Automotive | 6.61% | $27.11 |

JHX | James Hardie Industries | 4.80% | $32.32 |

DRO | Droneshield | 3.64% | $3.99 |

BPT | Beach Energy | 3.27% | $1.11 |

ALL | Aristocrat Leisure | 3.08% | $58.40 |

OBM | Ora Banda Mining | 2.78% | $1.55 |

CMM | Capricorn Metals | 2.58% | $14.34 |

REA | REA Group | 2.52% | $187.73 |

Ticker | Company | % Chg | Price |

|---|---|---|---|

DRR | Deterra Royalties | -5.79% | $4.07 |

RIO | Rio Tinto | -4.78% | $145.33 |

ZIM | Zimplats | -3.79% | $23.09 |

NIC | Nickel Industries | -2.60% | $0.94 |

CSC | Capstone Copper Corp | -2.47% | $14.62 |

AAI | Alcoa Corporation | -2.16% | $90.53 |

ILU | Iluka Resources | -1.88% | $6.26 |

XYZ | Block | -1.52% | $105.23 |

SLX | Silex Systems | -1.32% | $6.75 |

4DX | 4DMedical | -1.30% | $4.54 |

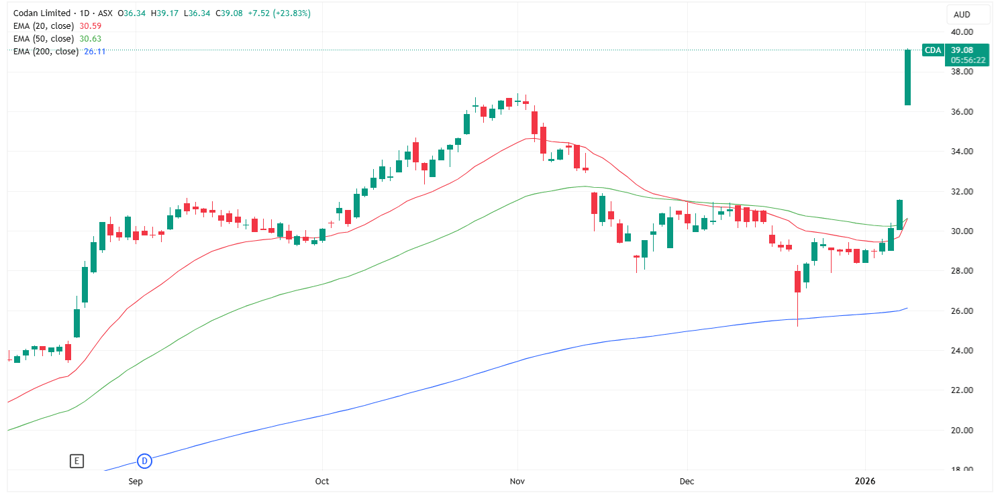

Codan rallies ~20pc in early trade

[10:04 am] Codan shares opened 15.1% higher ($36.34) and currently up 22.9% to a record $38.81.

That's about ~4% above its 3-Nov-25 record. What an incredibly move off the back of an above consensus trading update.

Codan daily price chart (Source: TradingView)

Codan first-half FY26 trading update

[9:30 am] Codan flagged a strong first half, with profit growth outpacing revenue as metal detection demand drove operating leverage.

First-half FY26 revenue is expected to be about $394m, up 29% on pcp, well ahead of typical mid-teens growth rates.

Underlying NPAT is expected to be at least $70m, up around 52% on pcp.

Metal detection revenue rose 46% to $168m, driven by gold detector sales in Africa and double-digit growth across other recreational markets.

Communications revenue increased 19% to $222m, tracking at the upper end of management’s 15% to 20% growth target range.

To add some perspective, Macquarie (Aug-25) was expecting 1H26 revenue of $384.9 million and NPAT of $67 million. This suggests today's revenue and NPAT guidance is tracking 2.2% and 4.4% ahead of estimates, respectively.

Codan is trading in a bit of a tricky spot, down ~14% from its 31-Oct-25 record high but still trading at a PE of 55x.

The stock experienced a 4.7% rally on Thursday, though this was likely in-line with a broad tech/growth bounce (e.g. Life360 +3.9%, Catapult Sports +3.6%, Bravura +3.2% etc.)

