25% plunge in iron ore price is just demand vs supply –Macquarie

The iron ore price is down over 25% in 2024 and ASX iron ore stocks are tanking. Major broker Macquarie tips iron ore can fall even further.

Source: Shutterstock, Market Index

Mentioned

KEY POINTS

- The iron ore price has fallen over 10% over the past few weeks, and over 25% since the start of the year

- The share prices of ASX iron ore companies have experienced similar fortunes, taking a chunk out of many Aussie investors’ portfolios

- An environment of “solid” supply and “weak” demand are contributing to the lower iron ore price and it's likely to get worse, suggests major broker Macquarie

Like many proud West-Australians I barrack for one of the two local footy teams (the Harley Reid one) and our major iron ore exporters. Roughly 98% of the population over here either works for BHP Group (ASX: BHP), Rio Tinto (ASX: RIO), or Fortescue (ASX: FMG) or knows someone who does.

Also, I know that about 98% of our country’s wealth (and the Treasurer’s budget surplus) comes from us, and let’s face it, where would Australia be without the great state of WA?

Whilst I can’t prove any of my statistics, I am pretty sure that WA’s and Australia’s economic fortunes have likely taken a nose-dive over the last few weeks as the price of iron ore has dropped around 10% to just over US$100/t. Worse still, it’s down about 25% since the start of the year.

The prices of iron ore miners are struggling too, as the below table indicates.

Company | Last Price | 1-mo Chg % | 2024 Chg % | 1-yr Chg % | MarketCap $M |

|---|---|---|---|---|---|

BHP Group (BHP) | $43.90 | +1.1% | -13.4% | +1.5% | $233,707 |

Rio Tinto (RIO) | $125.60 | -4.6% | -7.8% | +14.0% | $216,974 |

Fortescue (FMG) | $24.12 | -9.9% | -17.2% | +22.5% | $74,265 |

Mineral Resources (MIN) | $69.55 | -10.5% | -2.0% | +0.1% | $13,628 |

Champion Iron (CIA) | $6.43 | -10.8% | -23.2% | +7.2% | $3,331 |

Deterra Royalties (DRR) | $4.58 | -8.2% | -13.6% | +4.3% | $,2421 |

Mount Gibson Iron (MGX) | $0.410 | -7.9% | -26.1% | 0% | $498 |

Grange Resources (GRR) | $0.370 | -14.0% | -22.1% | -30.8% | $428 |

ASX iron ore stocks share price performances in 2024

The current state of the iron ore price is exactly what’s expected, according to major broker Macquarie. It’s just demand versus supply they suggest in their latest research note on iron ore and the ASX iron ore sector titled “Iron ore shipments Strong supply meets slowing demand”.

Let’s take a look at the key factors affecting each side of the iron ore price discovery process, as well as Macquarie’s outlook for iron ore prices in the near and long term, and finally, their views on ASX iron ore stocks.

Solid supply

The supply side of the iron ore price equation is one of seasonal strength from Pilbara-based producers BHP, RIO, and FMG, as well as unseasonal strength from major Brazilian producer Vale.

The local cohort increased their production in the April-May period by around 14% compared to the previous corresponding period. Macquarie notes June could deliver a further surge in production as it’s seasonally a very strong production month (typically 9% above than the annual average).

Also, June is the last opportunity for BHP, RIO, and FMG to catch up on their respective FY24 production guidance after what was a slow start to 2024.

In Brazil, the other major global iron ore producer, Vale, has logged a massive 33% increase in exports in April and May in what Macquarie notes is “traditionally a weaker seasonal period”. Macquarie describes Vale’s 34% jump in volumes in a single week in May as “remarkable”.

The upshot of all the above is that shipments of iron ore into China are likely to have rebounded in the June quarter and are likely bumping into capacity limits. The kicker is, these shipments are going to arrive at a time when port stocks in China remain “largely elevated”, according to Macquarie.

