10 ASX gold stocks the experts recommend to buy right now

Gold had its weakest quarterly performance since 2013, but a range of factors is keeping experts bullish.

Source: Shutterstock

Mentioned

KEY POINTS

- After a record-breaking run, gold has just endured its steepest quarterly fall in over a decade, driven by shifting Fed expectations and a stronger dollar – with higher energy prices threatening to drive up producer costs.

- Both the gold price and ASX gold stocks have bounced this week, but in both cases, remain well off peak prices.

- In this article, you'll understand why analysts remain bullish on gold, which ASX gold stocks performed well in the recent rally, and what looming FY27 cost pressures could mean for shareholder returns.

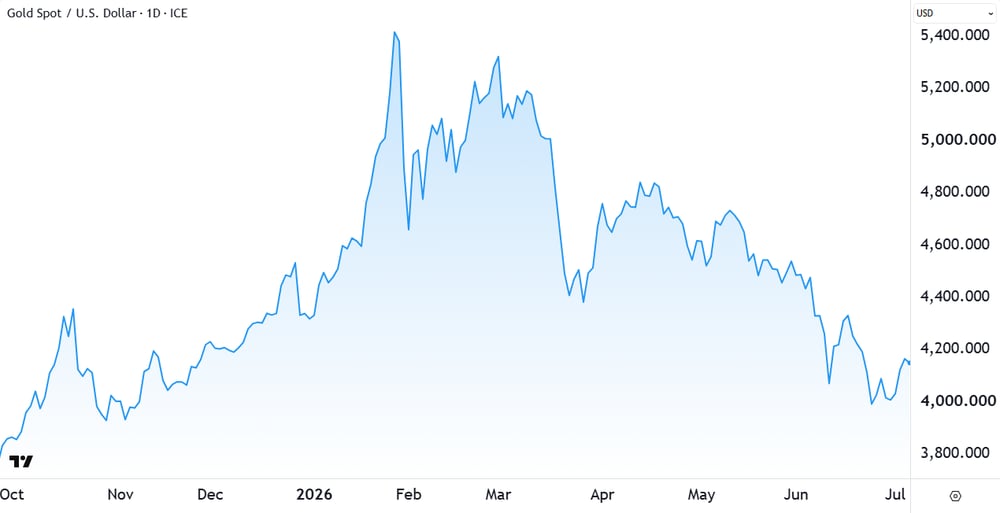

Gold has steadily lost momentum since hitting a record high of US$5,598/oz in January as the Middle East conflict lifted rate expectations due to simmering inflation concerns, and following a substantial appreciation in the US dollar. The June quarter was gold’s weakest in 13 years, ending its third longest winning streak in 50 years.

But a rally is potentially afoot. On Friday, the gold price rose more than 2% after a softer-than-expected US payrolls report cooled fears of further Fed rate hikes and weakened the dollar. The S&P/All Ords Gold Index (XGD) also climbed 8.3% on the same day after positive quarterly announcements from several gold miners, with Northern Star Resources jumping 11%, Catalyst Metals 19% and Genesis Minerals 16%.

Spot gold price chart. Source: TradingView

Analysts are still positive on gold, with several still forecasting a return to US$5,000/oz – but many have also acknowledged there are headwinds facing ASX gold miners. This article breaks down the forces behind gold's recent fall, the latest expert views, and takes a closer look at some of the big quarterly updates so far. Is the bull case for bullion still intact? Let’s dive in.

Why did the gold price drop?

During the June quarter, spot gold fell ~14% to finish near US$4,000/oz (A$5,790/oz), a level not seen since October 2025, and marking its weakest quarter since June 2013. Gold miners came under pressure too, with the global GDX and GDXJ indices down ~18% over the quarter and the XGD falling ~10% in the same period.

The reasons for gold’s demise in the last few months include:

Higher US interest rate outlook: surging energy prices reignited inflation concerns across global economies and triggered a more hawkish tone from Fed Chair Kevin Warsh. Markets moved from pricing in rate cuts to rate hikes, with higher rates generally seen as a negative for gold, as it carries no yield.

Surge in the US dollar: the benchmark for pricing gold is the US dollar, as the US dollar appreciates, it makes gold more expensive in other currencies, potentially reducing demand.

Break in momentum / sentiment: Arguably, the 15% three-day decline in January reset speculative flows into gold and other precious metals. As the gold price pulled back, flows from momentum-based strategies moderated.

ASX miners quarterlies and looming headwinds

Despite a falling commodity price, it seems ASX producers were still able to pull it from the ground within guidance:

Northern Star (NST)

June quarter gold sold of 433koz, taking FY26 gold sold to 1,543koz, meeting revised FY26 group guidance of above 1,500koz.

Vault Minerals (VAU)

June quarter gold production of 89.3koz (gold sold 87.9koz), taking FY26 production to 336.5koz (gold sold 334.9koz), up 14% quarter on quarter and meeting full-year guidance.

Catalyst Metals (CYL)

June quarter gold production of 31.8koz, taking FY26 production to 104koz, in line with FY26 guidance of 100–110koz.

Genesis Minerals (GMD)

June quarter gold production of 70.7koz, taking FY26 production to 285.4koz, within FY26 guidance of 260–290koz.

