Another bloodbath for the ASX 200 as oil prices spike, the Fed turns hawkish and miners get crushed

The ASX 200 has erased its entire year-to-date gain in just over two weeks amid surging oil, hawkish Fed rhetoric and a commodity rout.

Source: Shutterstock

KEY POINTS

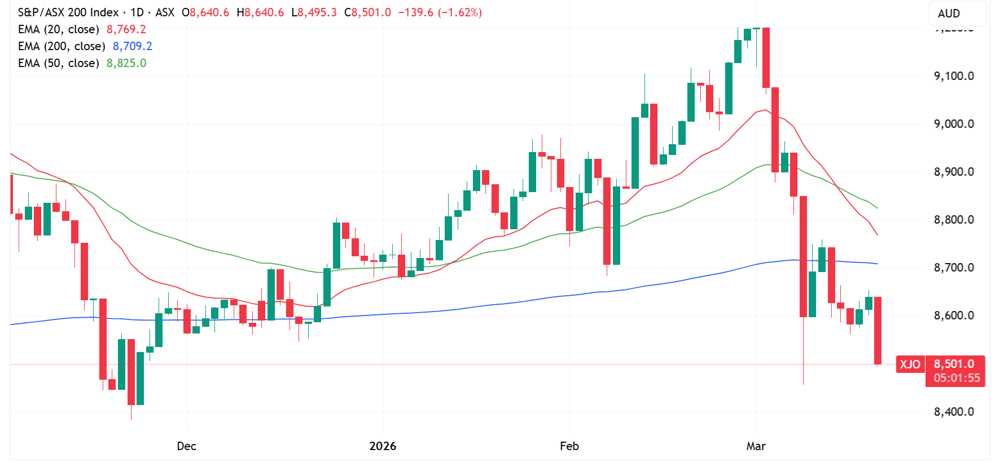

- The S&P/ASX 200 has flipped from a year-to-date gain of 5.6% to negative 2.5% in a little over two weeks, undercutting the 9 March low to trade at its lowest level since 21 November 2025, with 89.5% of constituents in the red at noon.

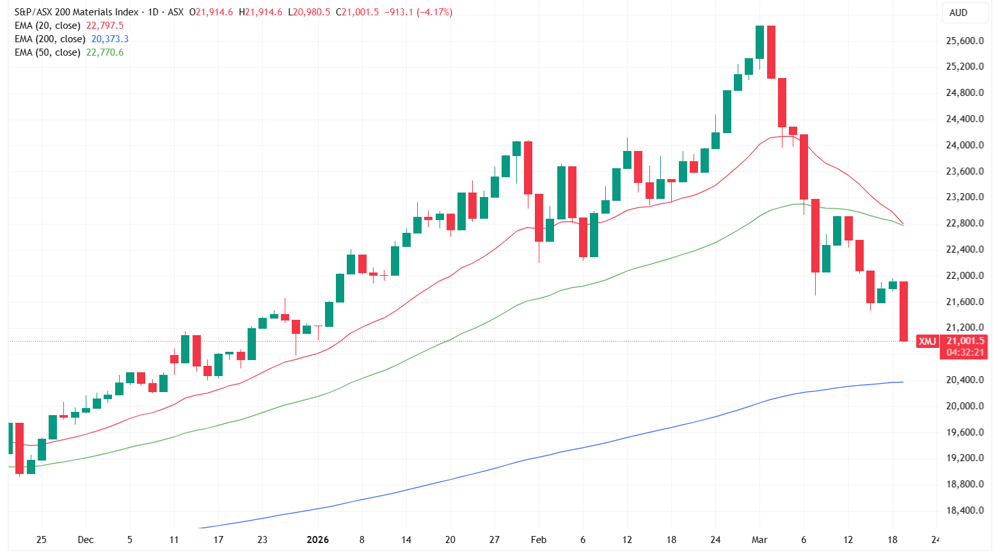

- The ASX 200 Materials Index has given back its entire 22% rally from late December to early March, with miners squeezed between weakening demand expectations and soaring input costs across diesel, electricity, explosives and logistics.

- Rate cut expectations have been completely repriced, with markets now pricing in zero Fed cuts by year-end compared to at least two just weeks ago, while the ECB is fully priced for 50 basis points of hikes this year.

The S&P/ASX 200 is down 1.57% at noon and on track to close at near four-month lows after a tough overnight session that featured hawkish remarks from the Fed, hotter-than-expected inflation data and higher oil prices.

Overnight session in a nutshell

S&P 500 (-1.36%), Dow (-1.63%), Nasdaq (-1.46%) and Russell 2000 (-1.64%)

The Fed held interest rates at 3.50-3.75%, as widely expected

At the press conference, Powell said the Fed "wasn't making as much progress on inflation as we had hoped"

US February producer price index came in hot, with headline figures up 0.7% month-on-month vs. 0.3% estimates, and the three-month annualised core pace at its highest since May 2022

The PPI report noted a 1.1% month-on-month spike in goods prices, the largest increase since August 2023, with over 20% of the final demand goods rise attributable to a 48.9% surge in fresh and dry vegetable prices

Qatar's Ras Laffan Industrial City, home to the world's largest LNG export plant, suffered "extensive damage" from an Iranian strike

Brent crude rallied 5.9% overnight to US$109.64 a barrel, the highest close since July 2022, with prices now up 83% year-to-date

Markets are now pricing in global central banks to hike. Swaps markets are fully pricing 50 bps of hikes for the ECB this year, and a 50% likelihood of a rate hike for the BoE by December, a sharp reversal from prior expectations of two cuts this year

ASX 200 today

In just over two weeks, the market has wiped out its year-to-date gain of 5.6%, swinging to negative 2.5%. The index has undercut the recent 9 March low and is trading at its lowest since 21 November, 2025.