Figure 6 - Port stock elevated at 148.5mt. Source: Platts, Mysteel, Thurlestone, Macquarie Strategy (From: Iron ore shipments Strong supply meets slowing demand, Macquarie Research 5 June 2024)

Weak demand

Turning to Chinese steel industry production – the ultimate destination for the vast majority of the world’s iron ore – Macquarie highlights that its May steel survey “showed sluggish sentiment”.

Orders were improving though, notes the broker, but this was to do with more participants turning positive rather than how positive they were. Overall Macquarie suggests “sentiment magnitude improvement is marginal” as steel mills are losing money in the current environment, and steel traders are looking to destock further due to weak demand.

Figure 7 - Hot metal output down -0.4% WoW. Source: Platts, Mysteel, Fubao, Macquarie Strategy. (From: Iron ore shipments Strong supply meets slowing demand, Macquarie Research 5 June 2024)

Equals lower prices

Iron-ore prices have remained buoyant, acknowledges Macquarie, noting that prices above US$100/t and as high as US$140/t earlier in the year have been supported by “financial flows” in anticipation the Chinese government would provide aggressive stimulus to support its ailing property sector.

The recent moderation in the iron ore price, which averaged US$114/t for 62% grade product, had converged to Macquarie’s “near-term” forecast of US$115/t. In the longer run, the broker expects further falls in the iron ore price which would likely average US$110/t in FY25, US$95/t in FY26, US$85/t in FY27, and $78/t in FY28.

Figure 8 - Iron ore prices are trading above our near-term price forecasts. Source: Bloomberg, Macquarie Research. (From: Iron ore shipments Strong supply meets slowing demand, Macquarie Research 5 June 2024)

Equals mixed views on ASX iron ore stocks

Macquarie’s seemingly bearish iron ore estimates might shock many investors in ASX iron ore stocks, but it’s consistent with most other estimates, as well as longer term Australian Government projections.

This means that if those falls do transpire, it’s not necessarily going to spell disaster for the share prices of local iron ore miners – at least some of the falls have undoubtedly already been priced in.

But, from time to time, history shows that supply (usually weather, but sometimes something bigger like a pandemic) and demand factors (usually the health of the Chinese property market) can conspire to shoot prices above or below consensus estimates.

This can cause volatility in the share prices of iron ore stocks as investors try to guess how long higher/lower prices might contribute to better/worse than expected earnings. That’s kind of where we are right now.