Miners and investors alike will be buoyed by the recent updates – it’s no mean feat for so many producers to meet guidance (any mining is prone to lost production due to weather, operational issues, unforeseen maintenance, etc.).

But due to the recent surge in fuel prices, extracting gold out of the ground is growing more expensive, and the experts warn there’s a real chance cost pressures may worsen. UBS expects sector-wide all-in sustaining costs (AISC) to rise ~A$110/oz year on year in FY27, to A$2,760/oz from A$2,650/oz, which it sees driving 5% earnings per share downside on average in FY27.

The investment bank also believes that in the wake of the Middle East conflict, impacts from the oil shock are likely to keep working their way through supply chains, with the effects showing up over the next six to 12 months — especially in anything made from or moved using diesel. That could mean delayed projects and slower ramp-ups, and higher costs across the board.

With all this said, miners managed to mitigate the toughest period for gold in over a decade, with GMD’s Executive Chair Raleigh Finlayson saying the miner managed to “generate higher underlying cashflow than the previous quarter despite a lower gold price [and a] higher diesel price.”

Gold price outlook

Reasons the experts are still positive on gold:

Rising US debt: With US federal debt already past US$39 trillion and projected to keep climbing, Canaccord Genuity said in a recent note that the mounting debt pile is one of the key supports for gold, as swelling deficits and borrowing erode confidence in the US dollar and push investors and central banks toward gold as an alternative store of value.

Higher inflation threat: UBS lists higher inflation among the conditions keeping the case for gold compelling, since rising prices erode the real return on cash and bonds and make non-yielding gold relatively more attractive.

Persistent geopolitical risk: Potential conflicts and trade tensions drive investors toward gold as a safe haven, lifting demand and price; Canaccord Genuity counts it as a pillar of its bullish gold thematic.

Continued tariff uncertainty: Tariffs stoke inflation and cloud the growth outlook, pushing investors toward gold as a hedge; UBS counts it as part of the backdrop underpinning demand, alongside weaker growth and dollar-related risks.

Sustained central bank buying: Canaccord Genuity points to China's buying of the precious metal in its bullish case for gold, noting it bought 320koz in May, its largest since December 2024, and has purchased 810koz year to date, nearly matching the 860koz bought in all of 2025.

Experts top ASX gold picks

Without taking the cost pressures lightly, Canaccord Genuity sees the gold landscape as ripe for investment. The broker notes that ASX gold sector valuations remain “relatively undemanding”, with its coverage currently trading at price to net asset value (P/ NAV) of 0.66 times, less than the historical average of 0.84 times. This “encourages positioning in the sector,” the broker said.

Looking at the broader broker coverage of the gold sector, it also remains decidedly bullish. Based on data in the Market Index Broker Consensus archive, of the major ASX gold producers, only Evolution Mining (EVN) is hold consensus rated, with the rest sporting consensus buys.

ASX Gold Sector Broker Consensus Summary, 3 months to 7 July 2026. Source: Market Index Broker Consensus. To obtain a stock’s Broker Consensus Rating, we assign a value of +1 to any rating better than HOLD/NEUTRAL/MARKETWEIGHT, a value of 0 for any rating equivalent to HOLD/NEUTRAL/MARKETWEIGHT, and a value of -1 to any rating worse than HOLD/NEUTRAL/MARKETWEIGHT. We then take the average of all assigned rating values and assign a Broker Consensus Rating of BUY to values greater than +0.5, a rating of HOLD for values between -0.5 and +0.5, and a rating of SELL for values less than -0.5. The Broker Consensus Target is simply the average of the target prices we have on file for each broker. Typically, brokers define their target prices as a 12-month forecast. Each target price is based on fundamental valuation assumptions.

Note that a Consensus Rating Value of 1.0 implies unanimous buy ratings among the brokers surveyed, demonstrating the strength of consensus for stocks like WAF, WGX, GMD, CYL, PRU, OBM, and NEM. RMS is also very highly rated, with a Consensus Rating Value of 0.90. RRL and NST are closer to the buy-hold 0.5 cutoff, and at 0.42, EVN sits just shy.

As for price growth upside to Consensus Target, this is where investors may wish to take the broker consensus with a pinch of salt. Many price targets were ratcheted up during gold’s bull phase through 2025 and the start of this year, and it’s possible some brokers are yet to mark their price targets to market after the recent pullback.

But, for what it’s worth, CYL is seen to have the greatest potential for price appreciation (+86.9% to Consensus Target), with WAF, RMS, WGX, OBM, and GMD also seen as substantially undervalued (each +50% to Consensus Target). Even EVN's 11.7% – the smallest upside in the table – still sits above the ASX 200's long-run average annual return.

When using broker consensus data, consider that stocks with greater coverage are likely to have the most reliable metrics. I’ve used a minimum cut off of three brokers to calculate a consensus, and there is a 3-month cut off on recency to ensure we are dealing with the latest broker data.

Conclusion

The gold bull run may have come off the boil, but ASX gold producers kept pulling it out of the ground within guidance and the brokers have remained bullish. The bigger question is cost, with UBS flagging that the oil shock could push all-in sustaining costs higher through FY27 and eat into earnings.

Whether this slump proves a reset or something worse comes down to whether gold's structural supports still hold, and on that front the case looks intact for now. Next month's full-year results are the next real test, so it's worth watching what the miners say about costs and cash when the numbers land.