Company page: Codan (CDA)

Aristocrat extends on-market buyback program

[9:08 am] Aristocrat has purchased $701.1 million worth of shares since February 2025, with plans to extends its on-market buyback program for a further $750 million in shares through to March 2027.

“... Our consistently strong cash flow generation, we are able to continue to pursue a mix of returns to shareholders via dividends and share buy-backs while also investing in strategic acquisitions and organic growth initiatives," says CEO Trevor Croker.

The stock is down 18% in the last twelve months and trading near the lowest level since October 2024 (so I guess it makes sense to pursue a buyback at these depressed prices).

Aristocrat suffered a 7.5% selloff on 12 November after its FY25 result flagged disappointment in Gaming Operations, where North American net adds came in below forecast and the revenue mix skewed toward lower-margin outright sales.

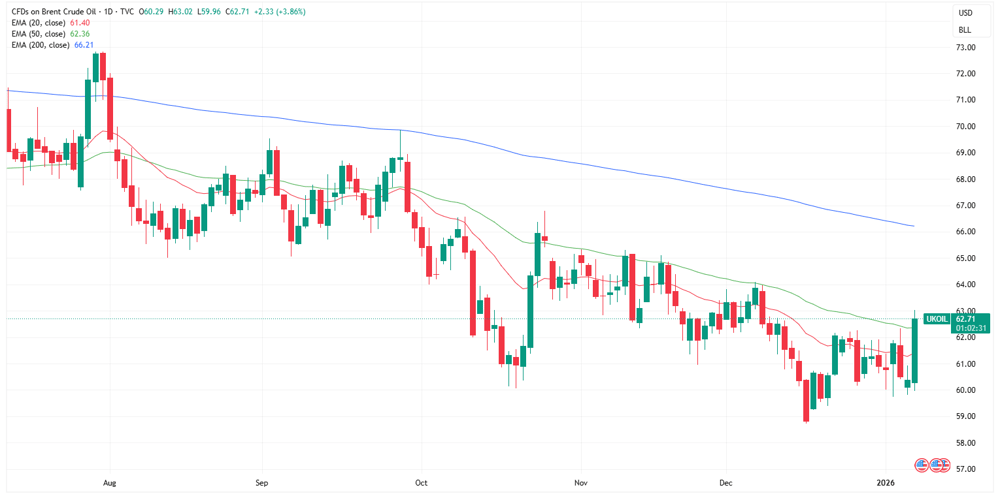

Oil prices bounce to one-month high

[9:01 am] Brent crude rallied 3.8% overnight to $62.6 a barrel, the highest level since 8 December. Plenty of recent bounces into the 50-day moving average have been sold off shortly after.

Woodside ADRs finished 2.35% higher overnight to US$15.70. This implies a $23.44 open today vs. Thursday's close of $22.95.

Brent crude daily price chart (Source: TradingView)

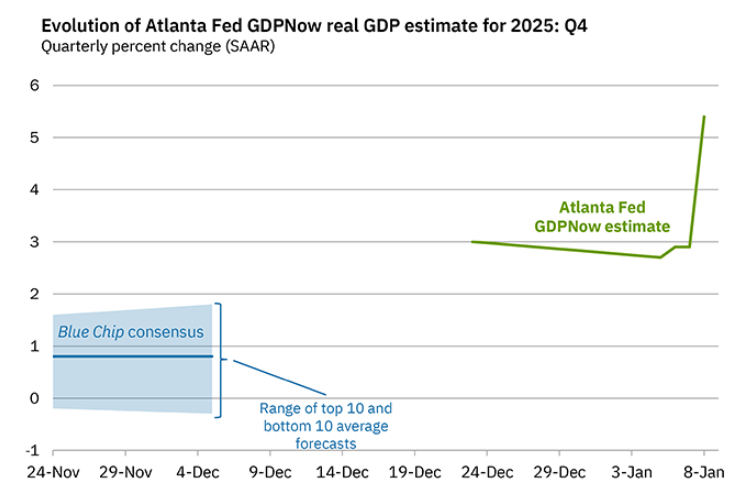

US GDPNow forecasts 5.4% growth in Q4

[8:50 am] The Atlanta Fed's GDPNow is forecasting 5.4% growth for the December quarter, up from 2.7% a few days ago. This massive pop largely reflects a smaller trade deficit (now at the smallest since 2009) and solid consumer spending.