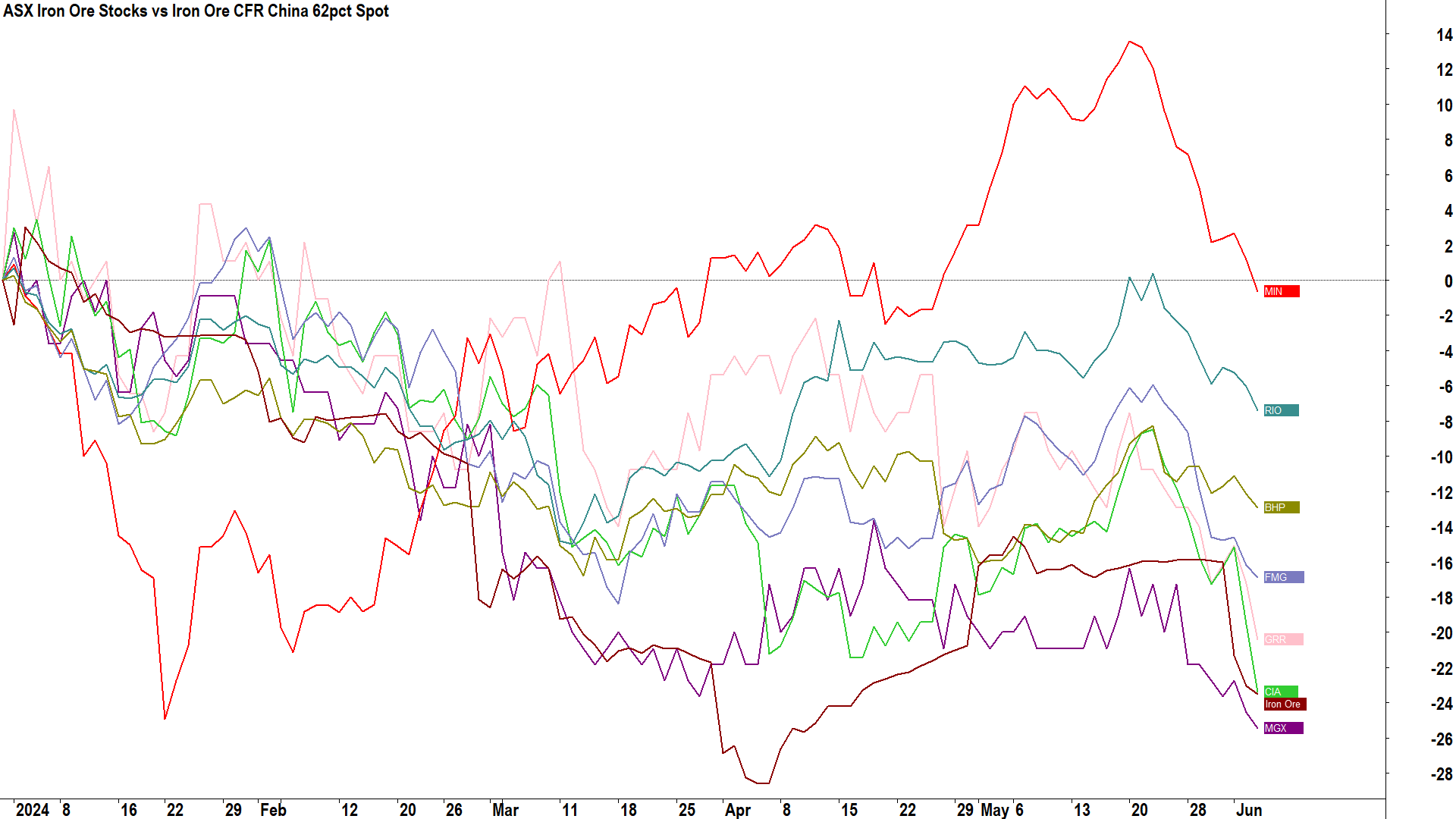

The chart below best illustrates both the volatility in the share prices in ASX iron ore stocks, and that for the most part, at least some of the fall in the iron ore price was already factored in (note how share prices generally haven’t fallen as much as the iron ore price).

ASX Iron Ore Stocks vs Iron Ore CFR China 62pct Spot. Click here for full size image.

{kind=link}

Macquarie notes FMG has the greatest upside with respect to earnings should prices remain higher than forecast, but naturally, this is a double-edged sword. “FMG boasts material upside for FY25E-FY26E at 25-98%” notes Macquarie. This compares to RIO’s +7% in FY25, +37% in FY26, and +63% in FY27 and BHP’s +2% in FY25, +41% in FY26, and +75% in FY27.

Despite the potential upside in the earnings of ASX iron ore stocks at spot prices, Macquarie bases its ratings and price targets on its forecasts and not on the volatility of spot prices. This means that it only has two ratings better than neutral in its ASX iron ore coverage: Mineral Resources (ASX: MIN) and Mount Gibson Iron (ASX: MGX).

Macquarie’s ASX iron ore sector coverage. Source: Macquarie Research (From: Iron ore shipments Strong supply meets slowing demand, Macquarie Research 5 June 2024) (“+/- Potential” column is based on closing prices of each stock on Wednesday 5 June)

*Note that in a separate research note published today (“Mineral Resources D(leveraging)-Day”) Macquarie cut its price target on MIN from $78 to $75 due to “a weaker earnings outlook and reduction of services multiple from 6.5x to 6.0x”.