S&P/ASX 200 daily chart (Source: TradingView)

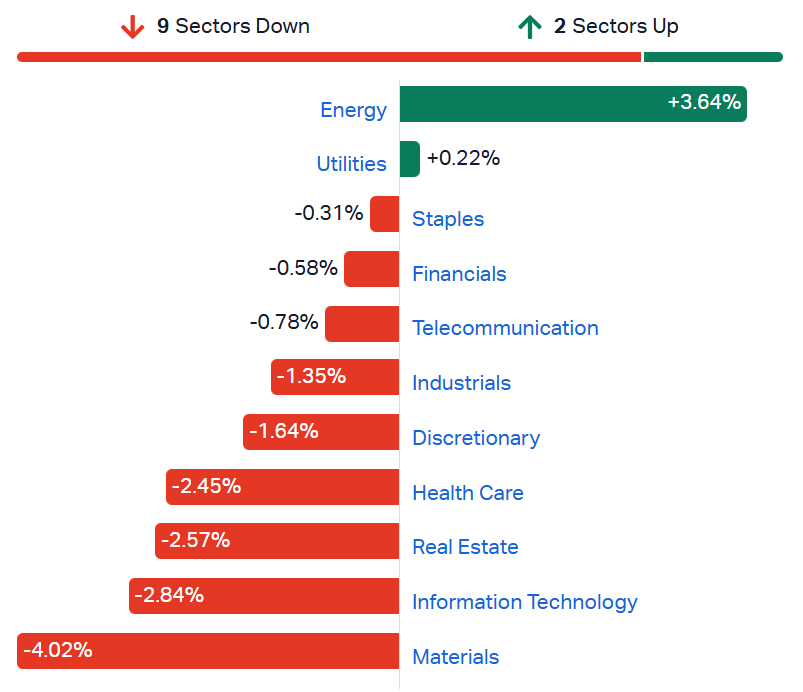

Breadth is weak, with 179 constituents trading lower (89.5%) and most sectors down 1.0% or more. Energy stocks have bucked the trend thanks to higher oil prices. Utilities and Staples are outperforming on a relative basis, a clear sign of a shift towards defensive pockets of the market. Growth and yield-sensitive sectors like Materials, Tech and Real Estate are leading the selloff, all down more than 2%.

S&P/ASX 200 sector performance as at 11:05 am AEDT (Source: Market Index)

Energy stocks buck the trend

Energy stocks have bucked the trend, with the S&P/ASX 200 Energy Index up 3.7% to its highest since April 2024. Leading the rally is a mix of refiners, coal, LNG and oil producers.

Ticker | Company | % Chg | Price | YTD % Chg |

|---|---|---|---|---|

VEA | Viva Energy Group | 12.3% | $2.37 | 14.5% |

YAL | Yancoal Australia | 5.9% | $7.96 | 59.8% |

ALD | Ampol | 5.2% | $33.15 | 3.9% |

WHC | Whitehaven Coal | 5.0% | $9.19 | 18.3% |

WDS | Woodside Energy | 4.9% | $32.98 | 39.0% |

NHC | New Hope Corporation | 3.4% | $5.43 | 35.4% |

STO | Santos | 3.3% | $8.03 | 29.9% |

BPT | Beach Energy | 3.0% | $1.27 | 8.7% |

Miners smashed

The S&P/ASX 200 Materials Index rallied roughly 22% between late December and 2 March, and it took just over two weeks to erase all of those gains.

S&P/ASX 200 Materials Index daily chart (Source: TradingView)

The Materials Index is down 4.0% today, after a heavy overnight session for most commodities.

Commodity | % Chg | Price (US$) |

|---|---|---|

Palladium | -7.8% | $1,476 |

Platinum | -5.0% | $2,025 |

Copper | -5.0% | $5.49 |

Silver | -5.0% | $75.36 |

Gold | -3.7% | $4,818 |

Zinc | -2.8% | $3,136 |

Aluminium | -1.1% | $3,351 |

Nickel | -1.0% | $17,278 |

Miners are getting squeezed from both sides, caught between deteriorating economic growth concerns that weigh on commodity demand and soaring input costs driven by the Iran conflict.

Diesel is not the only cost exposure. Crack spreads have blown out, meaning refined fuel costs are rising faster than crude alone implies. Air New Zealand last week flagged jet fuel prices soaring from US$85-90 a barrel before the conflict to US$150-200.

Electricity costs will rise regardless of the generation source, whether gas, coal or diesel/heavy fuel oil. Labour and logistics costs are also set to increase, covering fly-in fly-out operations and product transportation to port. Explosives face upward pressure given Saudi Arabia accounts for roughly 20% of global DAP production, while Gulf nations are significant suppliers of chemicals, reagents and acids used in ore processing.

Where to from here?

Markets are in a rough patch where the Iran conflict is showing no signs of de-escalation, and attacks on key Middle East energy infrastructure continue to elevate supply concerns. Oil prices continue to climb, albeit in an extremely volatile fashion, sending ripple effects through the supply chain and to the pump.

The Fed's hold and Powell's comments took a hawkish lean, with Powell flagging concerns that inflation pressures could last longer than expected. Just a few weeks ago, the market was pricing in at least two 25 bp cuts by year-end. Now markets are pricing in none.

For a market that was trading at record highs just three weeks ago, there is a lot of bad news to absorb across yields, the economic growth outlook and cost inflation. These kinds of unwinds can be aggressive, and often overshoot. But with the Iran conflict showing no signs of abating, the situation could get worse before it gets better. After all, you can't print energy.