ASX 200 companies set to deliver strongest earnings growth in four years

UBS' profit forecasts have surged from 3% to 12% in six months as miners and banks benefit from a resilient domestic economy.

Source: Shutterstock

KEY POINTS

- ASX 200 companies are forecast to deliver 12% earnings growth in FY26, up from 3% expected six months ago, marking the strongest profit growth in four years, according to UBS

- The Technology sector has reversed sharply with profit growth now expected at just 0.8% in FY26, with major players like WiseTech and Xero facing flat-to-negative earnings growth

- UBS highlights buy-rated stocks with upside potential including Coles, Qantas, Goodman Group and Flight Centre, while flagging downside risks for Woolworths, JB Hi-Fi and Treasury Wine Estates

The Australian sharemarket is heading into February reporting season with profit growth expectations that have quadrupled in just six months, underpinned by a domestic economy proving far more resilient than anticipated.

ASX 200 companies are now forecast to deliver earnings growth of 12% for FY26, up from the 3% expected six months ago, according to UBS. The upgrade represents the strongest profit growth in four years and comes as the RBA reversed course last week with a rate hike, after concluding its cutting cycle last August.

While valuation expansion drove the market to new highs through mid-2025, the current rally is being fuelled by actual profit growth, a healthier foundation for sustained gains, note the analysts.

Miners and banks lead the charge

The profit upgrade story is heavily concentrated in the market's traditional heavyweights. Mining companies are expected to see profits soar 30% this financial year after several years of decline. Banks are similarly positioned to benefit from earnings tailwinds as the economy strengthens.

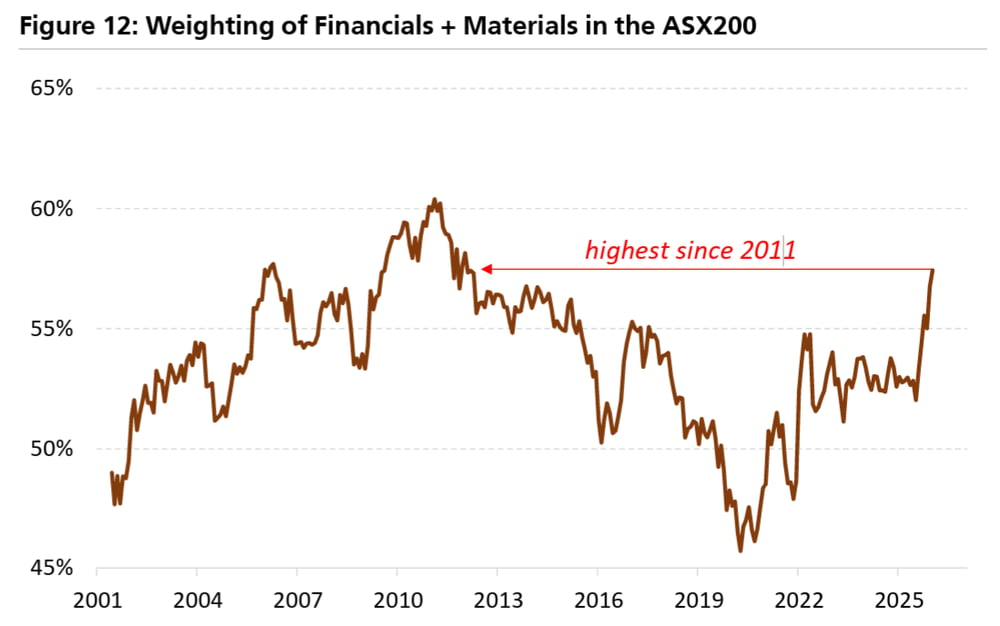

This resurgence has pushed Resources and Banks to their highest combined weighting in the S&P/ASX 200 since 2010. The so-called "old guard" sectors are reclaiming dominance after years of being overshadowed by capital-light growth companies.

Source: UBS

Technology stumbles badly

The most dramatic reversal has occurred in the technology sector. After years of being a bright spot for earnings, tech stocks have stumbled badly over the past six months and are now expected to see profits grow just 0.8% in FY26.

It's worth noting that these flat growth forecasts refer to the tech sector as a whole, where Wisetech and Xero dominate the estimates given their market weightings. Both companies are forecast to deliver flattish-to-negative year-on-year earnings growth in FY26.

The valuation compression in Australian tech has been aggressive, with former high-flyers showing little sign of forming a floor. UBS expects these capital-light businesses to face a level of investor scepticism not seen for some time.

However, UBS notes the selloff remains contained to the tech sector rather than spreading across the broader market. The ASX 200 forward price-to-earnings ratio still sits above 18x, compared to falling below 13x during the February 2022 market-wide selloff triggered by the Ukraine invasion. This suggests the current tech wobbles are micro rather than macro in nature.

Margins holding despite cost pressures

One positive development across the broader market has been companies' ability to maintain profit margins despite ongoing headwinds. Energy costs and wage pressures continue to weigh on businesses, but UBS's pricing power measure indicates companies remain in a relatively healthy pricing environment.

This pricing resilience should allow businesses reporting in February to maintain margins, supporting the overall profit growth outlook.

Currency impact minimal for this period

While the Australian dollar has recently broken through 70 US cents, UBS doesn't expect currency movements to be a significant factor in February results. The dollar averaged 66 cents through June to December 2025, essentially matching the prior corresponding period.

Some companies may reference the recent currency strength in their commentary, but the impact on reported earnings for the half should be limited.

Stock-specific opportunities

UBS analysts have identified specific companies where they see upside risk to consensus expectations during February results. Buy-rated names on this list include:

Coles

Cleanaway

Domino's Pizza

Flight Centre

Goodman Group

IAG Insurance

IDP Education

Navigator Global Investments

Qantas

Sigma Healthcare

Universal Store

WiseTech Global

Conversely, the firm sees downside risk for:

Accent Group

Aurizon

Bendigo and Adelaide Bank

Guzman y Gomez

JB Hi-Fi

Mirvac

Monadelphous

Orora

Reliance Worldwide

Super Retail Group

TPG Telecom

Treasury Wine Estates

Woolworths.

Looking ahead

UBS presents three key themes to navigate this reporting season:

#1 Cyclical stocks with exposure to the domestic economy or global commodities are likely to perform well. With PMI readings above 50, a rising Australian dollar and positive earnings momentum, GDP-linked businesses can offer relative safety amid the quality stock selloff.

#2 Investors should brace for continued pressure on capital-light growth companies. The scepticism around business model sustainability in light of AI threats shows little sign of abating.

#3 The return of Banks and Resources to market dominance means these sectors will use February results to highlight their earnings resilience against technology sector concerns.

UBS also warns that companies with the most "stale" earnings estimates, where sell-side analysts haven't updated forecasts for three months or more, tend to show outsized share price volatility on results.

The February reporting season will provide the first comprehensive read on how Australia's surprisingly strong economy is translating to corporate profits, and whether the sharp divergence between old economy and new economy stocks is justified by fundamentals.