ASX 200 crashes in worst session since 2020

The S&P/ASX 200 is trading 4.4% lower, on-track to mark its worst one-day session since the pandemic. Here's everything you need to know.

Source: Shutterstock

KEY POINTS

- The ASX 200 is down 4.4% at noon, on track for its worst single-day decline since the pandemic-era selloffs of March 2020.

- WTI crude has surged 25% to $114 a barrel after US and Israeli forces struck Iranian oil infrastructure for the first time, with no ceasefire talks in sight.

- Australian 10-year bond yields have spiked to levels last seen in 2011, with markets now pricing in a 30% chance of an RBA rate hike this month.

The ASX 200 is down 4.4% at noon, with nothing spared outside a handful of energy stocks. If the market closes at these levels, it will mark the worst one-day decline since the pandemic.

Global equity markets have been rocked by the ongoing Iran war, which sent WTI crude ~25% higher on Monday to US$114 a barrel, following a 35% rally last week – the largest weekly oil price gain since the pandemic. Wall Street futures are trading sharply lower, with S&P 500 and Nasdaq futures down 2.3% and 2.6% respectively.

Here's what you need to know about the Iran conflict and how key ASX sectors and stocks are performing.

Catch up quick: Iran conflict

The US-Israel campaign against Iran began on 28 February, marking a significant escalation in tensions that had been building for years over Iran's nuclear programme, its support for regional proxies, and repeated drone and missile exchanges with Israel.

Among the most significant developments was the killing of Supreme Leader Ali Khamenei, who had led Iran since 1989.

The campaign has struck more than 3,000 targets by the US and Israel , with 80% of Iran's air defences destroyed and 43 warships taken out, severely degrading the country's conventional military capability.

Iran has responded with force, launching attacks on more than 27 US military bases across the region and making over 90 strike attempts on Israel.

Mojtaba Khamenei, the late supreme leader's 56-year-old son, has been appointed as his replacement, raising questions about whether Iran's long-standing religious edict against nuclear weapons will hold under new leadership.

Iran's military says it can sustain at least six months of high-intensity conflict and is preparing to deploy advanced long-range missiles, suggesting the war is far from entering a de-escalation phase.

The worst session since Liberation Day

Today's selloff is on track to surpass Trump's Liberation Day selloff last April.

Date | Close | % Chg |

|---|---|---|

24/08/2015 | 5001.3 | -4.09% |

9/03/2020 | 5760.6 | -7.33% |

12/03/2020 | 5304.6 | -7.36% |

16/03/2020 | 5002 | -9.70% |

18/03/2020 | 4953.2 | -6.43% |

23/03/2020 | 4546 | -5.62% |

27/03/2020 | 4842.4 | -5.30% |

1/05/2020 | 5245.9 | -5.01% |

7/04/2025 | 7343.3 | -4.23% |

9/03/2026 | 8461 | -4.40% |

ASX 200 sessions with a decline of 4% or more, in chronological order.

A sea of red

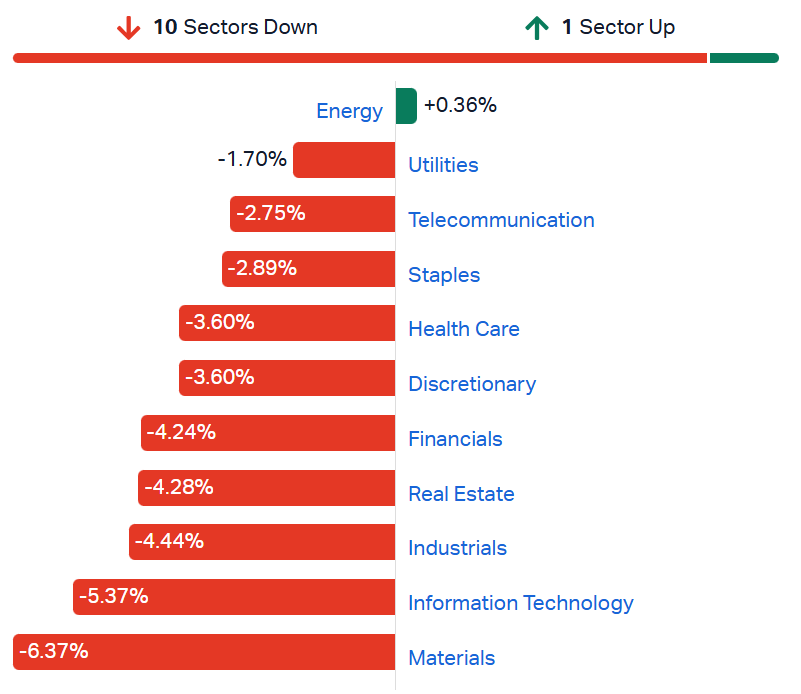

The market opened around 2.7% lower and has continued to slide, now down 4.4% with no bounce in sight.

