Are Sandfire Resources shares a buy after their quarterly report?

Sandfire Resources shares have dropped along with the copper price. Last week’s quarterly report gave brokers a chance to amend their views.

Source: Shutterstock, Market Index

Mentioned

KEY POINTS

- Sandfire Resources (ASX: SFR) is considered to be the most prominent ASX-listed copper pure play

- It enjoyed massive share price gains as the copper price soared earlier in the year, but since May shares have plunged 20%

- The company’s quarterly report provides the big brokers with an opportunity to reassess their views on the company in light of the recent pullback and decide: Buy, Hold, or Sell?

Copper was supposed to be the next big thing in 2024, but after a rollicking start to the year, the copper rally appears to have petered out – another victim of the dreaded commodity price cycle.

Sandfire Resources (ASX: SFR) is generally considered to be the pre-eminent pure-play copper stock on the ASX, and for this reason, both the best way to access the copper investing theme, and a major potential takeover target.

Indeed, SFR’s share price has tracked the copper price very well, as can be seen in the graphic below. If anything, SFR’s performance has outshone copper’s – demonstrating the excellent leverage it affords investors to a potential copper mega-trend.

%20performance%20in%202024%20(in%20percent).png)

Sandfire Resources (SFR) vs London Metals Exchange Copper Cash price in percentage terms since January 1, 2024.

On Thursday, Sandfire released its June quarter production and activities report. With possibly the last of the broking research notes covering the report hitting my desk this morning, I bring you a comprehensive overview of everything the brokers had to say about it, and whether they think SFR is a buy, hold, or sell. Let’s dive in!

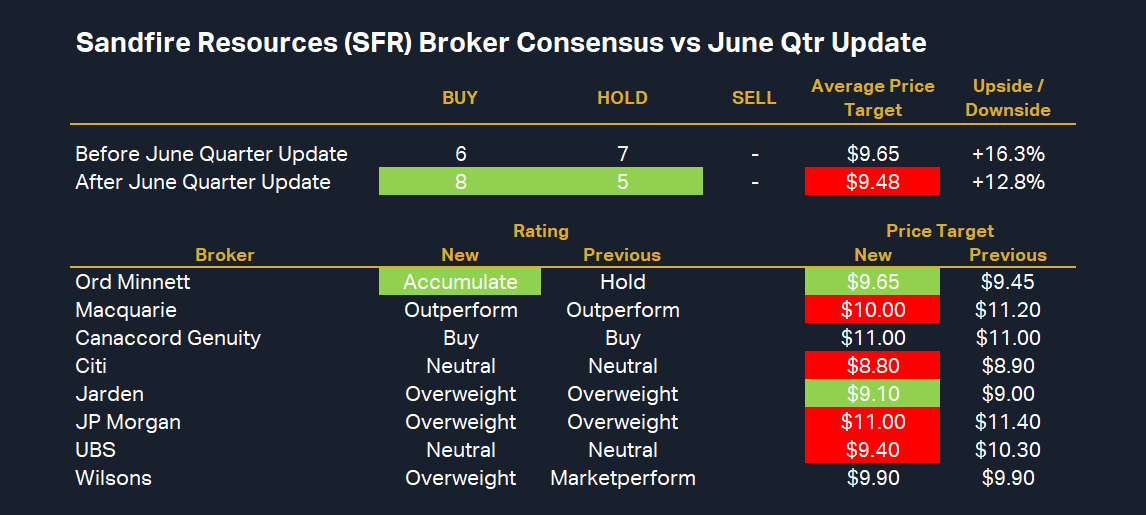

Sandfire Resources Broker Consensus vs June Quarter Update

%20Broker%20Consensus%20vs%20June%20Qtr%20Update.png)

Sandfire Resources Broker Consensus vs June Quarter Update infographic (assumes SFR share price $8.40) Click here for full size image

{kind=link}

Let’s kick off with a summary of all the moves in broker ratings and price targets post SFR’s quarterly report. The graphic above compares all the broker information we have on file going back three months to keep it current. We have filings for 13 brokers in total, of which 8 issued updates since the quarterly.