Source: Atlanta Fed

Glencore and Rio Tinto restart merger talks

[8:46 am] Glencore has confirmed that it has restarted discussions with Rio Tinto about a possible "combination of some or all of their businesses, which could include an all-share merger between Rio Tinto and Glencore.”

Rio Tinto ADRs closed 0.81% lower overnight, while Glencore ADRs surged 8.8%.

Fed doves talk big, markets stay cautious

[8:44 am] Fed policymakers are signalling aggressive rate cuts, but markets remain unconvinced amid firmer data and Fed leadership uncertainty.

Fed Governor Miran is advocating 150 bp of cuts in 2026, arguing inflation is effectively 2.3% and the labour market could absorb around 1 million additional jobs without reigniting price pressures.

Treasury Secretary Bessent reinforced the dovish push, calling further Fed cuts the key missing ingredient for stronger growth and urging the Fed not to delay easing.

Markets are pushing back, pricing only 53 bp of cuts through year-end, down from recent weeks as economic data has surprised to the upside since mid-December.

Fed chair succession risk is rising, with Kevin Warsh now marginally ahead of Kevin Hassett in betting markets, both viewed as more dovish than Powell.

Warsh is increasingly seen as the safer choice for Fed independence, while reports suggest lingering market and White House concerns around Hassett.

Investors near 10-year bearish extreme on oil

[8:42 am] A Goldman Sachs survey shows more than 59% of institutional investors are bearish or slightly bearish on crude, close to the lowest readings in its dataset going back to January 2016 and only exceeded last April amid Trump tariff fears.

A record share of respondents named oil as their favourite short, underscoring strong bearish positioning.

Markets have been weighed down by a supply glut as OPEC+ output rises, US production stays high and countries including Brazil and Guyana expand volumes.

Brent crude remains around US$60-plus, still down significantly from a year ago, reflecting surplus concerns despite modest recent bounce.

Source: Bloomberg

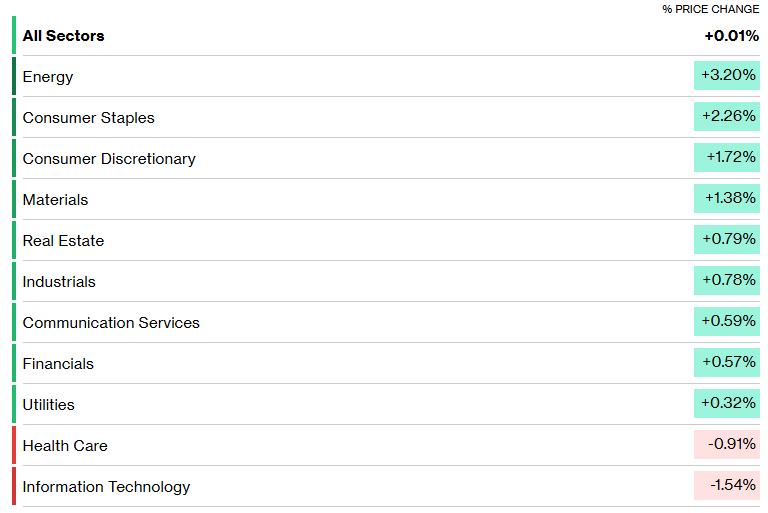

S&P 500 flat as tech stocks lag

[8:40 am] Breadth was notably positive overnight, with most sectors trading higher and the Equal-weight S&P 500 (+0.86%) outperforming the benchmark by 87 bps.

S&P 500 sector performance (Source: Bloomberg)

Good morning!

[8:27 am] ASX 200 futures are up 39pts (+0.44%) as of 8:30 am AEDT.

The overnight session in a nutshell:

S&P 500 (+0.01%) breakeven in a relatively choppy and sideways session

Breadth was notably strong, with sectors like Energy, Staples, Discretionary and Materials up more than one percent

Equal-weight S&P 500 (+0.86%) outperformed the official benchmark by 87 bps, Russell 2000 (+1.11%) also closed at fresh all-time highs

No major catalysts, markets in waiting mode for upcoming NFP data, Supreme Court decision on Trump tariffs, start of Q4 earnings and ongoing geopolitical uncertainty

The Morning Wrap will be up shortly, be back in a moment.