Pretty much everything is trading sharply lower, with the exception of energy. Breadth is abysmal, with 194 S&P/ASX 200 constituents (97%) in the red. The only six stocks bucking the trend are all from the energy sector: Yancoal, Santos, Beach Energy, New Hope, Woodside and Whitehaven Coal.

S&P/ASX 200 sectors as at 1:00 pm AEDT (Source: Market Index)

The market's largest stocks are offering no comfort, all down 4-6%.

Ticker | Company | % Chg | Price |

|---|---|---|---|

CBA | Commonwealth Bank | -4.04% | $165.50 |

BHP | BHP Group | -6.48% | $49.39 |

RIO | Rio Tinto | -4.82% | $151.03 |

NEM | Newmont | -3.26% | $159.76 |

NAB | National Australia Bank | -4.39% | $44.77 |

WBC | Westpac | -4.68% | $39.08 |

ANZ | ANZ Group | -4.61% | $35.91 |

WES | Wesfarmers | -2.94% | $73.59 |

MQG | Macquarie Group | -4.91% | $190.46 |

CSL | CSL | -3.47% | $141.19 |

S&P/ASX 10 performance (Source: Market Index)

The worst-performing ASX 200 stocks are mostly resource-related, alongside a handful of travel and tech names.

Ticker | Company | % Chg | Price |

|---|---|---|---|

DNL | Dyno Nobel | -11.36% | $3.01 |

PDI | Predictive Discovery | -11.26% | $0.81 |

CSC | Capstone Copper Corp | -10.77% | $11.18 |

DYL | Deep Yellow | -10.37% | $1.95 |

SFR | Sandfire Resources | -10.06% | $15.37 |

4DX | 4DMedical | -10.05% | $3.90 |

ZIP | Zip | -9.76% | $1.67 |

VGN | Virgin Australia | -9.14% | $2.64 |

PLS | PLS Group | -8.93% | $4.34 |

MSB | Mesoblast | -8.91% | $2.10 |

Yield stress test

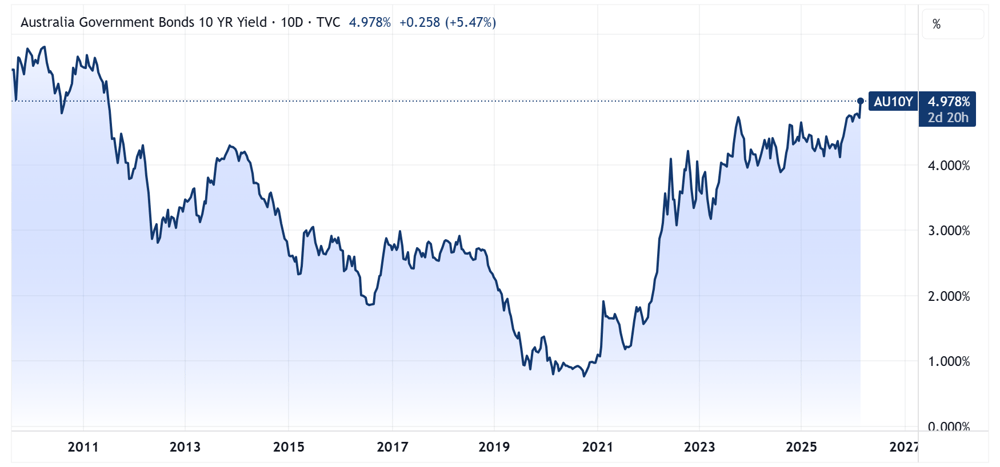

Soaring oil prices have stoked inflation concerns, driving the Australian 10-year bond yield up 340 basis points over the last six sessions, surpassing October 2023 levels to trade at levels last seen in July 2011. The October 2023 yield peak coincided with the low for global equity markets, with the ASX 200 falling around 9% between August and November 2023.

Australia 10-year bond yield chart (Source: TradingView)

Markets are now pricing in a 30% chance of a rate hike at this month's RBA meeting, with a 25bp hike fully priced in for May.

Where to from here?

It hinges on how the Iran conflict unfolds, and for now it continues to escalate.

In the past 24 hours, Israel and the US struck Iranian oil infrastructure for the first time, the US embassy in Norway was hit by an explosive device, and Iran's top security official vowed Trump "must pay the price." WTI crude opened 7.9% higher this morning and has since pushed to intraday highs of 25%, or US$114 a barrel, a clear signal that conditions are deteriorating.

The oil price surge is putting pressure on inflation expectations at a time when RBA trimmed mean CPI printed 3.4% in January, still above the 2-3% target.

Any de-escalation would be the key catalyst for calmer markets and help stabilise soaring oil prices and yields. But if the past 24 hours is any guide, oil infrastructure is now fair game on both sides, with no sign of ceasefire talks or negotiations.

The broader challenge for markets is that the ASX 200 entered the conflict trading at a forward price-to-earnings of 18.7x. With valuations already stretched, a deteriorating earnings and inflationary backdrop is the last thing markets need.