The only rating change came from Ord Minnett who upgraded SFR from HOLD to ACCUMULATE (reversing their 6 June downgrade). Overall, the brokers are now 8 BUY and 5 HOLD (versus 7 BUY and 6 HOLD previously).

To obtain a broker consensus rating, I like to assign a value of +1 to any rating better than HOLD/NEUTRAL/MARKETWEIGHT, 0 for HOLD/NEUTRAL/MARKETWEIGHT, and -1 to any rating worse than HOLD/NEUTRAL/MARKETWEIGHT. I associate an average rating value of greater than 0.5 as a BUY consensus, values between 0.5 and -0.5 a HOLD consensus, and values less than -0.5 as a SELL consensus.

Using this method, SFR’s average rating value of 0.62 earns it a consensus BUY rating in my book.

There were several price target changes for SFR, including 4 cuts and 2 raises. The result was the price target across the 13 brokers declining by 17 cents, or 1.8%, to $9.48. This implies 12.8% upside based on the price at the time of writing of $8.40.

The highest price target of $11 is held by Canaccord Genuity and JP Morgan. For what it’s worth, their $11 price target represents around 31% upside. The lowest price target of $8.25 is held by Morgan Stanley and represents around 2% downside – but this broker is yet to release a research update post-SFR report, so this might change.

I suggest it’s a vote of confidence that all but Morgan Stanley currently have a price target greater than SFR’s current price, and that the variance between all targets is less than 1% of SFR’s share price. It appears brokers are generally seeing roughly the same set of fundamentals for the company.

Let’s take a quick look at the broker’s commentaries to see if we can glean any further information as to what factors they think could move the dial going forward.

Canaccord Genuity

Retain BUY | Price Target $11.00

Broker viewed Motheo operational performance as strong, but noted weaker performance at MATSA

Overall, satisfied with June quarter report, and continues to see value in SFR’s share price

Citi

Retain NEUTRAL | Price Target $8.80⬇️ from $8.90

Broker noted the June quarter “ended on a high” with increased EBITDA margins, a strong performance at Motheo, and the addition of $68m cash

Broker liked the fact that update “provided some more timing of catalysts with an updated LOM plan for Motheo due August which should deliver more metal and a Black Butte FID 12-24m away”

“Exploration and organic growth remains the focus. We maintain our Neutral recommendation with our house view that copper consolidates before the next leg higher”

Jarden

Retain OVERWEIGHT | Price Target $9.10⬆️ from $9.00

Broker views SFR delivered a strong fourth quarter performance in terms of production, sales, and cash flow

Notes a significant reduction in the company’s debt position

Broker is comfortable with it’s OVERWEIGHT rating due to their strong conviction for copper price fundamentals

JP Morgan

Retain OVERWEIGHT | Price Target $11.00⬇️ from $11.40

Broker noted that FY24 EBITDA exceeded expectations but was disappointed by FY25 guidance. This caused the broker to downgrade their earnings forecast for FY25

SFR still represents an attractive valuation based upon the current share price, and also, factoring in the broker’s present positive view on the copper price in the medium term

Macquarie

Retain OUTPERFORM | Price Target $10.00⬇️ from $11.20

Broker noted that SFR’s quarterly copper production was in line with consensus, silver production beat consensus by 14%, but zinc production was 10% lower than consensus

The broker described FY25 production guidance as “mixed”, noting strong lead/silver production guidance (6-7% above consensus), but weaker copper/zinc production guidance (3-5% below consensus).

“Importantly, SFR had a material reduction in net debt, reducing US $85m QoQ to US$396m at the end of 4QFY24”, broker notes this was 11% below consensus

“Even after incorporating increased operating costs, SFR has a strong FY25 EV/Ebitda of 4.8x and FCF yield of 11%.”

UBS

Retain NEUTRAL | Price Target $9.40⬇️ from $10.30

“C1 costs of US$1.54/lb at MATSA and US$1.56/lb at Motheo highlight the ongoing cost control and improved by-product credits”

“We await capex guidance at the FY24 results, but with the stock off ~20% from recent highs it's starting to look more attractive once copper improves”

“As Motheo continues to beat expectations sustaining 5.4Mtpa over the Jun-Q, FY25 guidance of 53kt copper may prove to be conservative again”